Answered step by step

Verified Expert Solution

Question

1 Approved Answer

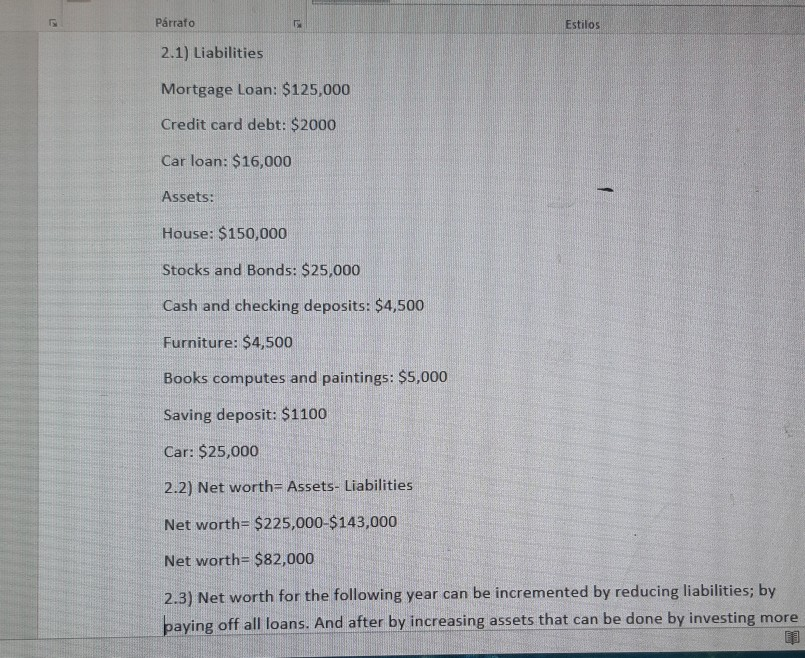

the net worth was calculated at $82, 000 this is the answer for question one (iii) (30 marks) Now suppose that YOU have an initial

the net worth was calculated at $82,000

this is the answer for question one

(iii) (30 marks) Now suppose that YOU have an initial endowment equivalent to an amount of THE NET WORTH calculated in question (i) above. If the current market interest rate is 3% and is expected to remain at this level for a long time, what will be the expected value of your initial endowment at the end of two years? What is the value for fifteen (15) years? What is the value for twenty-five (25) years? Why are the expected values different for the different periods even though the interest rate remains the same? Explain carefully. (10 marks) First, distinguish between an income/expenditure statement and a flow-of-funds statement; then, suppose you are given the following information on the revenues, expenses, assets and liabilities of a hypothetical Canadian chartered bank for the year 2018, determine the bank's return on assets (ROA). its return on equity (ROE), its liquidity (liquid asset) ratio, and capital adequacy (leverage) ratio. Lastly, construct BOTH the bank's balance sheet statement for the end of the year, 2018 and its income-expenditure statement for that year: Salaries and employee benefits..... $180,000; Interest on deposits..... $290,000; Interest income from loans..... $320,000; Investment income from Government of Canada bonds..... $75,000; Interest on non-deposit borrowing.....$30,000: Applicable income taxes..... $150,000; Occupancy costs.....$21,000; Provision for loan losses.....$52,000; Miscellaneous expenses..... $8,000; Interest on municipal securities..... $86,000; Service charges on deposits.... $210,000; Miscellaneous operating revenues..... $130.000; Bank equity capital.... $70 million: Demand (checking) deposits accounts .....$100 million; Savings deposit accounts.....$150 million; Time (fixed term) deposit accounts.....$300 million; Advances (loans) from the central bank.....$12 million; Cash reserves.....$20 million; Other assets.....$150 million; Real estate [i.e., mortgage] loans.....$80 million. Government of Canada securities.....$25 million; Commercial and industrial loans... $300 million: Other liabilities.....$38 million; Municipal securities.....$55 million; Loans to individuals.....$40 million. (50 marks) Prrafo Estilos 2.1) Liabilities Mortgage Loan: $125,000 Credit card debt: $2000 Car loan: $16,000 Assets: House: $150,000 Stocks and Bonds: $25,000 Cash and checking deposits: $4,500 Furniture: $4,500 Books computes and paintings: $5,000 Saving deposit: $1100 Car: $25,000 2.2) Net worth= Assets- Liabilities Net worth= $225,000-$143,000 Net worth= $82,000 2.3) Net worth for the following year can be incremented by reducing liabilities; by paying off all loans. And after by increasing assets that can be done by investing more (iii) (30 marks) Now suppose that YOU have an initial endowment equivalent to an amount of THE NET WORTH calculated in question (i) above. If the current market interest rate is 3% and is expected to remain at this level for a long time, what will be the expected value of your initial endowment at the end of two years? What is the value for fifteen (15) years? What is the value for twenty-five (25) years? Why are the expected values different for the different periods even though the interest rate remains the same? Explain carefully. (10 marks) First, distinguish between an income/expenditure statement and a flow-of-funds statement; then, suppose you are given the following information on the revenues, expenses, assets and liabilities of a hypothetical Canadian chartered bank for the year 2018, determine the bank's return on assets (ROA). its return on equity (ROE), its liquidity (liquid asset) ratio, and capital adequacy (leverage) ratio. Lastly, construct BOTH the bank's balance sheet statement for the end of the year, 2018 and its income-expenditure statement for that year: Salaries and employee benefits..... $180,000; Interest on deposits..... $290,000; Interest income from loans..... $320,000; Investment income from Government of Canada bonds..... $75,000; Interest on non-deposit borrowing.....$30,000: Applicable income taxes..... $150,000; Occupancy costs.....$21,000; Provision for loan losses.....$52,000; Miscellaneous expenses..... $8,000; Interest on municipal securities..... $86,000; Service charges on deposits.... $210,000; Miscellaneous operating revenues..... $130.000; Bank equity capital.... $70 million: Demand (checking) deposits accounts .....$100 million; Savings deposit accounts.....$150 million; Time (fixed term) deposit accounts.....$300 million; Advances (loans) from the central bank.....$12 million; Cash reserves.....$20 million; Other assets.....$150 million; Real estate [i.e., mortgage] loans.....$80 million. Government of Canada securities.....$25 million; Commercial and industrial loans... $300 million: Other liabilities.....$38 million; Municipal securities.....$55 million; Loans to individuals.....$40 million. (50 marks) Prrafo Estilos 2.1) Liabilities Mortgage Loan: $125,000 Credit card debt: $2000 Car loan: $16,000 Assets: House: $150,000 Stocks and Bonds: $25,000 Cash and checking deposits: $4,500 Furniture: $4,500 Books computes and paintings: $5,000 Saving deposit: $1100 Car: $25,000 2.2) Net worth= Assets- Liabilities Net worth= $225,000-$143,000 Net worth= $82,000 2.3) Net worth for the following year can be incremented by reducing liabilities; by paying off all loans. And after by increasing assets that can be done by investing moreStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Sterling Bonds And Fixed Income Handbook

Authors: Mark Glowrey

1st Edition

0857190423, 978-0857190420