Answered step by step

Verified Expert Solution

Question

1 Approved Answer

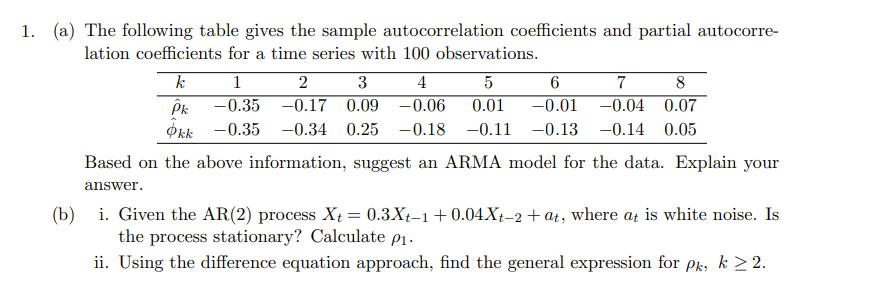

The question is as follows 1. (a) The following table gives the sample autocorrelation coefficients and partial autocorre- lation coefficients for a time series with

The question is as follows

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Discovering Advanced Algebra An Investigative Approach

Authors: Jerald Murdock, Ellen Kamischke, Eric Kamischke

1st edition

1559539844, 978-1604400069, 1604400064, 978-1559539845