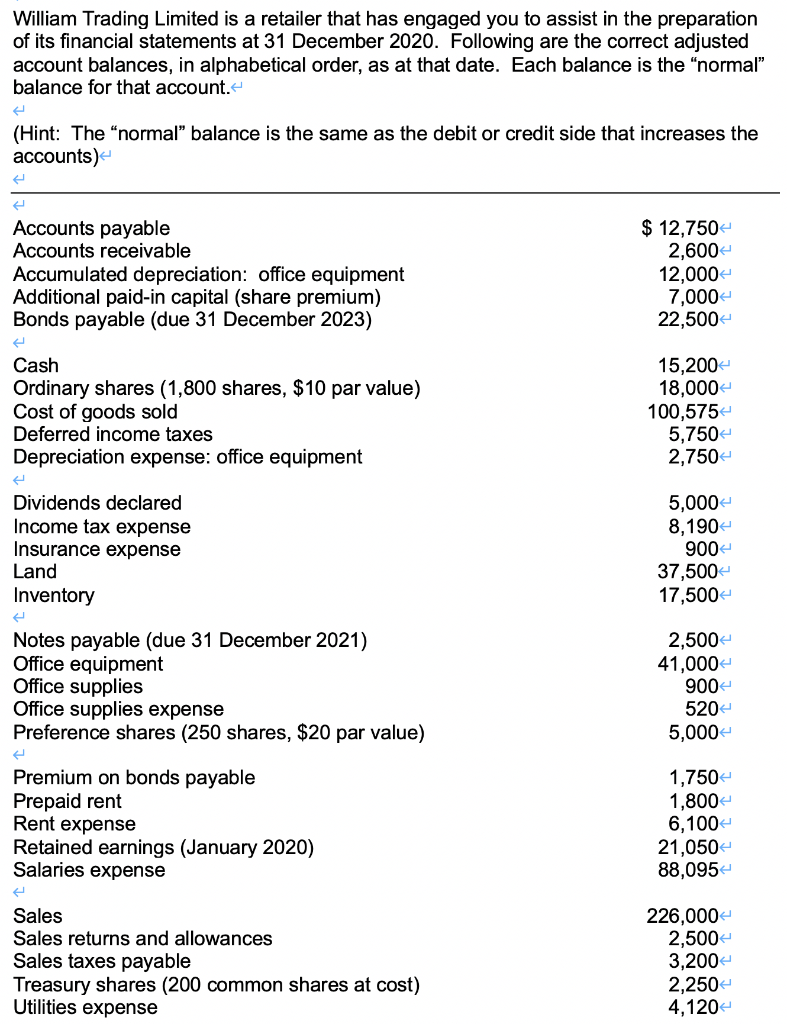

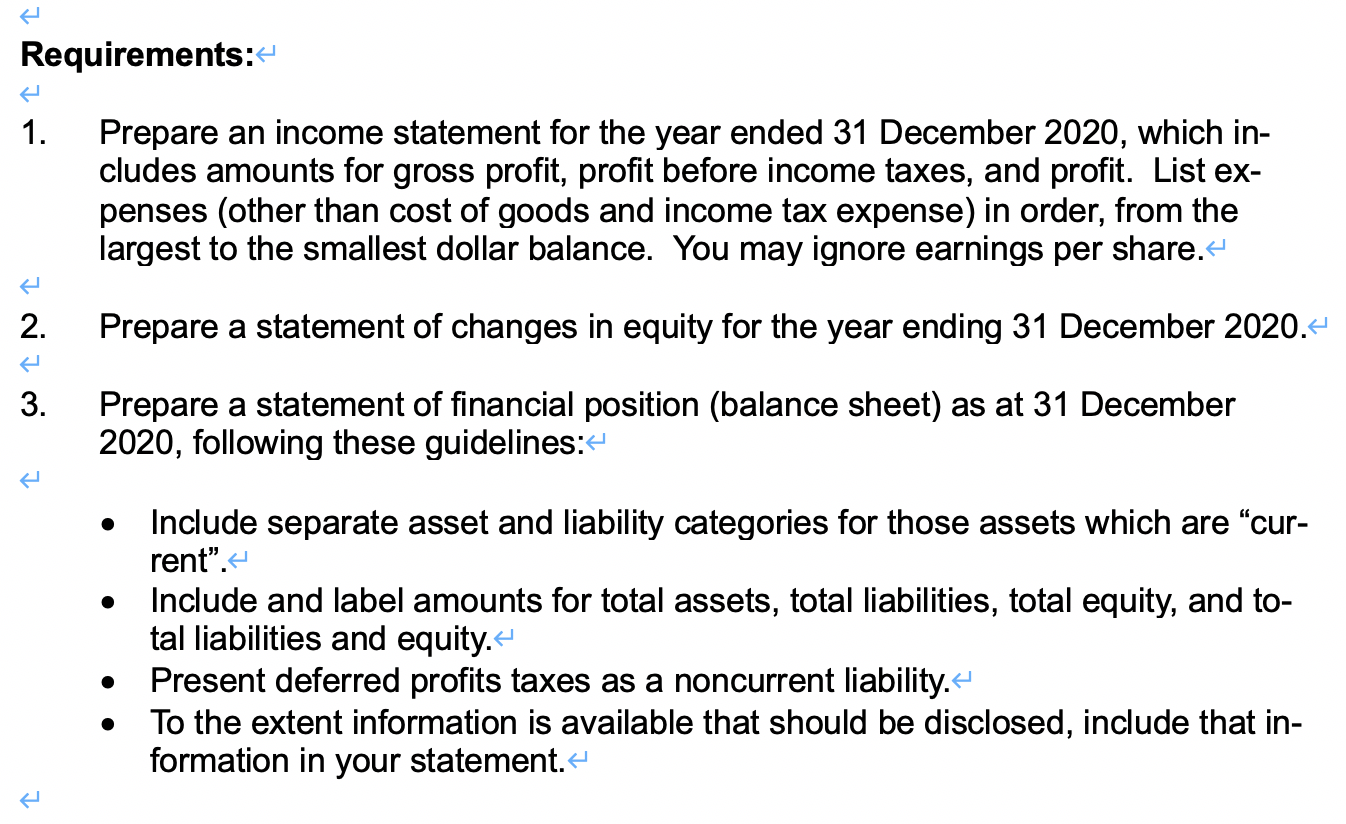

Question

The question requires to draw up (a) Income statement (b) Statement of changes in Equity (c) Statement of Financial Position. Thank You! Note: 1.No hand-written,

The question requires to draw up (a) Income statement (b) Statement of changes in Equity (c) Statement of Financial Position. Thank You!

Note: 1.No hand-written, please use your keyborad. 2. Don't paste or copy other's solutions, Thank you! 3. Please use a formal format for these three statements, including the correct type setting, headings and time period. 4. Please read the requirements below carefully! Please make the correct statements.

Thank you for your answers! I truly appreciate that!

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Managerial Accounting

Authors: Brenda Mallouk

2nd Edition

017640709X, 978-0176407094