Answered step by step

Verified Expert Solution

Question

1 Approved Answer

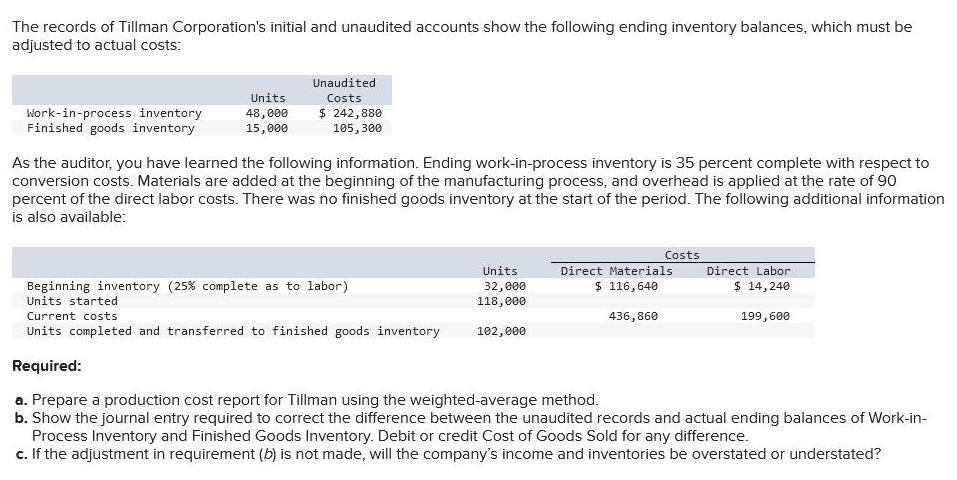

The records of Tillman Corporation's initial and unaudited accounts show the following ending inventory balances, which must be adjusted to actual costs: Work-in-process inventory

The records of Tillman Corporation's initial and unaudited accounts show the following ending inventory balances, which must be adjusted to actual costs: Work-in-process inventory Finished goods inventory Units 48,000 15,000 Unaudited Costs $ 242,880 105,300 As the auditor, you have learned the following information. Ending work-in-process inventory is 35 percent complete with respect to conversion costs. Materials are added at the beginning of the manufacturing process, and overhead is applied at the rate of 90 percent of the direct labor costs. There was no finished goods inventory at the start of the period. The following additional information is also available: Units 32,000 118,000 Costs 102,000 Direct Materials. $ 116,640 436,860 Direct Labor $ 14,240 199,600 Beginning inventory (25% complete as to labor) Units started Current costs Units completed and transferred to finished goods inventory Required: a. Prepare a production cost report for Tillman using the weighted-average method. b. Show the journal entry required to correct the difference between the unaudited records and actual ending balances of Work-in- Process Inventory and Finished Goods Inventory. Debit or credit Cost of Goods Sold for any difference. c. If the adjustment in requirement (b) is not made, will the company's income and inventories be overstated or understated?

Step by Step Solution

★★★★★

3.45 Rating (148 Votes )

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Fundamentals of Cost Accounting

Authors: William Lanen, Shannon Anderson, Michael Maher

5th edition

978-1259728877, 1259728870, 978-1259565403