Answered step by step

Verified Expert Solution

Question

1 Approved Answer

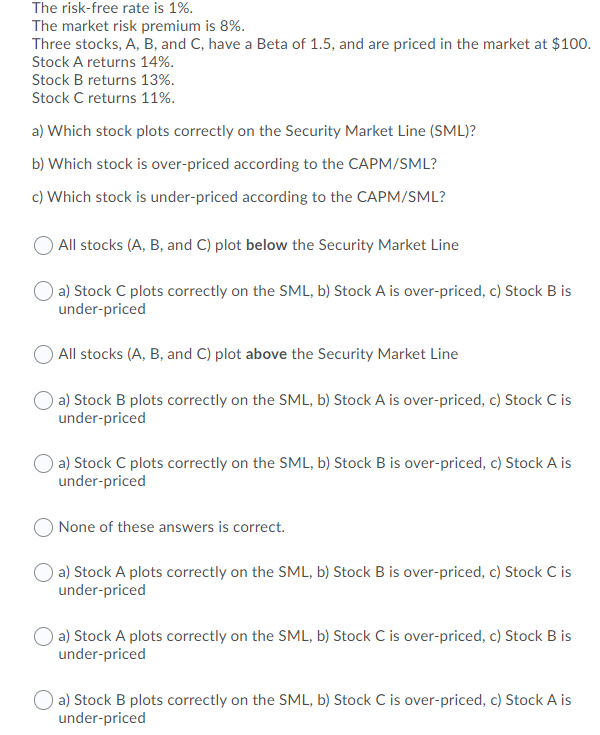

The risk-free rate is 1%. The market risk premium is 8%. Three stocks, A, B, and C, have a Beta of 1.5, and are

The risk-free rate is 1%. The market risk premium is 8%. Three stocks, A, B, and C, have a Beta of 1.5, and are priced in the market at $100. Stock A returns 14%. Stock B returns 13%. Stock C returns 11%. a) Which stock plots correctly on the Security Market Line (SML)? b) Which stock is over-priced according to the CAPM/SML? c) Which stock is under-priced according to the CAPM/SML? All stocks (A, B, and C) plot below the Security Market Line a) Stock C plots correctly on the SML, b) Stock A is over-priced, c) Stock B is under-priced All stocks (A, B, and C) plot above the Security Market Line a) Stock B plots correctly on the SML, b) Stock A is over-priced, c) Stock C is under-priced a) Stock C plots correctly on the SML, b) Stock B is over-priced, c) Stock A is under-priced None of these answers is correct. a) Stock A plots correctly on the SML, b) Stock B is over-priced, c) Stock C is under-priced a) Stock A plots correctly on the SML, b) Stock C is over-priced, c) Stock B is under-priced a) Stock B plots correctly on the SML, b) Stock C is over-priced, c) Stock A is under-priced

Step by Step Solution

★★★★★

3.50 Rating (160 Votes )

There are 3 Steps involved in it

Step: 1

The detailed answer for the above question is provided below The correct answer is a ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

McGraw Hills Conquering SAT Math

Authors: Robert Postman, Ryan Postman

2nd Edition

0071493417, 978-0071493413