Answered step by step

Verified Expert Solution

Question

1 Approved Answer

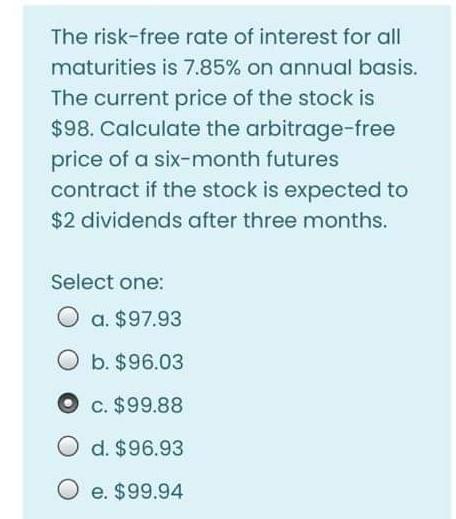

The risk-free rate of interest for all maturities is 7.85% on annual basis. The current price of the stock is $98. Calculate the arbitrage-free price

The risk-free rate of interest for all maturities is 7.85% on annual basis. The current price of the stock is $98. Calculate the arbitrage-free price of a six-month futures contract if the stock is expected to $2 dividends after three months. Select one: O a. $97.93 O b. $96.03 c. $99.88 O d. $96.93 O e. $99.94

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Modeling Financial Time Series With S PLUS

Authors: Eric Zivot, Jiahui Wang

2nd Edition

0387279652, 0387323481, 9780387279657, 9780387323480