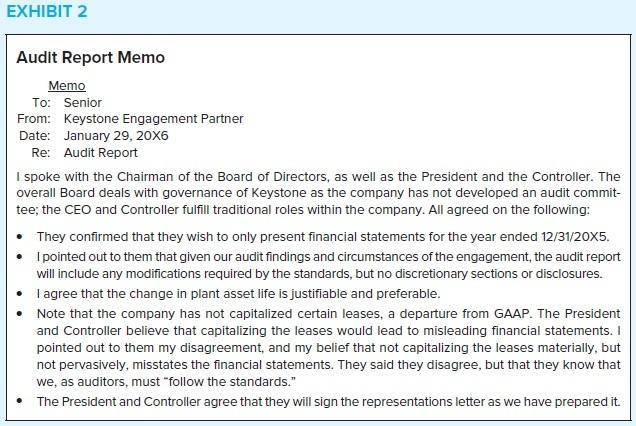

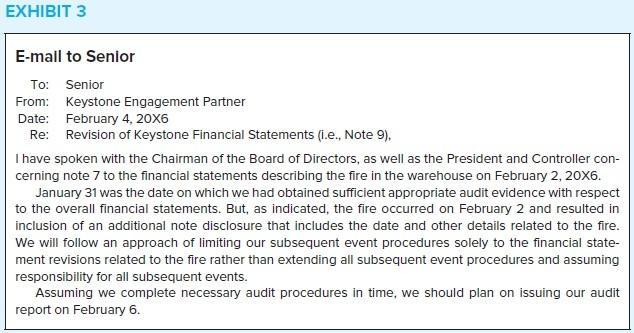

The simulation presents a draft of a nonpublic company audit report document and three exhibits. To allow this DRS to stand alone without consideration of

The simulation presents a draft of a nonpublic company audit report document and three exhibits. To allow this DRS to stand alone without consideration of other parts of the Keystone Computers & Networks, Inc. (Keystone) case, assume that the findings described in this case were identified very late in the audit and that any other misstatements identified in other portions of the case have been corrected.

An associate member of the Adams, Barnes & Co. audit team prepared a first draft of the audit report on Keystone’s 20X5 financial statements.

Required:

Your job as senior on the engagement is to review and revise the 20X5 audit report for the Keystone audit. For each of the sentences called out in the points on the document, determine if the current language is appropriate as is, should be removed altogether, or replaced with any of the provided alternatives. Ensure that the 20X5 list is appropriate given the information provided. Links to each of the exhibits are provided in the document, but are available in the list below for convenience.

Exhibit 1 - Working Paper Memo

Exhibit 2 - Audit Report Memo

Exhibit 3 - E-mail to Senior

Document

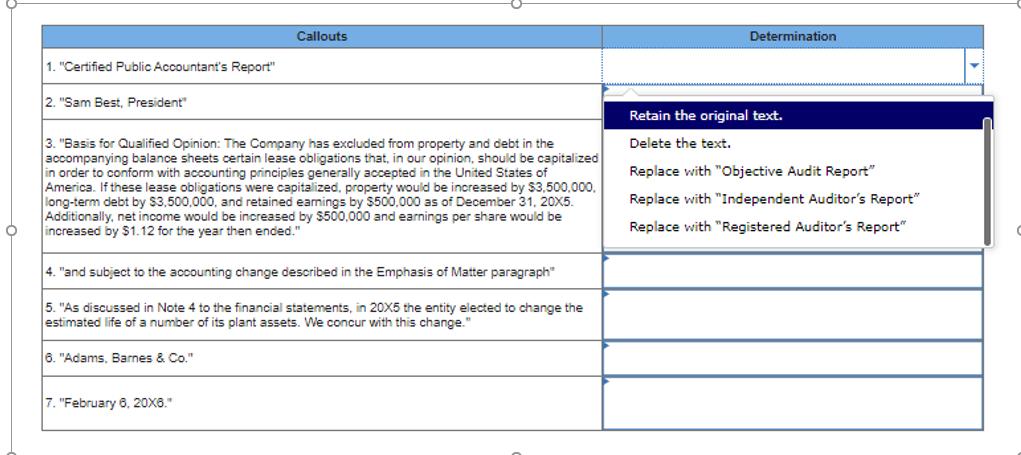

(For each Document Callout, choose the correct Determination from the table below.)

Certified Public Accountant’s Report (Callout #1)

To Sam Best, President: (Callout #2)

We have audited the accompanying financial statements of Keystone Computers & Networks, Inc., which comprise the balance sheet as of December 31, 20X5, and the related statements of income, changes in stockholders’ equity, and cash flows for the year then ended, and the related notes to the financial statements.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits in accordance with auditing standards generally accepted in the United States of America. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Basis for Qualified Opinion

The Company has excluded from property and debt in the accompanying balance sheets certain lease obligations that, in our opinion, should be capitalized in order to conform with accounting principles generally accepted in the United States of America. If these lease obligations were capitalized, property would be increased by $3,500,000, long-term debt by $3,500,000, and retained earnings by $500,000 as of December 31, 20X5. Additionally, net income would be increased by $500,000 and earnings per share would be increased by $1.12 for the year then ended. (Callout #3)

Opinion

In our opinion, except for the effects of the matter described in the Basis for Qualified Opinion paragraph and subject to the accounting change described in the Emphasis of Matter paragraph, (Callout #4) the financial statements referred to above present fairly, in all material respects, the financial position of Keystone Computers & Networks, Inc., as of December 31, 20X5, and the results of its operations and its cash flows for the year then ended in accordance with accounting principles generally accepted in the United States of America.

Emphasis of Matter

As discussed in Note 4 to the financial statements, in 20X5 the entity elected to change the estimated life of a number of its plant assets. We concur with this change. (Callout #5)

Adams, Barnes & Co. (Callout #6)

Phoenix, Arizona

February 6, 20X6. (Callout #7)

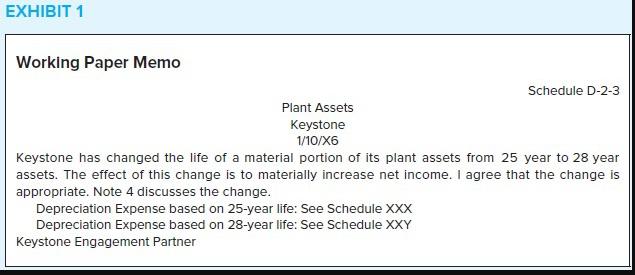

EXHIBIT 1 Working Paper Memo Schedule D-2-3 Plant Assets Keystone 1/10/X6 Keystone has changed the life of a material portion of its plant assets from 25 year to 28 year assets. The effect of this change is to materially increase net income. I agree that the change is appropriate. Note 4 discusses the change. Depreciation Expense based on 25-year life: See Schedule XXX Depreciation Expense based on 28-year life: See Schedule XXY Keystone Engagement Partner

Step by Step Solution

3.49 Rating (169 Votes )

There are 3 Steps involved in it

Step: 1

Callouts Determination 1 Certified Public Accountants Report Replace with Independent Auditors Repor...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Ray Whittington, Kurt Pany

19th edition

978-0077804770, 78025613, 77804775, 978-0078025617