Answered step by step

Verified Expert Solution

Question

1 Approved Answer

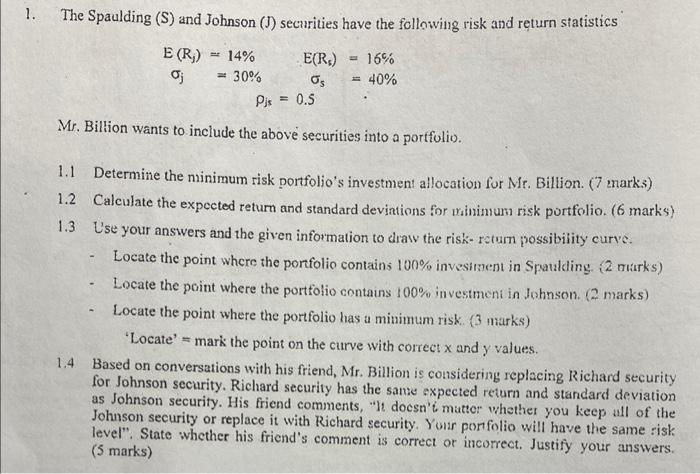

The Spaulding (S) and Johnson (J) securities have the following risk and return statistics E(Rj)=14%E(R5)=16% j=30%s=40% js=0.5 Mr. Biltion wants to include the above securities

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance In America An Unfinished Story

Authors: Kevin R. Brine, Mary Poovey

1st Edition

022650204X, 978-0226502045