Question

The spreadsheet Group Report Data.xlsx contains monthly returns on eleven Australian industry portfolios from January 2011 to March 2022. The industry abbreviations are in the

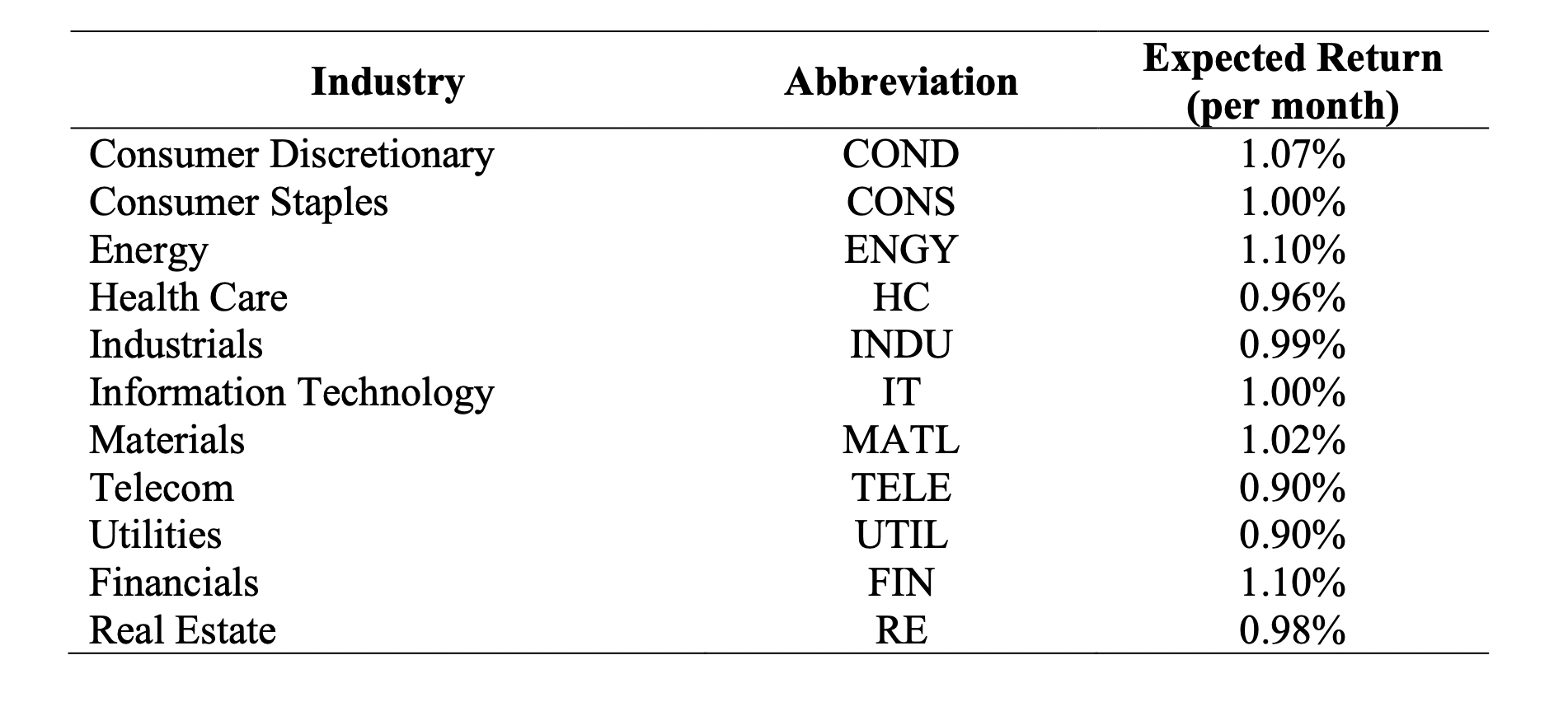

The spreadsheet Group Report Data.xlsx contains monthly returns on eleven Australian industry portfolios from January 2011 to March 2022. The industry abbreviations are in the table below.

Investor utility is represented by: U = E(R) 12A2. There are two investors with different risk aversion coefficients (A). Gladys has a risk aversion coefficient of 7 and Dominic has a risk aversion coefficient of 3. Investors are able to short-sell each industry throughout the report. Investors are unable to borrow or lend at the risk-free rate except for part 5 of the report. The expected returns per month to be used throughout the report are in the following table. Do not use historical average returns as expected returns. You need to use the historical returns to estimate the covariance matrix.

Calculate the optimal portfolio for both investors that consists of all eleven industries. Compare this to the other portfolios you have already estimated in parts 1, 2 and 3 in terms of diversification benefits. What do you observe? Contrast the differences in what you observe between the two investors. (15 marks)

Industry Abbreviation Consumer Discretionary Consumer Staples Energy Health Care Industrials Information Technology Materials Telecom Utilities Financials Real Estate COND CONS ENGY HC INDU IT MATL TELE UTIL FIN RE Expected Return (per month) 1.07% 1.00% 1.10% 0.96% 0.99% 1.00% 1.02% 0.90% 0.90% 1.10% 0.98% Industry Abbreviation Consumer Discretionary Consumer Staples Energy Health Care Industrials Information Technology Materials Telecom Utilities Financials Real Estate COND CONS ENGY HC INDU IT MATL TELE UTIL FIN RE Expected Return (per month) 1.07% 1.00% 1.10% 0.96% 0.99% 1.00% 1.02% 0.90% 0.90% 1.10% 0.98%

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial management theory and practice

Authors: Eugene F. Brigham and Michael C. Ehrhardt

12th Edition

978-0030243998, 30243998, 324422695, 978-0324422696