Question

The Starbucks integrative case provides you with an opportunity to apply to Starbucks the entire six step analysis framework of this textbook. This portion of

The Starbucks integrative case provides you with an opportunity to apply to Starbucks the entire six step

analysis framework of this textbook. This portion of the integrative case relies on the analysis of Starbucks financial statements through fiscal year 2012 and applies the seven-step forecasting procedure of this chapter to develop complete forecasts of Starbucks financial statements through Year 5.

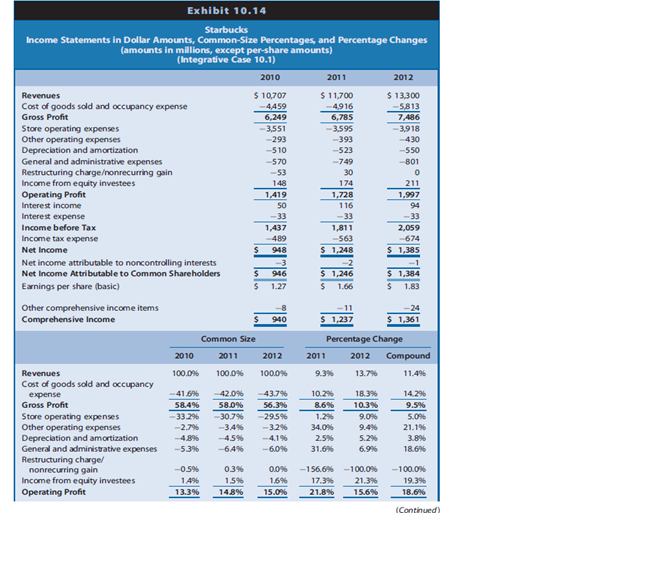

Exhibits 10.14 and 10.15 provide Starbucks income statements and balance sheets for fiscal years 2010 through 2012 in dollar amounts, common-size format, and rate-of-change format.

Exhibit 10.16 presents Starbucks statements of cash flows for fiscal years 2010 through 2012. These financial statements report the financial performance and position of Starbucks and summarize the results of Starbucks operating, investing, and financing activities. The common-size and rate-of-change balance sheets and income statements for Starbucks highlight relations among accounts and trends over time.

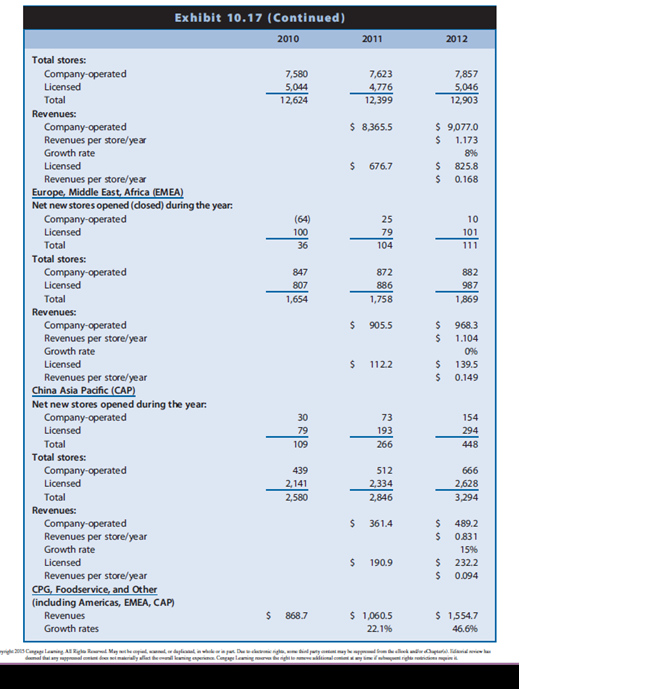

Exhibit 10.17 provides sales analysis data and store operating data through fiscal year 2012, including same store sales growth rates, new store openings, and total numbers of stores open, including a detailed breakdown of revenues and revenue growth by segment and by store-type.

Note: Management guidance, disclosed in 2012 and again at the end of the first quarter in Year 1, indicates Starbucks is planning to open roughly 1,300 new stores during Year 1 (300 owned and 300 licensed stores in the Americas; 200 owned and 400 licensed stores in the China Asia Pacific segment; and 34 owned and 66 licensed stores in the Europe, Middle East and Africa segment). Starbucks management also indicated they expect to incur $1,200 million in capital expenditures during Year 1. Management did not provide guidance beyond Year 1.

REQUIRED

Develop complete forecasts of Starbucks income statements, balance sheets, and statements of cash flows for Years 1 through 5. As illustrated in this chapter, develop objective and unbiased forecast assumptions for all of Starbucks future operating, investing, and financing activities through Year 5 and capture those expectations using financial statement forecasts.

SPECIFICATIONS

a. Build your own spreadsheets to develop and capture your financial statement forecast assumptions and data for Starbucks

b. Starbucks operating, investing, and financing activities involve primarily opening and operating company-owned retail coffee shops in the United States and around the world. Starbucks annual reports provide useful data on the number of company-operated stores Starbucks owns, the new stores it opens each year, and the same-store sales growth rates. These data reveal that Starbucks revenues and revenue growth rates differ significantly across different segments. Use these data, summarized in Exhibit 10.17 as a basis to forecast (1) Starbucks future sales from existing stores, (2) the number of new company-operated stores Starbucks will open, (3) future sales from new stores, and (4) capital expenditures for new stores.

c. Starbucks business also involves generating revenues from licensing Starbucks stores and selling Starbucks coffee and other products through foodservice accounts, grocery stores, warehouse clubs, and so on. Use the data in Exhibits 10.17 to build forecasts of future revenues from licensing activities and foodservice and other activities.

d. Use your forecasts of capital expenditures for new stores together with Starbucks data on property, plant, and equipment and depreciation to build a schedule to forecast property, plant, and equipment and depreciation expense as described in the chapter for PepsiCo.

e. Starbucks appears to use repurchases of common equity shares as the flexible financial account for balancing the balance sheet. Common equity share repurchases are similar to dividends as a mechanism to distribute excess capital to common equity shareholders. Therefore, build your financial statement forecasts using dividends as the flexible financial account.

Exhibit 10.14 Income Statements in Dollar Amounts, Common-size Percentages, and Percentage Changes (amounts in millions, except pershare amounts) (Integrative Case 10.1) 2010 2011 2012 10707 11,700 13300 Cost of goods sold and occupancy expense 4459 4916 5813 Gross Profit 6.249 6,785 7 486 Store operating expenses 3,55 3595 3918 Other operating expenses 393 -430 Depreciation and amortization -510 -523 550 General and administrative expenses -570 Restructuring chargeonrecurring gain Income from equity investees 148 Operating Profit A19 1,728 1, 97 Interest income Interest expense 33 Income before Tax 2,059 1A37 1,811 Income tax expense 563 674 3 948 31 3 1,248 1,385 Net Income Net income attributable to noncontrolling interests Net Income Attributable to Common Shareholders 946 1,246 1,384 Earnings per share basic) 1.66 Other comprehensive income items Comprehensive income 940 1237 Common Size Percentage Change Compound 2010 2012 2011 2012 93% 37% 11.4% 00.0% 100.0% 1000% Cost of goods sold and occupancy -42.0% -43,79% 00.2% 8.3% 14.2 Gross Profit 58.49% 58.0% 56.39% 10.3% 9.5% Store operating expenses -30.7% -295% 1.2% 90% other operating expenses 3A9% 9.4% Depreciation and amortization -48% -4.5% 4.1% General and administrative expenses 5.3% -649% 31.6% 69% 18.6% Restructuring charge/ nonrecurring gain Income from equity investees 16% 17.3% 21.3% Operating Profit (Continued Exhibit 10.14 Income Statements in Dollar Amounts, Common-size Percentages, and Percentage Changes (amounts in millions, except pershare amounts) (Integrative Case 10.1) 2010 2011 2012 10707 11,700 13300 Cost of goods sold and occupancy expense 4459 4916 5813 Gross Profit 6.249 6,785 7 486 Store operating expenses 3,55 3595 3918 Other operating expenses 393 -430 Depreciation and amortization -510 -523 550 General and administrative expenses -570 Restructuring chargeonrecurring gain Income from equity investees 148 Operating Profit A19 1,728 1, 97 Interest income Interest expense 33 Income before Tax 2,059 1A37 1,811 Income tax expense 563 674 3 948 31 3 1,248 1,385 Net Income Net income attributable to noncontrolling interests Net Income Attributable to Common Shareholders 946 1,246 1,384 Earnings per share basic) 1.66 Other comprehensive income items Comprehensive income 940 1237 Common Size Percentage Change Compound 2010 2012 2011 2012 93% 37% 11.4% 00.0% 100.0% 1000% Cost of goods sold and occupancy -42.0% -43,79% 00.2% 8.3% 14.2 Gross Profit 58.49% 58.0% 56.39% 10.3% 9.5% Store operating expenses -30.7% -295% 1.2% 90% other operating expenses 3A9% 9.4% Depreciation and amortization -48% -4.5% 4.1% General and administrative expenses 5.3% -649% 31.6% 69% 18.6% Restructuring charge/ nonrecurring gain Income from equity investees 16% 17.3% 21.3% Operating Profit (ContinuedStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The ImpactAssets Handbook For Investors

Authors: Jed Emerson

1st Edition

1783087293, 978-1783087297