Answered step by step

Verified Expert Solution

Question

1 Approved Answer

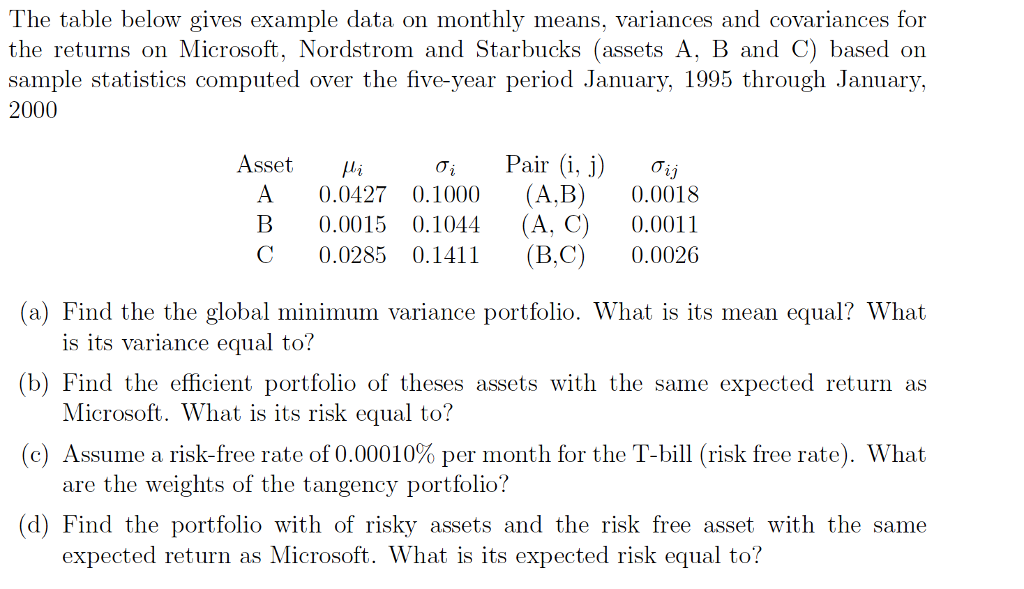

The table below gives example data on monthly means, variances and covariances for the returns on Microsoft, Nordstrom and Starbucks (assets A, B and C)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of Fixed Income Securities

Authors: Frank Fabozzi, Steven Mann, Francesco Fabozzi

9th Edition

1260473899, 978-1260473896