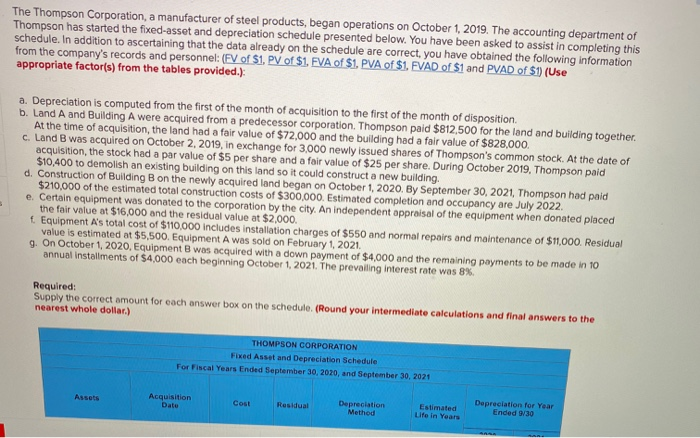

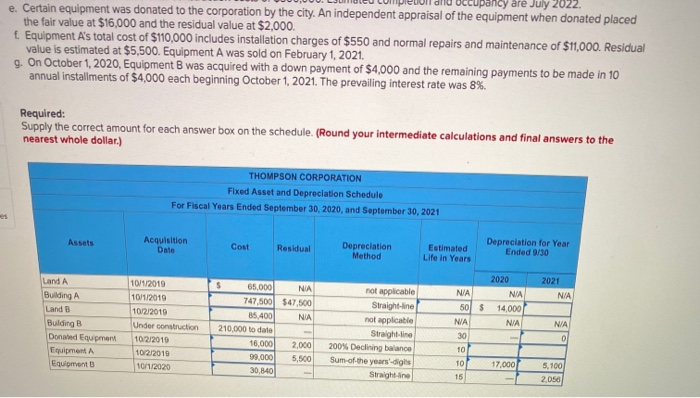

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2019. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel: (FV of $1. PV of $1. EVA of $1. PVA of $1. FVAD of $1 and PVAD of $1) (Use appropriate factor(s) from the tables provided.): a. Depreciation is computed from the first of the month of acquisition to the first of the month of disposition b. Land A and Building A were acquired from a predecessor corporation. Thompson paid $812,500 for the land and building together. At the time of acquisition, the land had a fair value of $72,000 and the building had a fair value of $828,000. C. Land B was acquired on October 2, 2019, in exchange for 3,000 newly issued shares of Thompson's common stock. At the date of acquisition, the stock had a par value of $5 per share and a fair value of $25 per share. During October 2019, Thompson paid $10,400 to demolish an existing building on this land so it could construct a new building. d. Construction of Building Bon the newly acquired land began on October 1, 2020. By September 30, 2021, Thompson had paid $210,000 of the estimated total construction costs of $300,000. Estimated completion and occupancy are July 2022 e. Certain equipment was donated to the corporation by the city. An independent appraisal of the equipment when donated placed the fair value at $16,000 and the residual value at $2,000. & Equipment A's total cost of $110,000 includes installation charges of $550 and normal repairs and maintenance of $11,000. Residual value is estimated at $5,500. Equipment A was sold on February 1, 2021. g. On October 1, 2020. Equipment B was acquired with a down payment of $4,000 and the remaining payments to be made in 10 annual installments of $4,000 each beginning October 1, 2021. The prevailing interest rate was 8%. Required: Supply the correct amount for each answer box on the schedule. (Round your intermediate calculations and final answers to the nearest whole dollar.) THOMPSON CORPORATION Fixed Asset and Depreciation Schedule For Fiscal Years Ended September 30, 2020, and September 30, 2021 Acquisition Residual Cost Depreciation Method Depreciation for Year Ended 9/30 Estimated Life In Years e. Certain equipment was donated to the corporation by the city. An independent appraisal of the equipment when donated placed the fair value at $16,000 and the residual value at $2,000. Equipment A's total cost of $110,000 includes installation charges of $550 and normal repairs and maintenance of $11,000. Residual value is estimated at $5,500. Equipment A was sold on February 1, 2021 On October 1, 2020, Equipment B was acquired with a down payment of $4,000 and the remaining payments to be made in 10 annual installments of $4,000 each beginning October 1, 2021. The prevailing interest rate was 8%. Required: Supply the correct amount for each answer box on the schedule. (Round your intermediate calculations and final answers to the nearest whole dollar.) THOMPSON CORPORATION Fixed Asset and Depreciation Schedule For Fiscal Years Ended September 30, 2020, and September 30, 2021 Acquisition Assets Depreciation for Year Ended 9/30 Cost Depreciation Method Estimated Life in Years Residual Date 2021 NA NUA NA $47.500 2020 NA 14,000 N/A 10/1/2019 10/1/2019 10/2/2010 Under construction S 50 NA NA Land A Bunga Land B Bulding B Donald Equipment Equipment Eugment N/A S 65000 747,500 5.400 210.000 to date 16.000 09.000 30,840 not applicable Straight-line not applicable Straight-line 200% Declining balance Sum of the years Straight line 2,000 5.500 10/2/2019 1012020 101 101 15 17 000 5.100