Question

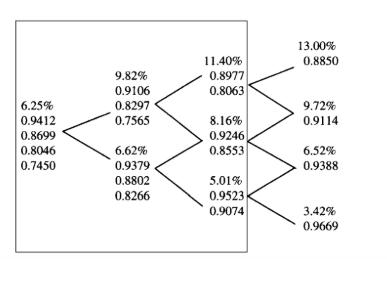

The three-period binomial interest rate tree provided below gives one-period interest rates and prices of zero-coupon bonds. Starting at t = 0, you are provided

The three-period binomial interest rate tree provided below gives one-period interest rates and prices of zero-coupon bonds. Starting at t = 0, you are provided with the one-period interest rate and prices of zero-coupon bonds with maturities of one period, two periods, three periods, and four periods. At t=1, you are provided with the one-period interest rate and prices of zero-coupon bonds with maturities of one period, two periods, and three periods. At t=2, you are provided with the one-period interest rate and prices of zero-coupon bonds with maturities of one period and two periods. At t=3, you are provided with the one-period interest rate and prices of zero-coupon bonds with maturity of one period.

Calculate the price of a two-period floor (depicted below by a rectangle) with an exercise rate of 9 percent. The underlying is the one-period rate.

6.25% 0.9412 0.8699 0.8046 0.7450 9.82% 0.9106 0.8297 0.7565 6.62% 0.9379 0.8802 0.8266 11.40% 0.8977 0.8063 8.16% 0.9246 0.8553 5.01% 0.9523 0.9074 13.00% 0.8850 m 9.72% 0.9114 6.52% 0.9388 3.42% 0.9669

Step by Step Solution

There are 3 Steps involved in it

Step: 1

The price of a twoperiod floor with an exercise rate of 9 is the amount of money that the holder of ...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Calculus

Authors: Dale Varberg, Edwin J. Purcell, Steven E. Rigdon

9th edition

131429248, 978-0131429246