Question

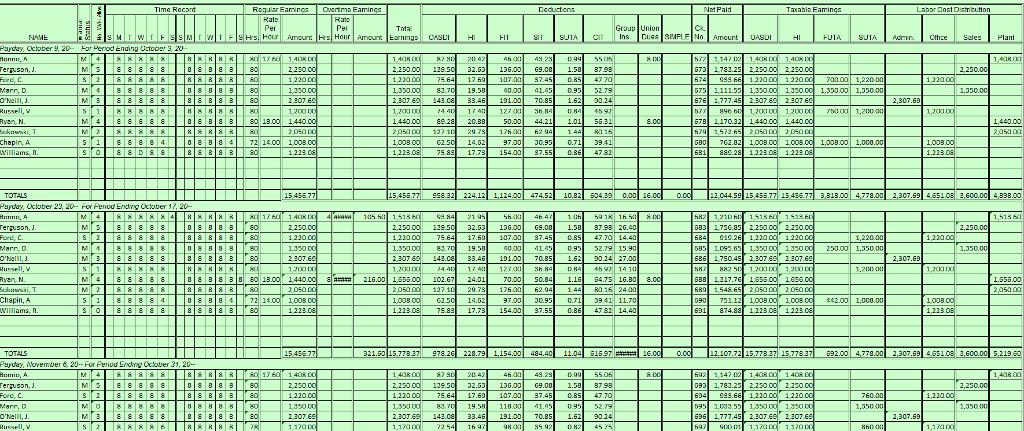

The first payroll in October covered the two workweeks that ended on September 26 and October 3. This payroll transaction has been entered for you

The first payroll in October covered the two workweeks that ended on September 26 and October 3. This payroll transaction has been entered for you in the payroll register, the employees' earnings records, the general journal, and the general ledger. By reviewing the calculations of the wages and deductions in the payroll register and the posting of the information to the employees' earnings records, you can see the procedure to be followed each payday.

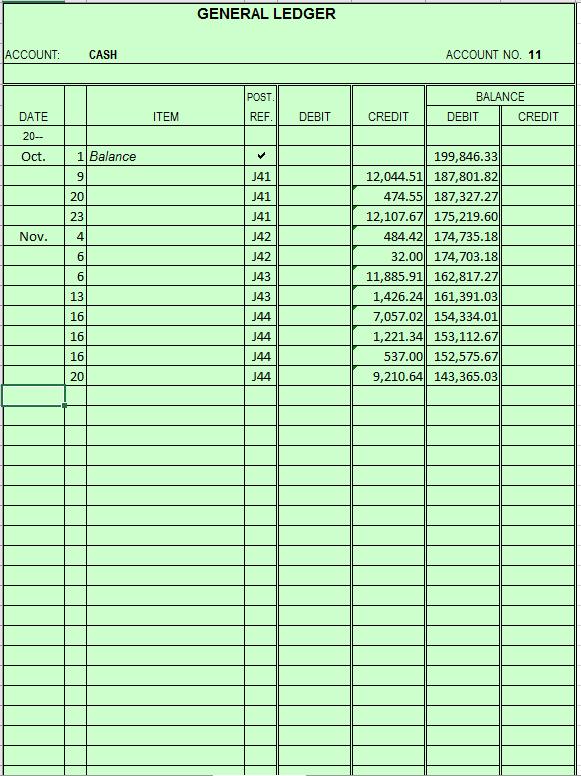

Wages and salaries are paid by issuing special payroll checks. When the bank on which they are drawn receives such checks, they will be charged against the payroll cash account.

Observe the following rules in computing earnings each pay period:

Do not make any deduction from an employee's earnings if the employee loses less than 15 minutes of time in any day. Time lost that exceeds 15 minutes is rounded to the nearest quarter-hour and deducted. If the time lost by an employee is not to be deducted, the time clerk will make a notation to that effect on the Time Clerk's Report.

In completing the time record columns of the payroll register for all workers, you should place an 8 in the day column for each full day worked. If an employee works less than a full day, show the actual hours for which the employee will be paid.

In the case of an employee who begins work during a pay period, compute the earnings by paying the employees their weekly rate for any full week worked. For any partial week, compute the earnings for that week by multiplying the hours worked by the hourly rate of pay.

If time lost is to be deducted from a salaried employee's pay, the employee's pay must be determined by multiplying the actual hours worked for that week by the hourly rate. If hours are missed but no pay is deducted, include those hours in the Time Record columns on the payroll register. The following schedule shows the weekly and hourly wage rates of the salaried employees:

Plant workers (Bonno and Ryan), other than supervisors, are employed on an hourly basis. Compute the wages by multiplying the number of hours worked during the pay period by the employee's hourly rate.

The information needed and the sequence of steps that are completed for the payroll are presented in the following discussion.

The time clerk prepared Time Clerk's Report Nos. 38 and 39 from the time cards used by the employees for these workweeks. Inasmuch as the president, sales manager, sales representatives, and supervisors do not ring in and out on the time clock, their records are not included in the time clerks report, but their salaries must be included in the payroll.

① The following schedule shows the hourly wage rates of the three hourly employees used in preparing the payroll register for the payday on October 9.

Pay Points

Tax calculations are to be taken to three decimal places and then rounded to two places.

② The entry required for each employee is recorded in the payroll register. The names of all employees are listed in alphabetical order, including yours as “Student.” The fold-out payroll register forms needed to complete this project are in the Payroll Register.

No deduction has been made for the time lost by Williams. Thus, the total number of hours (80) for which payment was made is recorded in the Regular Earnings Hours column of the payroll register. However, a notation of the time lost (D) was made in the Time Record column. When posting to Williams's earnings record, 80 hours is recorded in the Regular Earnings Hours column (no deduction for the time lost).

In computing the federal income taxes to be withheld, use wage-bracket tables.

Each payday, $8 was deducted from the earnings of the two plant workers for union dues (Bonno and Ryan).

Pay Points

Use tax tables for biweekly payroll period.

Payroll check numbers were assigned beginning with check no. 672.

In the Labor Cost Distribution columns at the extreme right of the payroll register, each employee's gross earnings were recorded in the column that identifies the department in which the employee regularly works. The totals of the Labor Cost Distribution columns provide the amounts to be charged to the appropriate salary and wage expense accounts and aid department managers and supervisors in comparing the actual labor costs with the budgeted amounts.

Once the net pay of each employee was computed, all the amount columns in the payroll register were footed, proved, and ruled.

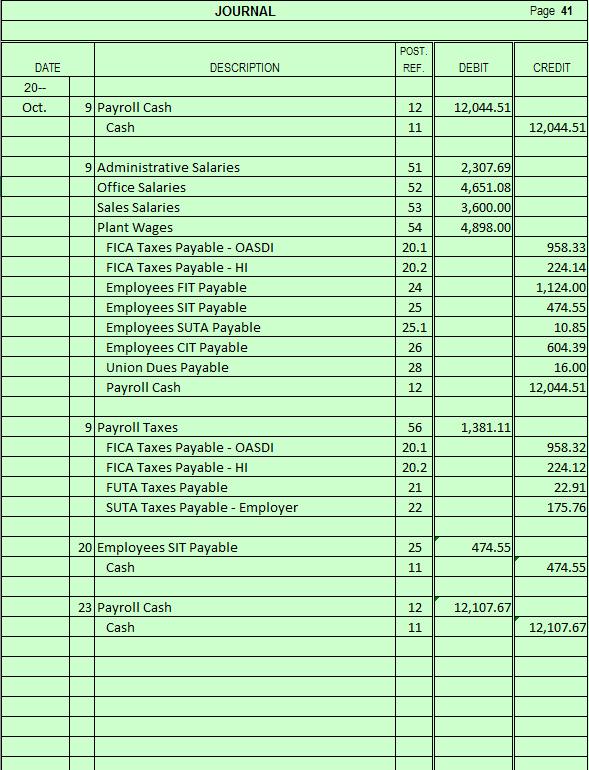

③ An entry was made in the journal transferring from the regular cash account to the payroll cash account the amount of the check issued to Payroll to cover the net amount of the payroll; next, the entry was posted.

④ Information from the payroll register was posted to the employees' earnings records.

Note that when posting the deductions for each employee, a column has been provided in the earnings record for recording each deduction for FICA (OASDI and HI), FIT, SIT, SUTA, and CIT. All other deductions for each employee are to be totaled and recorded as one amount in the Other Deductions column. Subsidiary ledgers are maintained for Group Insurance Premiums Collected and Union Dues Withheld. Thus, any question about the amounts withheld from an employee's earnings may be answered by referring to the appropriate subsidiary ledger. In this project, your work will not involve any recording in or reference to the subsidiary ledgers.

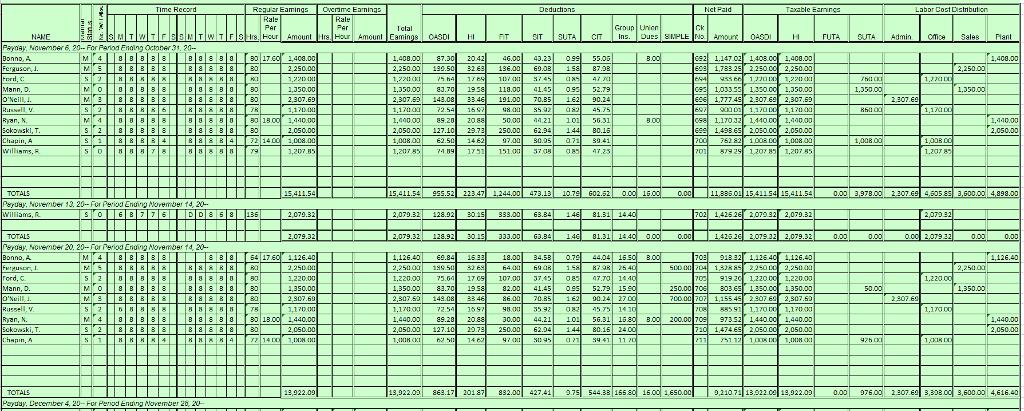

⑤ The proper journal entry recorded salaries, wages, taxes, and the net amount of cash paid from the totals of the payroll register. The journal entry to record the payroll for the first pay in the fourth quarter appears below and in the general journal.

The amounts charged the salary and wage expense accounts were obtained from the totals of the Labor Cost Distribution columns in the payroll register. As shown in the listing of the labor cost accounts in Figure 7.5 the salaries and wages were charged as follows:

Figure 7.5

FICA Taxes Payable—OASDI and FICA Taxes Payable—HI were credited for $958.57 and $224.19, respectively, the amounts deducted from employees' wages.

Employees FIT Payable, Employees SIT Payable, Employees SUTA Payable, Employees CIT Payable, and Union Dues Payable were credited for the total amount withheld for each kind of deduction from employees' wages. In subsequent payroll transactions, Group Insurance Premiums Collected will be credited for the amounts withheld from employees' wages for this type of deduction. Finally, Payroll Cash was credited for the sum of the net amounts paid all employees.

⑥ The payroll taxes for this pay were then recorded in the general journal as follows:

Payroll Taxes was debited for the sum of the employer's FICA, FUTA, and SUTA taxes. The taxable earnings used in computing each of these payroll taxes were obtained from the appropriate column totals of the payroll register. Note that only part of Ford's wages are taxable ($700 out of $1,220 gross pay) for FUTA ($7,000 limit). The computation of the debit to Payroll Taxes was:

FICA Taxes Payable—OASDI was credited for $958.57, the amount of the liability for the employer's portion of the tax. FICA Taxes Payable—HI was credited for $224.18, the amount of the liability for the employer's share of this tax. FUTA Taxes Payable was credited for the amount of the tax on the employer for federal unemployment purposes ($22.91). SUTA Taxes Payable—Employer was credited for $175.76, which is the amount of the contribution required of the employer under the state unemployment compensation law.

⑦ The journal entries were posted to the proper ledger accounts.

October 15

This is the day on which the deposits of FICA and FIT taxes and the city of Philadelphia income taxes for the September payrolls are due. However, in order to concentrate on the fourth-quarter payrolls, we will assume that the deposits for the third quarter and the appropriate entries were already completed.

October 20

No. 2 On this date, Glo-Brite Paint Company must deposit the Pennsylvania state income taxes withheld from the October 9 payroll.

The deposit rule states that if the employer expects the aggregate amount withheld each quarter to be $1,000 or more, the employer must pay the withheld tax semimonthly.

The tax must be remitted within three banking days after the close of the semimonthly periods ending on the 15th and the last day of the month.

① Prepare the journal entry to record the deposit of the taxes, and post to the appropriate ledger accounts.

② Pennsylvania has eliminated the filing of paper forms (replaced by telefile or online filing). The information needed to telefile is listed—complete the information worksheet needed for the first semimonthly period of October. The company's Pennsylvania employer account number is 000-0-3300, its EIN is 00-0000660, its filing password is GBPCOM, and its telephone number is (215) 555-9559.

October 23

Pay Points

Even though they are not on the time clerk's report, remember to pay the president, sales manager, sales representatives, and supervisors.

No. 3 Prepare the payroll for the last pay period of October from Time Clerk's Report Nos. 40 and 41.

The proper procedure in recording the payroll follows:

① Complete the payroll register.

In as much as only a portion of the payroll register sheet was used in recording the October 9 payroll, the October 23 payroll should be recorded on the same sheet to save space. On the first blank ruled line after the October 9 payroll, insert “Payday October 23—For Period Ending October 17, 20--.” On the following lines, record the payroll information for the last pay date of October. When recording succeeding payrolls, continue to conserve space by recording two payrolls on each separate payroll register sheet.

The workers in the plant (Bonno and Ryan) are paid time and a half for any hours worked over eight each workday and for work on Saturdays and are paid twice the regular hourly rate for work on Sundays or holidays.

With this pay period, the cumulative earnings of several employees exceed the taxable income base set up by FUTA and SUTA. This factor must be considered in preparing the payroll register and in computing the employer's payroll taxes. Refer to each employee's earnings record to see the amount of cumulative earnings.

② Make the entry transferring from Cash to Payroll Cash the net amount of the total payroll, and post.

③ Post the required information from the payroll register to each employee's earnings record.

④ Record in the journal the salaries, wages, taxes withheld, group insurance premiums collected, union dues withheld, and net amount paid, and post to the proper ledger accounts.

The entry required to record the October 23 payroll is the same as that to record the October 9 payroll, except it is necessary to record the liability for the amount withheld from the employees' wages to pay their part of the group insurance premium. The amount withheld should be recorded as a credit to Group Insurance Premiums Collected.

⑤ Record in the journal the employer's payroll taxes and the liabilities created; post to the appropriate ledger accounts.

November 4 2016

Pay Points

Be sure to deduct 30¢ premium for each $1,000 of group insurance carried by each employee (last payday of each month).

No. 4 Deposit with the state of Pennsylvania the amount of state income taxes withheld from the October 23 payroll and complete information worksheet.

No. 5 Virginia Russell completed a new Form W-4, changing the number of withholding allowances to 2. Change Russell's earnings record (her marital status has not changed).

No. 6 Thomas J. Sokowski completed a new Form W-4, showing that his marital status changed to single and that the number of withholding allowances remains at 2. Change Sokowski's earnings record accordingly.

No. 7 Dewey Mann completed a new Form W-4, leaving his marital status as married but dropping the number of withholding allowances to 0. Change Mann's earnings record accordingly.

November 6

No. 8 Pay the treasurer of the union the amount of union dues withheld during the month of October.

Pay Points

Make changes in November 6 pay. Refers to Nos. 5, 6, and 7.

No. 9 Prepare the payroll for the first pay period in November from Time Clerk's Report Nos. 42 and 43 and record the paychecks issued to all employees. Record this payroll at the top of the second payroll register sheet.

Note: Virginia Russell worked only 38 hours in the week ending October 24. Therefore, compute her pay for that week by multiplying 38 by $15.00 (her hourly rate). Ruth Williams worked only 39 hours in the week ending October 24. Therefore, compute her pay for that week by multiplying 39 by $15.29 (her hourly rate).

Also, record the employer's payroll taxes.

November 13

Pay Points

Prepare a Wage and Tax Statement, Form W-2, to be given to Williams.

No. 10 Because of her excessive tardiness and absenteeism during the year, the company discharged Ruth Williams today. For the week ending November 7, she was late a total of six hours; and for this week, she missed two full days and was late two hours on another day. In lieu of two weeks' notice, Williams was given two full weeks' pay ($1,223.08). Along with her dismissal pay ($1,223.08), she was paid for the week ending November 7 (34 hours, or $519.86) and the days worked this current week (22 hours, or $336.38). The total pay for the two partial weeks is $856.24.

① Record a separate payroll register (on one line) to show Williams's total earnings, deductions, and net pay. The two weeks' dismissal pay is subject to all payroll taxes. Include dismissal pay with the total earnings but do not show the hours in the Time Record columns. Use the tax table for the biweekly payroll period for the total gross pay ($2,079.32) of Williams.

The deduction for group insurance premiums is $14.40. In the Time Record column, make a note of Williams's discharge as of this date. Indicate the payroll check number used to prepare the final check for Williams. When posting to the earnings record, make a notation of Williams's discharge on this date.

② Prepare the journal entries to transfer the net cash and to record Williams's final pay and the employer's payroll taxes. Post to the ledger accounts.

③ Use the blank Form W-2. Box “a” should be left blank, since the Glo-Brite Paint Company does not use a control number to identify individual Forms W-2.

November 16

No. 11 Electronically deposit the amount of FICA taxes and federal income taxes for the October payrolls and complete the Federal Deposit Information Worksheet. Since the company is subject to the monthly deposit rule, the deposit is due on the 15th of the following month. See the deposit requirements explained. November 15 is a Sunday; therefore, the deposit is to be made on the next business day.

Prepare the journal entry to record the deposit of the taxes, and post to the appropriate ledger accounts.

No. 12 Since Glo-Brite Paint Company withholds the city of Philadelphia income tax, you must deposit the taxes with the Department of Revenue. The deposit rule that affects Glo-Brite Paint Company states that if the withheld taxes are between $350 and $16,000 per month, the company must deposit the tax monthly by the 15th of the following month. The withheld taxes for the October payrolls were $1,224.72.

Pay Points

On all tax and deposit forms requiring a signature, use Joseph O'Neill's name.

① Prepare the journal entry to record the deposit of the taxes, and post to the appropriate ledger accounts.

② Complete the Philadelphia Employer's Return of Tax Withheld coupon (Monthly Wage Tax), which appears.

November 17

No. 13 Prepare an employee's earnings record for Beth Anne Woods, a new employee who began work today, Tuesday. Woods is single and claims one withholding allowance. She is employed as a programmer at a monthly salary of $2,600. Address, 8102 Franklin Court, Philadelphia, PA 19105-0915. Telephone, 555-1128. Social Security No. 000-00-1587. She is eligible for group insurance coverage of $47,000 immediately, although her first deduction for group insurance will not be made until December 18.

Department: Office

Weekly rate: $600.00

Hourly rate: $15.00

November 18

No. 14 Deposit with the state of Pennsylvania the amount of state income taxes withheld from the November 6 and 13 (Ruth Williams) payrolls and complete the information worksheet.

November 20

Pay Points

Remember to deduct the premiums on the group insurance for each employee.

No. 15 With this pay, the company has decided to offer employees a Savings Incentive Match Plan (SIMPLE Retirement Plan). Most of the employees opted to wait until the start of the following year to participate. However, the following employees have decided to take part in the plan for the remaining pay periods of the year.

A two-column list of employees and their Savings Incentive Match Plan contributions. The information in the table is as follows: James Ferguson:; $500 contribution per pay period. Dewey Mann:; $250 contribution per pay period. Joseph O'Neill:; $700 contribution per pay period. Norman Ryan:; $200 contribution per pay period.

The contributions are to be deducted from the participating employee's pay and are excluded from the employee's income for federal income tax purposes. The other payroll taxes still apply. On the payroll registers and the earnings record, use the blank column under “Deductions” for these contributions. Use the term “SIMPLE” as the new heading for this deduction column (on both the payroll register and employee's earnings record).

Use the account in the general ledger for SIMPLE Contributions Payable—account no. 29.

The company must match these contributions dollar for dollar, up to 3 percent of the employee's compensation. These payments will be processed through the Accounts Payable Department.

Prepare the payroll for the last pay period of November from Time Clerk's Report Nos. 44 and 45, and record the paychecks issued all employees. Also, record the employer's payroll taxes.

Pay Points

The new wage rates are effective for the December 4 payroll.

No. 16 Salary increases of $30 per week, effective for the two weeks covered in the December 4 payroll, are given to Catherine L. Ford and Virginia A. Russell. The group insurance coverage for Ford will be increased to $50,000; for Russell, it will be increased to $49,000. Update the employees' earnings records accordingly. The new wage rates are listed below.

November 30

No. 17 Prepare an employee's earnings record for Paul Winston Young, the president's nephew, who began work today. Young is single and claims one withholding allowance. He is training as a field sales representative in the city where the home office is located. His beginning salary is $2,730 per month. Address, 7936 Holmes Drive, Philadelphia, PA 19107-6107. Telephone, 555-2096. Social Security No. 000-00-6057. Young is eligible for group insurance coverage of $49,000.

Department: Sales

Weekly rate: $630.00

Hourly rate: $15.75

December 3 2016

No. 18 Deposit with the state of Pennsylvania the amount of state income taxes withheld from the November 20 payroll and complete the information worksheet.

December 4

No. 19 Prepare the payroll for the first pay period of December from Time Clerk's Report Nos. 46 and 47, and record the paychecks issued all employees. Record this payroll at the top of the third payroll register sheet.

Note: Thursday, November 26, is a paid holiday for all workers.

Also, record the employer's payroll taxes.

No. 20 Anthony V. Bonno reports the birth of a son and completes an amended Form W-4, showing his total withholding allowances to be five. Change his earnings record accordingly, effective with the December 18 pay.

No. 21 Both Anthony Bonno and Norman Ryan have been notified that their union dues will increase to $9 per pay, starting with the last pay period of the year. Reflect these increases in the December 18 pay and show the changes on their earnings records.

December 9

No. 22 Pay the treasurer of the union the amount of union dues withheld during the month of November.

December 11

No. 23 The Payroll Department was informed that Virginia A. Russell died in an automobile accident on her way home from work Thursday, December 10.

December 14

Pay Points

This final pay is not subject to withholding for FIT, SIT, or CIT purposes.

Pay Points

Prepare a Wage and Tax Statement, Form W-2, which will be given to the executor of the estate along with the final paycheck.

No. 24 ① Make a separate entry (on one line) in the payroll register to record the issuance of a check payable to the Estate of Virginia A. Russell. This check covers Russell's work for the weeks ending December 5 and 12 ($1,134.00) plus her accrued vacation pay ($1,260.00). Do not show the vacation hours in the Time Record columns on the payroll register, but include them in the Total Earnings column.

Russell's final biweekly pay for time worked and the vacation pay are subject to FICA, FUTA, and SUTA (employer and employee) taxes. Since Russell's cumulative earnings have surpassed the taxable earnings figures established by FUTA and SUTA, there will not be any unemployment tax on the employer. The deduction for group insurance premiums is $14.70.

② Make a notation of Russell's death in the payroll register and on her earnings record.

③ Prepare journal entries to transfer the net pay and to record Russell's final pay and the employer's payroll taxes. Post to the ledger accounts.

④ Include the final gross pay ($2,394.00) in Boxes 3 and 5, but not in Boxes 1, 16, and 18. Use the blank Form W-2.

In addition, the last wage payment and vacation pay must be reported on Form 1099-MISC. A Form 1096 must also be completed. These forms will be completed in February before their due date. (See Transaction Nos. 41 and 42.)

December 15

No. 25 Electronically deposit the amount of FICA taxes and federal income taxes for the November payrolls and complete the Federal Deposit Information Worksheet.

No. 26 Deposit with the city of Philadelphia the amount of city income taxes withheld from the November payrolls.

December 18

No. 27 Deposit with the state of Pennsylvania the amount of state income taxes withheld from the December 4 payroll and complete the information worksheet.

No. 28 Glo-Brite has been notified by the insurance company that there will be no premium charge for the month of December on the policy for Virginia Russell. Prepare the entry for the check made payable to the estate of Virginia A. Russell, for the amount that was withheld for insurance from her December 14 pay.

No. 29 Prepare an employee's earnings record for Richard Lloyd Zimmerman, who was employed today as time clerk to take the place left vacant by the death of Virginia A. Russell last week. His beginning salary is $2,600 per month. Address, 900 South Clark Street, Philadelphia, PA 19195-6247. Telephone, 555-2104. Social Security No. 000-00-1502. Zimmerman is married and claims one withholding allowance. Zimmerman is eligible for group insurance coverage of $47,000, although no deduction for group insurance premiums will be made until the last payday in January.

Department: Office

Weekly rate: $600.00

Hourly rate: $15.00

Pay Points

Remember to deduct the premiums on the group insurance for each employee.

January 6

No. 31 Deposit with the state of Pennsylvania the amount of state income taxes withheld from the December 18 payroll and complete the information worksheet.

January 8

No. 32 Pay the treasurer of the union the amount of union dues withheld during the month of December.

January 15

No. 33 Electronically deposit the amount of FICA taxes and federal income taxes for the December payrolls, and complete the Federal Deposit Information Worksheet.

No. 34 Deposit with the city of Philadelphia the amount of city income taxes withheld from the December payrolls.

February 1

No. 35 Prepare Form 941, Employer's Quarterly Federal Tax Return, with respect to wages paid during the last calendar quarter. Pages 7-55 and 7-56 contain a blank Form 941. The information needed in preparing the return should be obtained from the ledger accounts, payroll registers, employees' earnings records, and Federal Tax Deposit forms.

Form 941 and all forms that follow are to be signed by the president of the company, Joseph T. O'Neill.

No. 36 ① Complete Form 940, Employer's Federal Unemployment (FUTA) Tax Return, using the blank forms reproduced. Also, complete the Federal Deposit Information Worksheet, using the blank form reproduced.

Total wages for the first three quarters was $142,224.57. FUTA taxable wages for the first three quarters was $65,490.00.

FUTA tax liability by quarter:

1st quarter—$204.53

2nd quarter—$105.25

3rd quarter—$83.16

The first FUTA deposit is now due.

Journalize the entry to record the electronic deposit for the FUTA tax liability.

No. 37 ① Prepare Form UC-2, Employer's Report for Unemployment Compensation—Fourth Quarter, using the blank form reproduced. In Pennsylvania, a credit week is any calendar week during the quarter in which the employee earned at least $50 (without regard to when paid). The maximum number of credit weeks in a quarter is 13. The telephone number of the company is (215) 555-9559. All other information needed in preparing the form can be obtained from the ledger accounts, the payroll registers, and the employees' earnings records.

② Journalize the entry to record the payment of the taxes for the fourth quarter.

Time Record Requiar Earnings Overtime Eamings Net Paid Taxabis Earrints Labor Cost Distribution Rate Rate Per Per Total C WTFSSMTWTFSHs WI-SHrs. Hour Hour Amount Hrs Hour Amount Earnings OASCI HI FIT SIT SUTA CI Dues SIMPLE No Amount OASDI HI FUTA SUIA Admin. Office Sales Plant 80 1760 1408 DO 87 30 800 1,408 00 572 1,147 02 1,408 00 1,408 DO 673 1,783.25 2.250.00 2.250.00 ] [N y 88888 80 8888 80 B 08 88888 80 88888 80 2.250.00 122000 1,350.00 2.307.60 88888 80 1,200 00 88888 80 18.00 1440.00 88RR 80 2050.00 2,250.00 1,220 00 1,350.00 40.00 41.45 0.95 191.00 70.85 1.62 1,408.00 20:42 46:00 099 43.25 55.05 2.250.00 139.50 32.63 136.00 69.08 1.58 87.98 1,22000 75.64 17.69 107.00 97.45 0.85 47.70 1,350.00 83.70 19.58 52.79 2,307.60 143.08 33.46 90.24 1,20000 74 407 17.40 4592 89.28 1,440.00 20.88 50.00 44.21 1.01 56.31 2,050.00 127 1 29.75 176.00 62.94 1.44 80.16 1,008.00 62.50 14.62 97.00 30.93 1,223.08 75.89 17.73 154.00 97.55 674 988.66 1220 00 1.220.00 700.00 1,220.00 575 1,111.55 1,350.00 1,350.00 1,350.00 1,350.00 571 1,777.45 2.307.60 2.307.60 577 896.60 1,200.00 1,20000 1.200.00 1440.00 1440.00 678 1,170.32 1,440.00 1440.00 679 1,572.65 205000 2,050.00 127.00 36.84 0.84 750.00 1,200,00 1,20000 8.00 1,440.00 2,050.00 88884 72 14.00 1.008.00 88888 80 1.228.08 0.71 39.41 0.86 47.82 GBO 762.82 1,008.00 1,008.00 1,008.00 1,000.00 581 880.28 1,228 08 1.228.08 1.000.00 1,223.08 15.456.77 15,455.77 956.32 224.12 1,124.00 474.52 10.82 604.39 0.00 16.00 0.00 12.044.59 15.455.77 15.456.77 3.818.00 4,778.00 2,307.69 4,651.08 3,600.00 4,898.00 59 1408 004 Ava 2.250.00 1,518 60 53 18 16 50 8 87.98 26.40 1220.00 47.70 14.40 1,220.00 1.350.00 2,250.00 1,350.00 1,220.00 250.00 1,350.00 105 50 1,513 60 2.250.00 1,220.00 1,350.00 83.70 19.58 2,307.60 143.08 33.46 74.40 17.40 216.00 1655.00 102.67 24.01 KAFKA 2,050.00 127.10 29.75 RRRRR 1760 88888 80 88888 80 Tola 88888 8 80 88888 8 80 88888 xd 8880 18.00 88888 80 88884 72 14.00 88888 99.84 21.95 56.00 46.47 1.06 139.50 32.03 136.00 69.08 1.58 75.64 17.69 107.00 37.45 0.85 40.00 41.45 0.95 191.00 70.85 1.62 12700 Sh 84 D84 70.00 50.84 1.16 176.00 62.94 1.44 52.79 15.90 90.24 27.00 582 1,210 60 151560 1518 60 683 1,756.85 2.250.00 2.250.00 584 910.26 1.220.00 1.220.00 585 1,095.65 1.350.00 1,350.00 686 1,750.45 2.307.65 2.207.65 587 882 50 1,20000 120000 688 1,317.76 1,656.00 1656.00 2.307.60 120000 1,20000 45 92 14 10 1,200.00 1,200 000 1440.00 samm 64.75 16.00 8.00 Dave L40:00 80.16 24.00 2,050.00 1.555.00 2,050.00 1.008.00 1,008.00 02.50 14.02 97.00 30.95 0.71 39.41 11.70 680 1,548.65 2,050.00 2.050.00 751.12 1,008.00 1,008.00 874.88 1,223.08 1.228.08 442.00 1,000.00 090 691 1,008.00 1,223.08 80 1223.08 1,223.08 75.89 17.73 154.00 37.55 0.86 47.82 14.40 ||| 15.456.77 321.50 15.778.37 978.26 228.79 1.154.00 484.40 11.04 515.97 16.00 0.00 12.107.72 15.778.37 15.778.37 692.00 4,778.00 2,307.69 4.651.08 3,600.00 5.219.60 8.00 1,408 00 2,250.00 8888 80 17 60 140 00 88888 80 2,250.00 88888 80 1,220.00 8880 1,350.00 8888880 2.307.69 RRRR 78 88888 1,40R 00 87.90 20.42 2.250.00 139.50 32.03 1,220.00 75.64 17.69 1.350.00 83.71 19.58 2,307.69 143.08 33.46 1,17000 72 54 16:47 1,220.00 46.00 48.25 0.99 55.06 136.00 69.00 1.50 87.98 107.00 97.45 0.85 47.70 118.00 41.45 0.95 52.79 191.00 70.85 1.62 90.24 98 00 55.92 0.82 45.75 692 1,147.00 1,408 00 1 408 00 093 1,783.25 2.250.00 2.250.00 694 099.66 1,220.00 1220.00 595 1,033.55 135000 1.350.00 696 1,777.45 2,307.69 2.307.69 597 900 01 1,17000 117000 760.00 1,350.00 8 1,350.00 117000 860 00 1,17000 Deductions NAME SMTWTF Payday, October 9, 20 Monne, A For Perod Ending October 3, 20 M 4 81 MS 8: S2 81 188 88 Ferguson, J. Ford, C Marr, D. M 4 O'Neill, J. M 3 88 8 Russell, V Ryan, N. Sokowski, T. S 1 Ak M 4 M 2 88 5 1 88 4 Chapin, A Williams, I. S 0 88 D88 J T TOTALS Payday, October 23, 20- For Period Ending October 17, 20- Bann, A M4 MS 88 Ferguson, J. Ford, C. S2 Marr, D. M 4 8888 O'Neill, J. M 3 S 1 88 Russell, V Ryan, N. Sokowski, T. M 4 88888 M 2 5 1 Chapin, A Williams, R. 8888 4 88888 S 0 T T I TOTALS Payday, November 6, 20-For Period Ending October 21, 20- Bonno, A. Terguson, J. Ford, C. M4 ** M5 8888 S2 88888 MO 88888 M 3 88888 S2 ****6 Marr, D O'Neill, J. Russell, V Group Union Ins 2,307.60 2,307.69 2,307.69

Step by Step Solution

3.38 Rating (151 Votes )

There are 3 Steps involved in it

Step: 1

Ans The more time we spend at work the less time we have for other important things in life Research suggests that working excessively long hours usua...

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Statistical Techniques In Business And Economics

Authors: Douglas Lind, William Marchal

16th Edition

78020522, 978-0078020520