Answered step by step

Verified Expert Solution

Question

1 Approved Answer

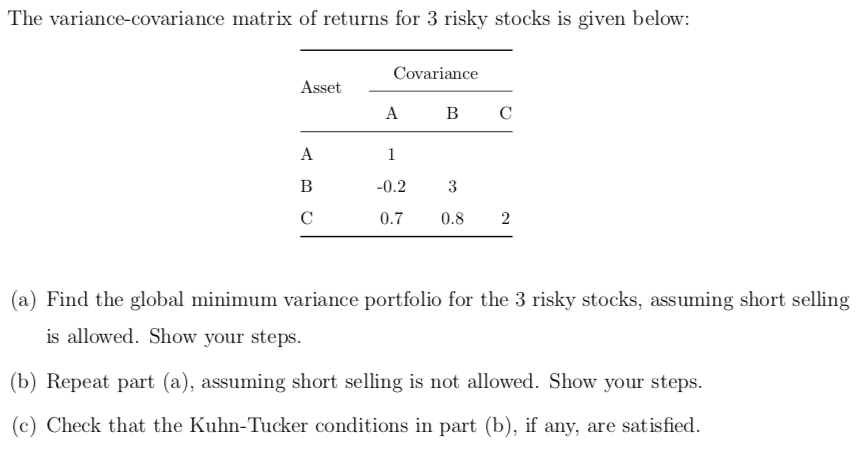

The variance-covariance matrix of returns for 3 risky stocks is given below: (a) Find the global minimum variance portfolio for the 3 risky stocks, assuming

The variance-covariance matrix of returns for 3 risky stocks is given below: (a) Find the global minimum variance portfolio for the 3 risky stocks, assuming short selling is allowed. Show your steps. (b) Repeat part (a), assuming short selling is not allowed. Show your steps. (c) Check that the Kuhn-Tucker conditions in part (b), if any, are satisfied

The variance-covariance matrix of returns for 3 risky stocks is given below: (a) Find the global minimum variance portfolio for the 3 risky stocks, assuming short selling is allowed. Show your steps. (b) Repeat part (a), assuming short selling is not allowed. Show your steps. (c) Check that the Kuhn-Tucker conditions in part (b), if any, are satisfied Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Microfinance Handbook An Institutional And Financial Perspective

Authors: Joanna Ledgerwood

1st Edition

0821343068, 978-0821343067