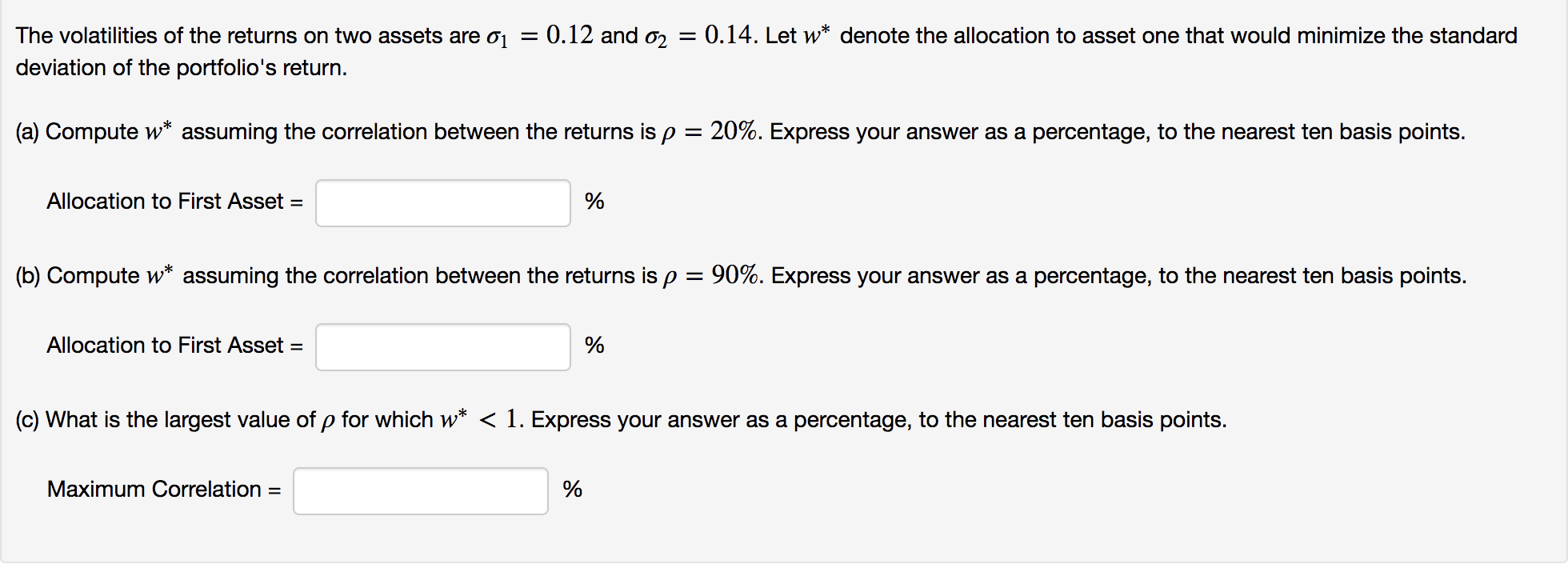

The volatilities of the returns on two assets are = = 0.12 and = 0.14. Let w* denote the allocation to asset one that

The volatilities of the returns on two assets are = = 0.12 and = 0.14. Let w* denote the allocation to asset one that would minimize the standard deviation of the portfolio's return. (a) Compute w* assuming the correlation between the returns is p = 20%. Express your answer as a percentage, to the nearest ten basis points. Allocation to First Asset = (b) Compute w* assuming the correlation between the returns is p = Allocation to First Asset = % Maximum Correlation = % % (c) What is the largest value of p for which w* < 1. Express your answer as a percentage, to the nearest ten basis points. 90%. Express your answer as a percentage, to the nearest ten basis points.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Calculating Optimal Portfolio Weights and Maximum Correlation We can use Modern Portfolio Theory MPT ...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Bruce Bowerman, Richard O'Connell

6th Edition

0073401838, 978-0073401836