Answered step by step

Verified Expert Solution

Question

1 Approved Answer

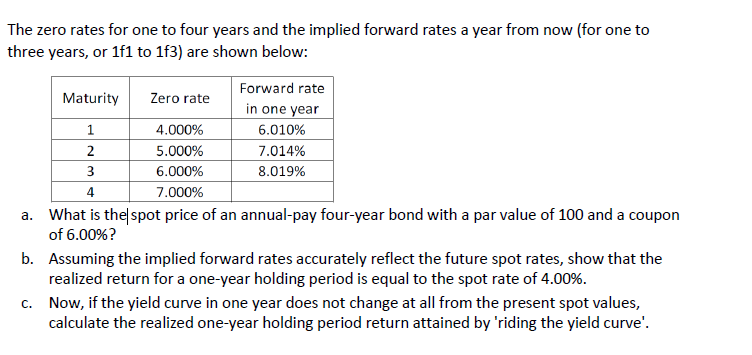

The zero rates for one to four years and the implied forward rates a year from now ( for one to three years, or 1

The zero rates for one to four years and the implied forward rates a year from now for one to

three years, or to are shown below:

a What is thelspot price of an annualpay fouryear bond with a par value of and a coupon

of

b Assuming the implied forward rates accurately reflect the future spot rates, show that the

realized return for a oneyear holding period is equal to the spot rate of

c Now, if the yield curve in one year does not change at all from the present spot values,

calculate the realized oneyear holding period return attained by 'riding the yield curve'.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Essentials Of Investments

Authors: Zvi Bodie, Alex Kane, Alan Marcus

11th Edition

1260288390, 978-1260288391