Answered step by step

Verified Expert Solution

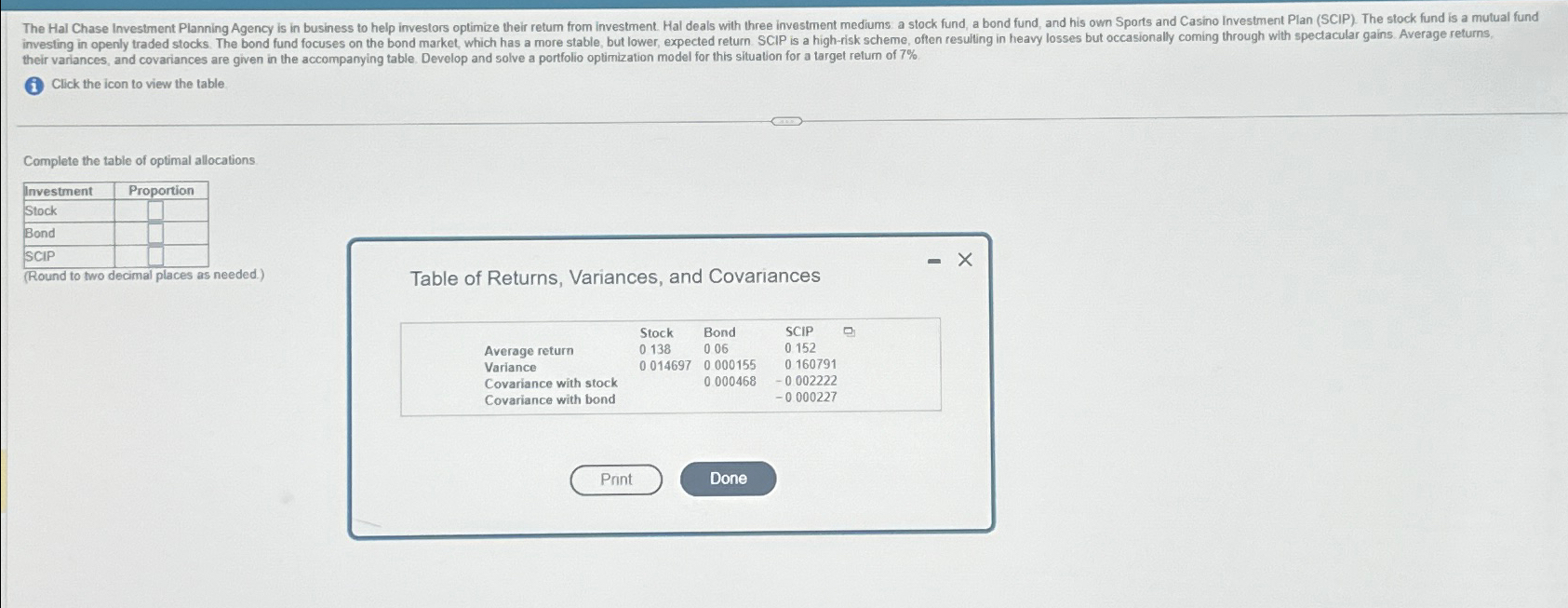

Question

1 Approved Answer

their variances, and covariances are given in the accompanying table. Develop and solve a portfolio optimization model for this situation for a target relum of

their variances, and covariances are given in the accompanying table. Develop and solve a portfolio optimization model for this situation for a target relum of

Click the icon to view the table

Complete the table of optimal allocations

tableInvestmentProportionStock

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

History Of Financial Institutions Essays On The History Of European Finance 1800–1950

Authors: Carmen Hofmann , Martin L. Müller

1st Edition

1138325007, 978-1138325005