Answered step by step

Verified Expert Solution

Question

1 Approved Answer

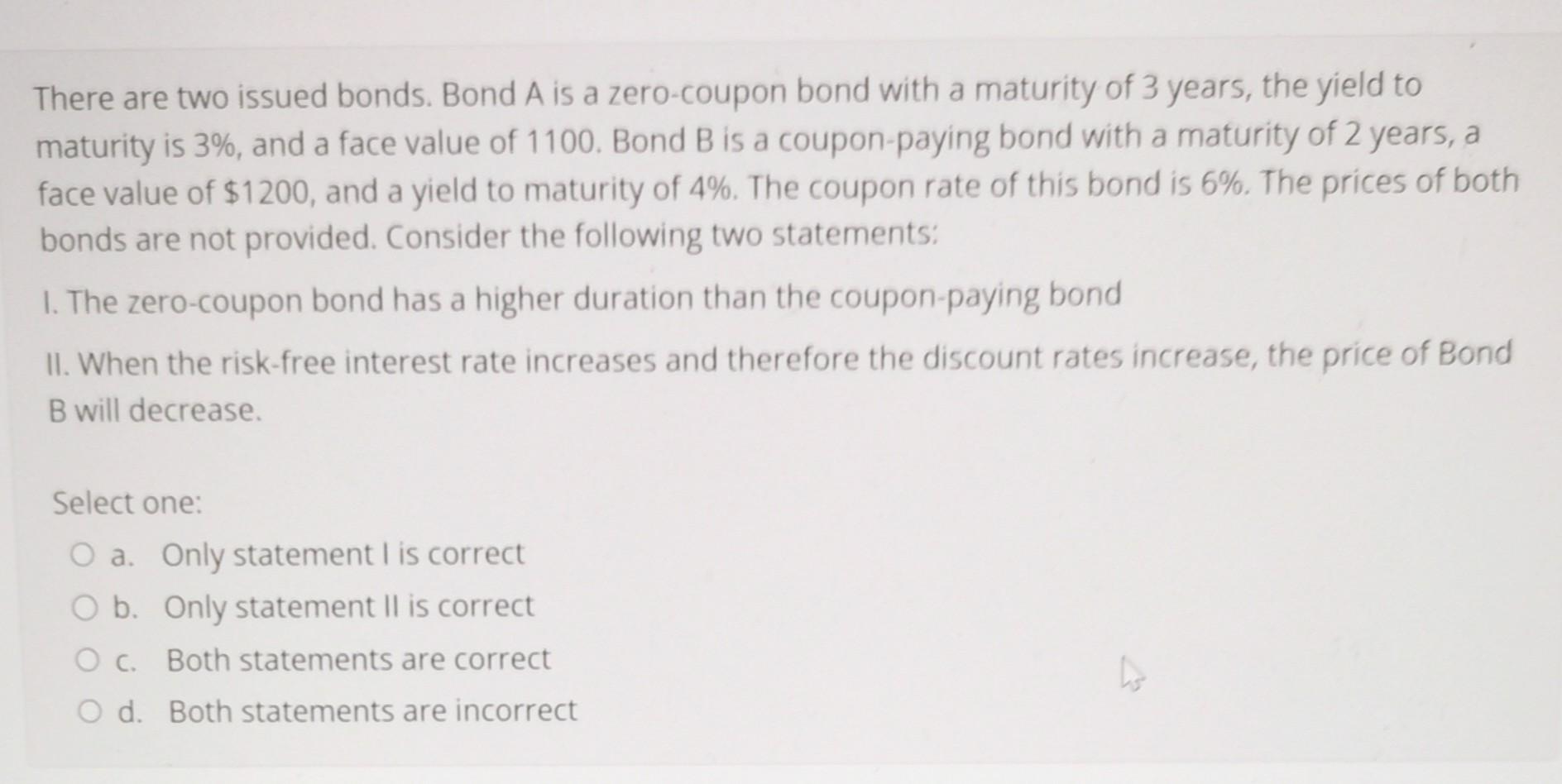

There are two issued bonds. Bond A is a zero-coupon bond with a maturity of 3 years, the yield to maturity is 3%, and a

There are two issued bonds. Bond A is a zero-coupon bond with a maturity of 3 years, the yield to maturity is 3%, and a face value of 1100 . Bond B is a coupon-paying bond with a maturity of 2 years, a face value of $1200, and a yield to maturity of 4%. The coupon rate of this bond is 6%. The prices of both bonds are not provided. Consider the following two statements: I. The zero-coupon bond has a higher duration than the coupon-paying bond II. When the risk-free interest rate increases and therefore the discount rates increase, the price of Bond B will decrease. Select one: a. Only statement 1 is correct b. Only statement II is correct c. Both statements are correct d. Both statements are incorrect

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Handbook Of Energy Trading

Authors: Stefano Fiorenzani, Samuele Ravelli, Enrico Edoli

1st Edition

1119953693, 978-1119953692