Question

There are two risky assets, D and E . The expected returns of D and E are 8% and 12%, respectively. The standard deviation of

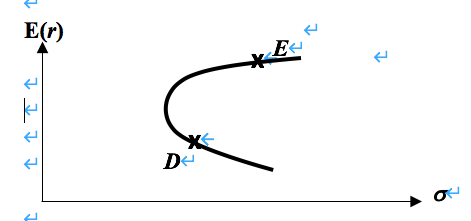

There are two risky assets, D and E. The expected returns of D and E are 8% and 12%, respectively. The standard deviation of D and E are 10% and 25%, respectively. The correlation between the assets is positive and less than 1.

(a)Suppose an investor is indifferent between holding 100% in D and holding 100% in E. What is his risk aversion A?

(b) From the different combinations of D and E, you can identify the portfolio that gives you the lowest standard deviation, which is the minimum variance portfolio, A. Can A, D, and E lie on the same utility indifference curve for the investor in part (a)? Briefly explain. (No calculations necessary.) (Hint: Consider the portfolio opportunity set, shown below).

a D

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Nurse Managers Guide To Budgeting And Finance

Authors: Al Rundio

2nd Edition

1940446589, 978-1940446585