Answered step by step

Verified Expert Solution

Question

1 Approved Answer

there is nothing to update. everything is in the question. Suppose you are expecting the stock price to move substantially over the next three months.

there is nothing to update. everything is in the question.

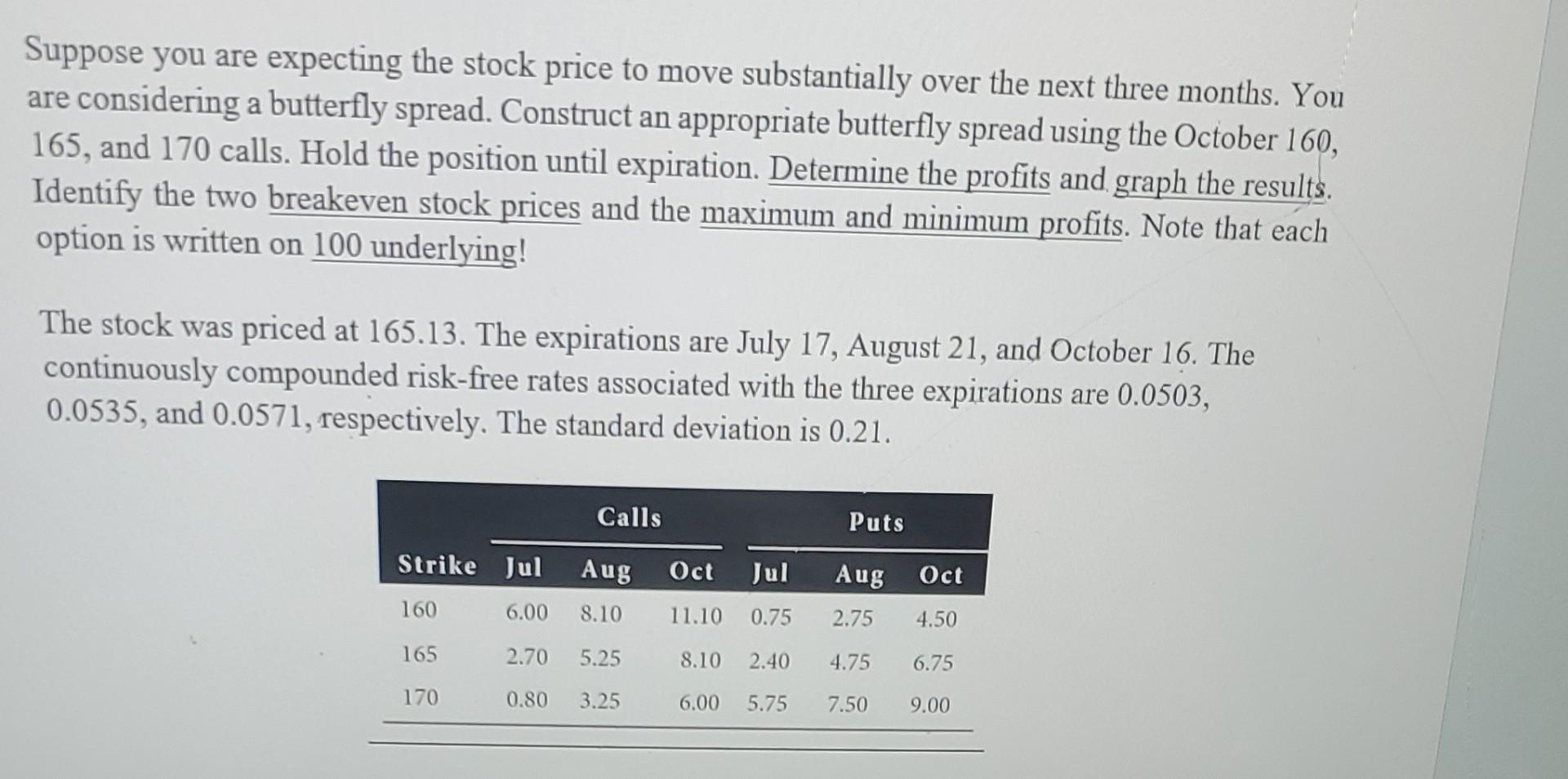

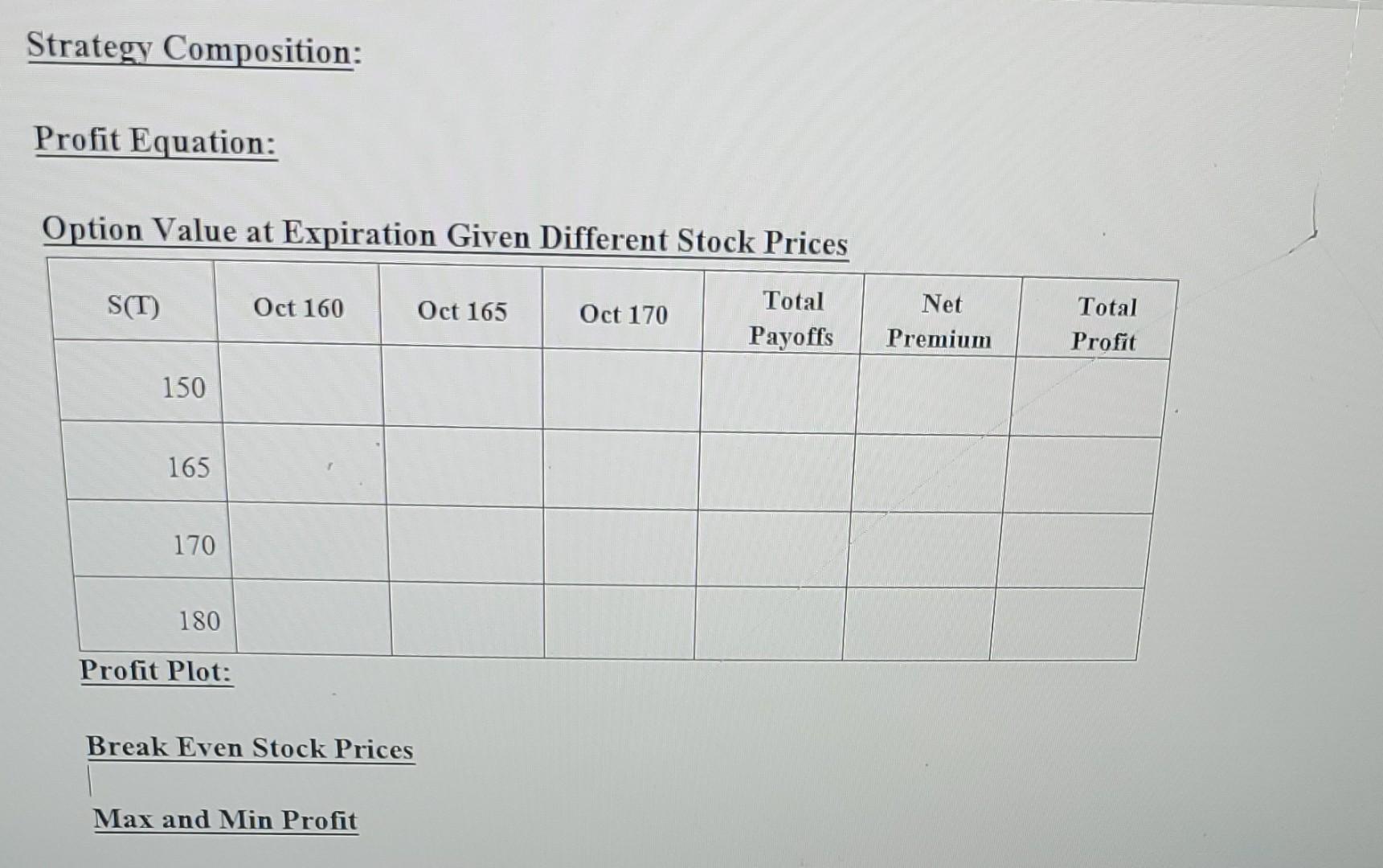

Suppose you are expecting the stock price to move substantially over the next three months. You are considering a butterfly spread. Construct an appropriate butterfly spread using the October 160, 165, and 170 calls. Hold the position until expiration. Determine the profits and graph the results. Identify the two breakeven stock prices and the maximum and minimum profits. Note that each option is written on 100 underlying! The stock was priced at 165.13. The expirations are July 17, August 21, and October 16. The continuously compounded risk-free rates associated with the three expirations are 0.0503, 0.0535, and 0.0571, respectively. The standard deviation is 0.21. Option Value at Expiration Given Different Stock Prices BreakEvenStockPrices Max and Min ProfitStep by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Asymptotic Chaos Expansions In Finance Theory And Practice

Authors: David Nicolay

2014 Edition

1447165055, 9781447165057