Answered step by step

Verified Expert Solution

Question

1 Approved Answer

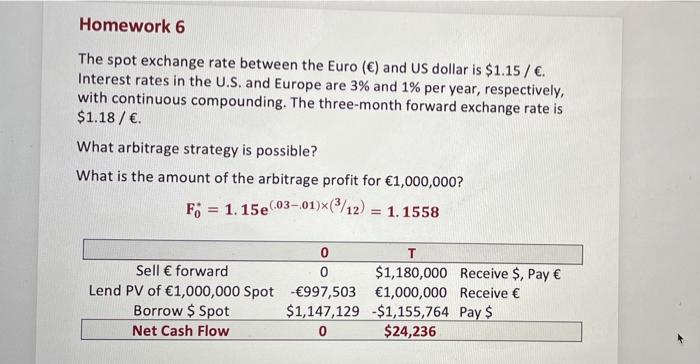

These are the answers but what are the calculations to get these numbers? Homework 6 The spot exchange rate between the Euro () and US

These are the answers but what are the calculations to get these numbers?

Homework 6 The spot exchange rate between the Euro () and US dollar is $1.15 / . Interest rates in the U.S. and Europe are 3% and 1% per year, respectively, with continuous compounding. The three-month forward exchange rate is $1.18 / . What arbitrage strategy is possible? What is the amount of the arbitrage profit for 1,000,000? F = 1.15e eC03-01/12) = 1.1558 0 T Sell forward 0 $1,180,000 Receive $, Pay Lend PV of 1,000,000 Spot 997,503 1,000,000 Receive Borrow $ Spot $1,147,129 $1,155,764 Pay $ Net Cash Flow 0 $24,236 Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Wealth Mastery Unveiled By Marcus M Dawson A Millennial S Guide To Financial Freedom And Success

Authors: Marcus M. Dawson

1st Edition

979-8865054313