Answered step by step

Verified Expert Solution

Question

1 Approved Answer

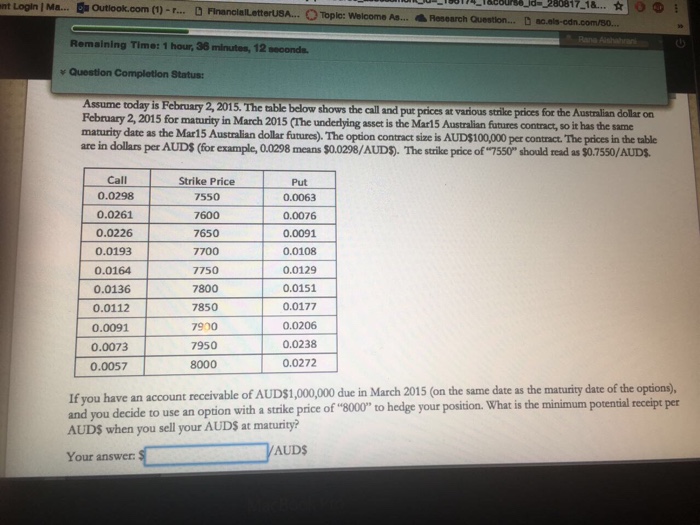

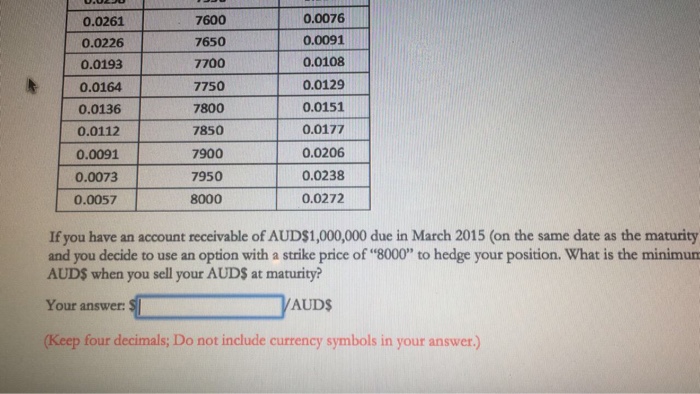

They r one question International finance Login I Ma... outlook.com 1) r D nt 80817-18... nt FinanclatuetterUSA... O Toplot welcome As... 4Research Question... Remaining Time:

They r one question

International finance

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Get Rich With Dividends

Authors: Marc Lichtenfeld

3rd Edition

1119985552, 978-1119985556