Answered step by step

Verified Expert Solution

Question

1 Approved Answer

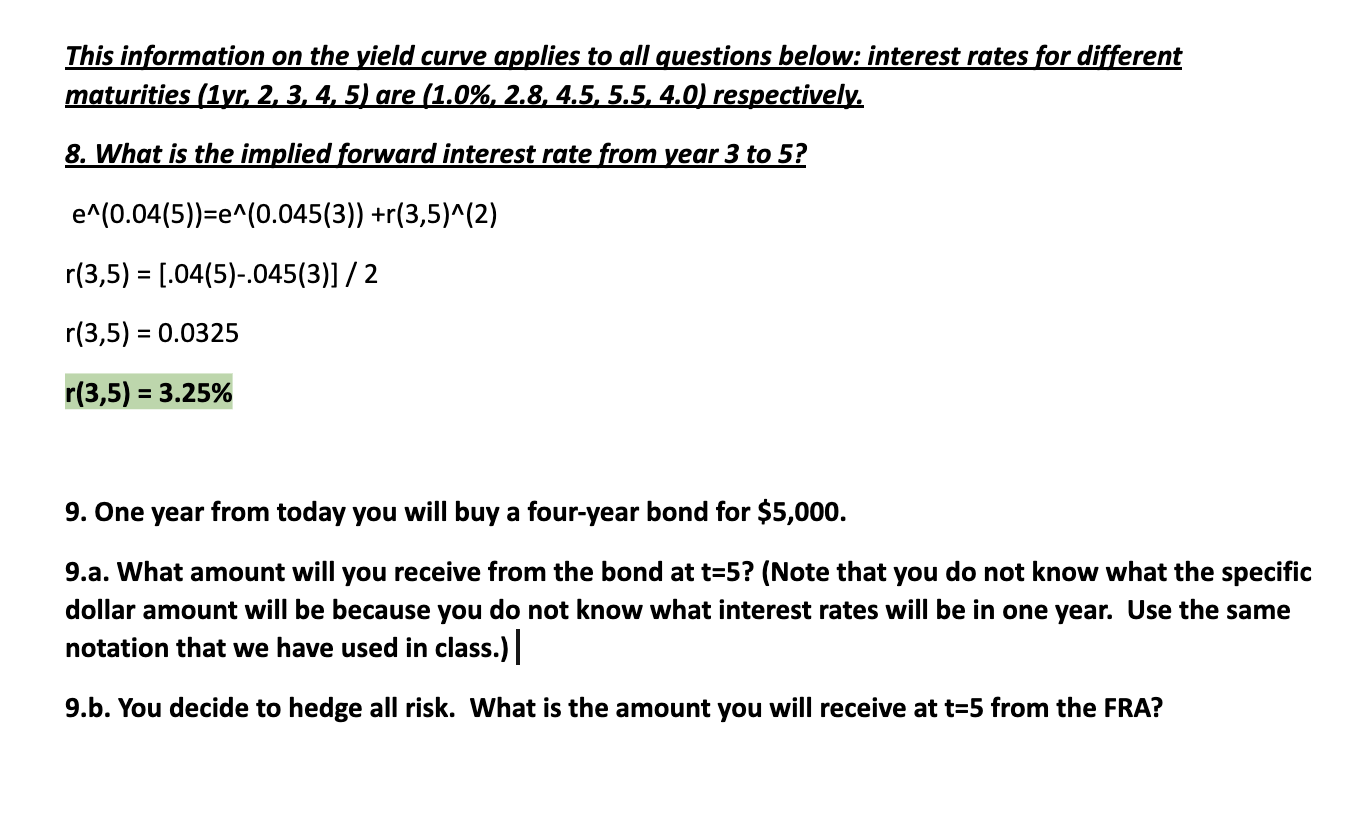

This information on the yield curve applies to all questions below: interest rates for different maturities (1yr, 2, 3, 4, 5) are (1.0%, 2.8, 4.5,

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Who Is Your Competition You Real Estate Wholesaling Questions Answers And Tools To Help Beginners Crush Their Fears And Stop Procrastinating

Authors: Nick Zalonis

1st Edition

1716097193, 978-1716097195