Answered step by step

Verified Expert Solution

Question

1 Approved Answer

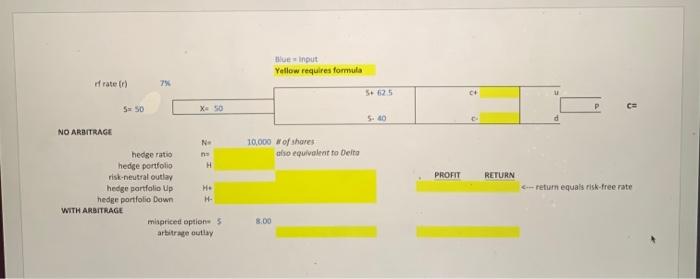

This is a binomial option pricing model. please solve for the missing solutions in the yellow. Blue input Yellow requires formula fraten 7 5 50

This is a binomial option pricing model. please solve for the missing solutions in the yellow.

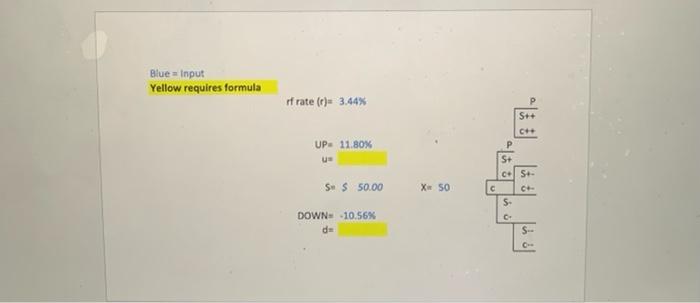

Blue input Yellow requires formula fraten 7 5 50 C= X 50 5.40 10,000 of shares also equivalent to Delta PROFIT RETURN NO ARBITRAGE N: hedge ratio ns hedge portfolio H risk-neutral outlay hedge portfolio Up He hedge portfolio Down H- WITH ARBITRAGE miapriced optione 5 arbitrage outlay return equals risk-free rate 8.00 Blue = Input Yellow requires formula rf rate (r) 3.44% P S++ C++ UP: 11.80% S+ ces S $50.00 X 50 S C DOWN 10.56% de S Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Analyzing And Forecasting Futures Prices

Authors: Anthony Herbst

1st Edition

0595142990, 978-0595142996