Question

This is a practice question in my unit - the answers that were given were: 6 month zero rate: 5.21% 1 year zero rate: 5.5%

This is a practice question in my unit - the answers that were given were:

6 month zero rate: 5.21%

1 year zero rate: 5.5%

1.5 year zero rate: 5.8%

2 year zero rate: 6%

Could please show the process and formula to arrive at the above answers - instant upvote when answered!

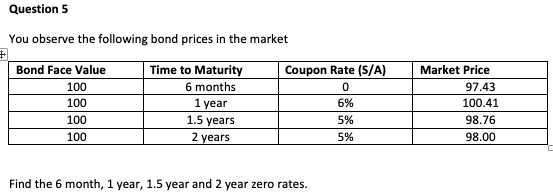

Question 5 You observe the following bond prices in the market + Bond Face Value Time to Maturity 100 6 months 100 1 year 100 1.5 years 100 2 years Find the 6 month, 1 year, 1.5 year and 2 year zero rates. Coupon Rate (S/A) 0 6% 5% 5% Market Price 97.43 100.41 98.76 98.00Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

International Finance For Dummies

Authors: Ayse Evrensel

1st Edition

111852389X, 978-1118523896