Question

***This is from Investment and Financial Mathematics (IFM) course for Actuaries. Please give handwritten solution with ALL steps shown plus with description because I need

***This is from Investment and Financial Mathematics (IFM) course for Actuaries. Please give handwritten solution with ALL steps shown plus with description because I need to understand the process. I will give "thumbs-up" for clear and correct solution. Thanks in advance!***

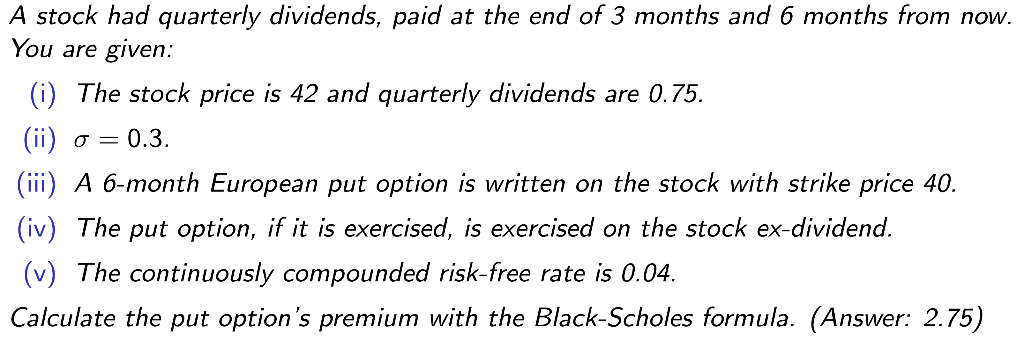

A stock had quarterly dividends, paid at the end of 3 months and 6 months from now. You are given: (i) The stock price is 42 and quarterly dividends are 0.75. (ii) O=0.3. (iii) A 6-month European put option is written on the stock with strike price 40. (iv) The put option, if it is exercised, is exercised on the stock ex-dividend. (v) The continuously compounded risk-free rate is 0.04. Calculate the put option's premium with the Black-Scholes formula. (Answer: 2.75)Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Shopify And Google Seo Masterclass 2023 Building Ecommerce Website That Sells

Authors: Ekaterina Ramishvili

1st Edition

979-8361408788