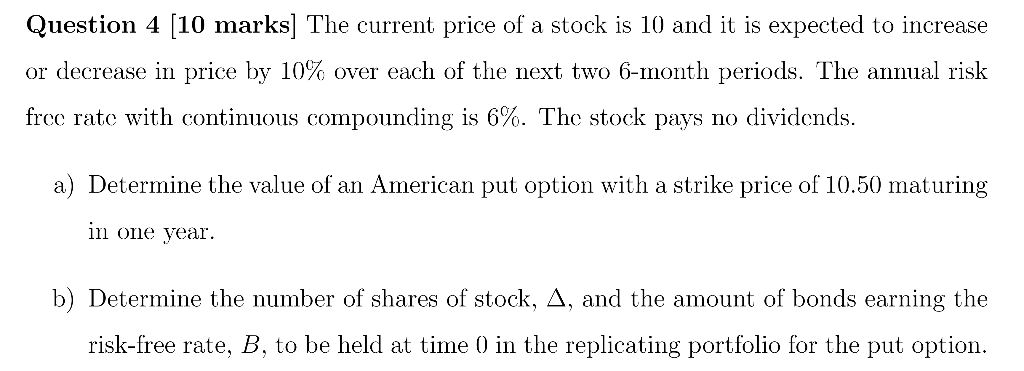

Question

***This is from Investment and Financial Mathematics (IFM) course for Actuaries. Please give handwritten solution with all steps shown. I will give thumbs-up for clear

***This is from Investment and Financial Mathematics (IFM) course for Actuaries. Please give handwritten solution with all steps shown. I will give "thumbs-up" for clear and correct solution. Thanks in advance!***

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Risk Management And Financial Institutions

Authors: John C. Hull

3rd Edition

1118269039, 9781118269039