This is government accounting Please answer some expert in the field NOT FINANCIAL ACCOUNTING PLEASE

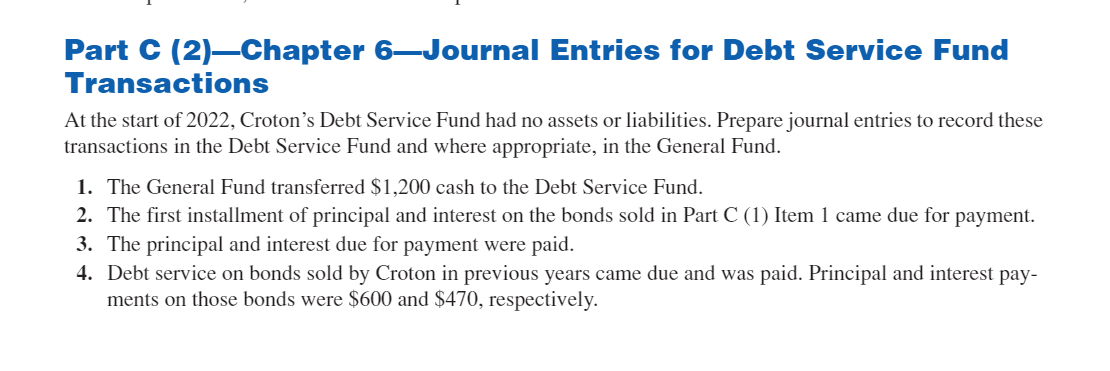

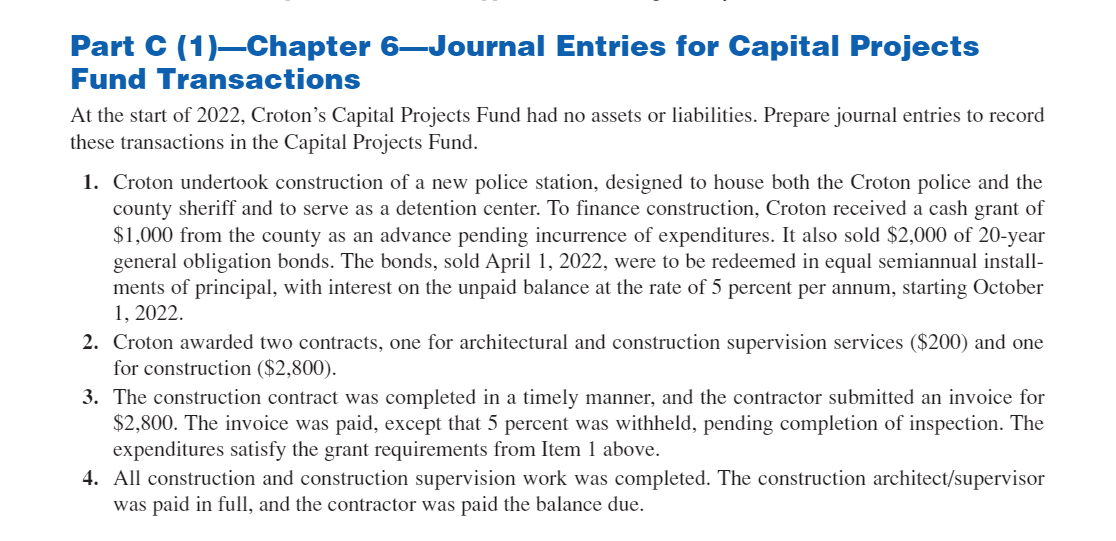

Part C (2)-Chapter 6-Journal Entries for Debt Service Fund Transactions At the start of 2022, Croton's Debt Service Fund had no assets or liabilities. Prepare journal entries to record these transactions in the Debt Service Fund and where appropriate, in the General Fund. 1. The General Fund transferred $1,200 cash to the Debt Service Fund. 2. The first installment of principal and interest on the bonds sold in Part C (1) Item 1 came due for payment. 3. The principal and interest due for payment were paid. 4. Debt service on bonds sold by Croton in previous years came due and was paid. Principal and interest payments on those bonds were $600 and $470, respectively. Part C (1)-Chapter 6-Journal Entries for Capital Projects Fund Transactions At the start of 2022, Croton's Capital Projects Fund had no assets or liabilities. Prepare journal entries to record these transactions in the Capital Projects Fund. 1. Croton undertook construction of a new police station, designed to house both the Croton police and the county sheriff and to serve as a detention center. To finance construction, Croton received a cash grant of $1,000 from the county as an advance pending incurrence of expenditures. It also sold $2,000 of 20-year general obligation bonds. The bonds, sold April 1, 2022, were to be redeemed in equal semiannual installments of principal, with interest on the unpaid balance at the rate of 5 percent per annum, starting October 1, 2022. 2. Croton awarded two contracts, one for architectural and construction supervision services (\$200) and one for construction ($2,800). 3. The construction contract was completed in a timely manner, and the contractor submitted an invoice for $2,800. The invoice was paid, except that 5 percent was withheld, pending completion of inspection. The expenditures satisfy the grant requirements from Item 1 above. 4. All construction and construction supervision work was completed. The construction architect/supervisor was paid in full, and the contractor was paid the balance due. Part C (2)-Chapter 6-Journal Entries for Debt Service Fund Transactions At the start of 2022, Croton's Debt Service Fund had no assets or liabilities. Prepare journal entries to record these transactions in the Debt Service Fund and where appropriate, in the General Fund. 1. The General Fund transferred $1,200 cash to the Debt Service Fund. 2. The first installment of principal and interest on the bonds sold in Part C (1) Item 1 came due for payment. 3. The principal and interest due for payment were paid. 4. Debt service on bonds sold by Croton in previous years came due and was paid. Principal and interest payments on those bonds were $600 and $470, respectively. Part C (1)-Chapter 6-Journal Entries for Capital Projects Fund Transactions At the start of 2022, Croton's Capital Projects Fund had no assets or liabilities. Prepare journal entries to record these transactions in the Capital Projects Fund. 1. Croton undertook construction of a new police station, designed to house both the Croton police and the county sheriff and to serve as a detention center. To finance construction, Croton received a cash grant of $1,000 from the county as an advance pending incurrence of expenditures. It also sold $2,000 of 20-year general obligation bonds. The bonds, sold April 1, 2022, were to be redeemed in equal semiannual installments of principal, with interest on the unpaid balance at the rate of 5 percent per annum, starting October 1, 2022. 2. Croton awarded two contracts, one for architectural and construction supervision services (\$200) and one for construction ($2,800). 3. The construction contract was completed in a timely manner, and the contractor submitted an invoice for $2,800. The invoice was paid, except that 5 percent was withheld, pending completion of inspection. The expenditures satisfy the grant requirements from Item 1 above. 4. All construction and construction supervision work was completed. The construction architect/supervisor was paid in full, and the contractor was paid the balance due