Answered step by step

Verified Expert Solution

Question

1 Approved Answer

this is how the question is. theres nothing more to it thats all i have and want to learn. Question 24.15 The following relates to

this is how the question is. theres nothing more to it thats all i have and want to learn.

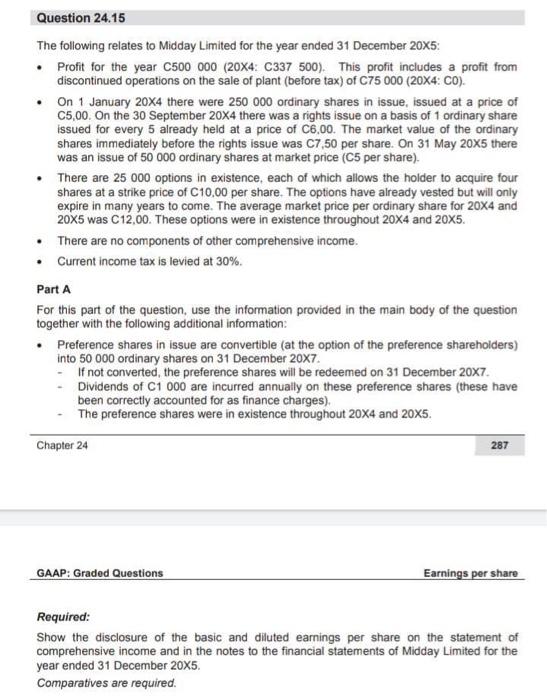

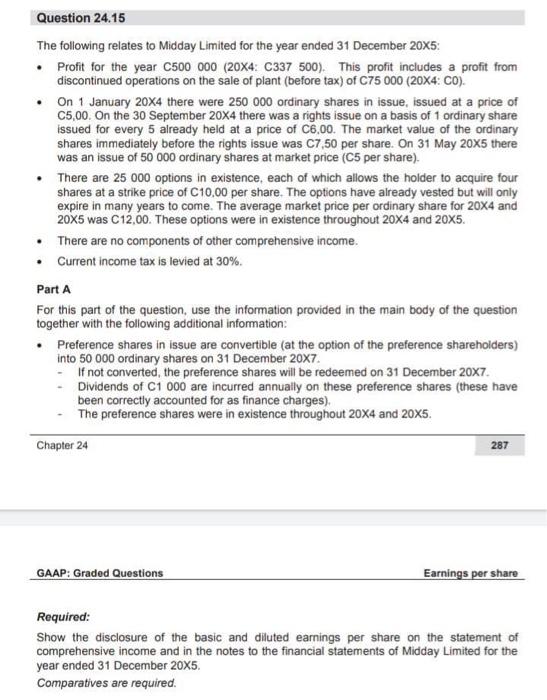

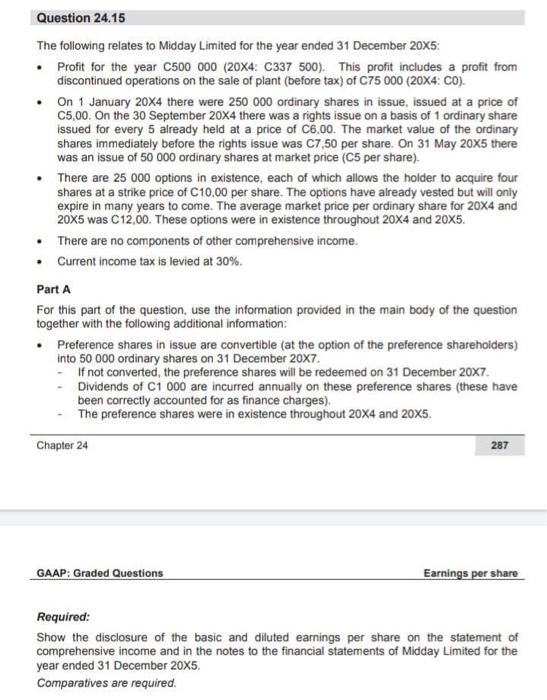

Question 24.15 The following relates to Midday Limited for the year ended 31 December 20X5: Profit for the year C500 000 (20X4: C337 500). This profit includes a profit from discontinued operations on the sale of plant (before tax) of C75 000 (20X4: CO). On 1 January 20X4 there were 250 000 ordinary shares in issue, issued at a price of C5,00. On the 30 September 20X4 there was a rights issue on a basis of 1 ordinary share issued for every 5 already held at a price of C6,00. The market value of the ordinary shares immediately before the rights issue was C7,50 per share. On 31 May 20X5 there was an issue of 50 000 ordinary shares at market price (C5 per share). There are 25 000 options in existence, each of which allows the holder to acquire four shares at a strike price of C10,00 per share. The options have already vested but will only expire in many years to come. The average market price per ordinary share for 20X4 and 20X5 was C12,00. These options were in existence throughout 20X4 and 20X5. There are no components of other comprehensive income. Current income tax is levied at 30%. Part A For this part of the question, use the information provided in the main body of the question together with the following additional information: Preference shares in issue are convertible (at the option of the preference shareholders) into 50 000 ordinary shares on 31 December 20X7. - - If not converted, the preference shares will be redeemed on 31 December 20x7. Dividends of C1 000 are incurred annually on these preference shares (these have been correctly accounted for as finance charges). The preference shares were in existence throughout 20X4 and 20X5. Chapter 24 287 GAAP: Graded Questions Earnings per share Required: Show the disclosure of the basic and diluted earnings per share on the statement of comprehensive income and in the notes to the financial statements of Midday Limited for the year ended 31 December 20X5. Comparatives are required. Question 24.15 The following relates to Midday Limited for the year ended 31 December 20X5: Profit for the year C500 000 (20X4: C337 500). This profit includes a profit from discontinued operations on the sale of plant (before tax) of C75 000 (20X4: CO). On 1 January 20X4 there were 250 000 ordinary shares in issue, issued at a price of C5,00. On the 30 September 20X4 there was a rights issue on a basis of 1 ordinary share issued for every 5 already held at a price of C6,00. The market value of the ordinary shares immediately before the rights issue was C7,50 per share. On 31 May 20X5 there was an issue of 50 000 ordinary shares at market price (C5 per share). There are 25 000 options in existence, each of which allows the holder to acquire four shares at a strike price of C10,00 per share. The options have already vested but will only expire in many years to come. The average market price per ordinary share for 20X4 and 20X5 was C12,00. These options were in existence throughout 20X4 and 20X5. There are no components of other comprehensive income. Current income tax is levied at 30%. Part A For this part of the question, use the information provided in the main body of the question together with the following additional information: Preference shares in issue are convertible (at the option of the preference shareholders) into 50 000 ordinary shares on 31 December 20X7. - - If not converted, the preference shares will be redeemed on 31 December 20x7. Dividends of C1 000 are incurred annually on these preference shares (these have been correctly accounted for as finance charges). The preference shares were in existence throughout 20X4 and 20X5. Chapter 24 287 GAAP: Graded Questions Earnings per share Required: Show the disclosure of the basic and diluted earnings per share on the statement of comprehensive income and in the notes to the financial statements of Midday Limited for the year ended 31 December 20X5. Comparatives are required. Question 24.15 The following relates to Midday Limited for the year ended 31 December 20X5: Profit for the year C500 000 (20X4: C337 500). This profit includes a profit from discontinued operations on the sale of plant (before tax) of C75 000 (20X4: CO). On 1 January 20X4 there were 250 000 ordinary shares in issue, issued at a price of C5,00. On the 30 September 20X4 there was a rights issue on a basis of 1 ordinary share issued for every 5 already held at a price of C6,00. The market value of the ordinary shares immediately before the rights issue was C7,50 per share. On 31 May 20X5 there was an issue of 50 000 ordinary shares at market price (C5 per share). There are 25 000 options in existence, each of which allows the holder to acquire four shares at a strike price of C10,00 per share. The options have already vested but will only expire in many years to come. The average market price per ordinary share for 20X4 and 20X5 was C12,00. These options were in existence throughout 20X4 and 20X5. There are no components of other comprehensive income. Current income tax is levied at 30%. Part A For this part of the question, use the information provided in the main body of the question together with the following additional information: Preference shares in issue are convertible (at the option of the preference shareholders) into 50 000 ordinary shares on 31 December 20X7. - - If not converted, the preference shares will be redeemed on 31 December 20x7. Dividends of C1 000 are incurred annually on these preference shares (these have been correctly accounted for as finance charges). The preference shares were in existence throughout 20X4 and 20X5. Chapter 24 287 GAAP: Graded Questions Earnings per share Required: Show the disclosure of the basic and diluted earnings per share on the statement of comprehensive income and in the notes to the financial statements of Midday Limited for the year ended 31 December 20X5. Comparatives are required Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Environmental Audits

Authors: Cliff VanGuilder

1st Edition

1938549600, 978-1938549601