Answered step by step

Verified Expert Solution

Question

1 Approved Answer

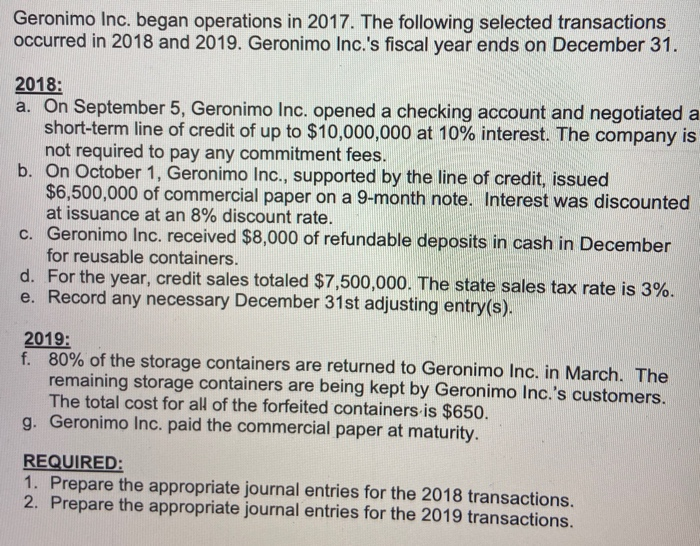

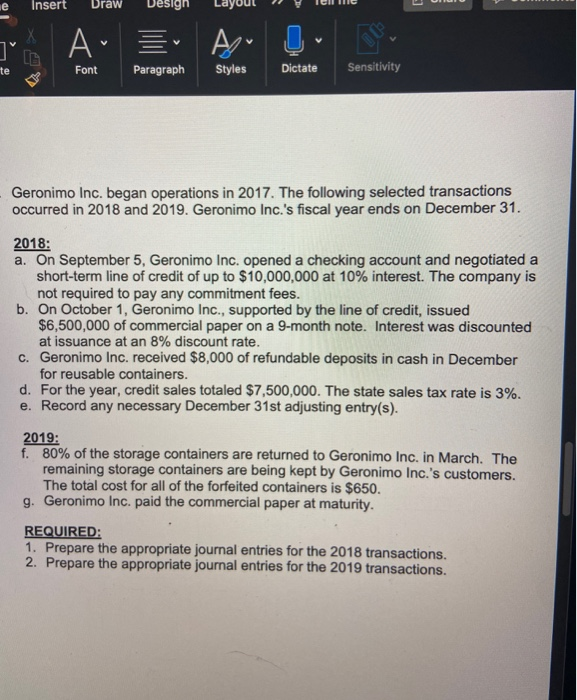

this is the only information i was given Geronimo Inc. began operations in 2017. The following selected transactions occurred in 2018 and 2019. Geronimo Inc.'s

this is the only information i was given

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Control And Audit In Management Accounting Cima Stage 4

Authors: Jeff Coates, Colin Rickwood, Ray Stacey

1st Edition

0750609958, 978-0750609951