Answered step by step

Verified Expert Solution

Question

1 Approved Answer

This is the question there's no additional info to provide you, please read it carefully 1st,2nd pictures explain the question and 3rd pic required for

This is the question there's no additional info to provide you, please read it carefully

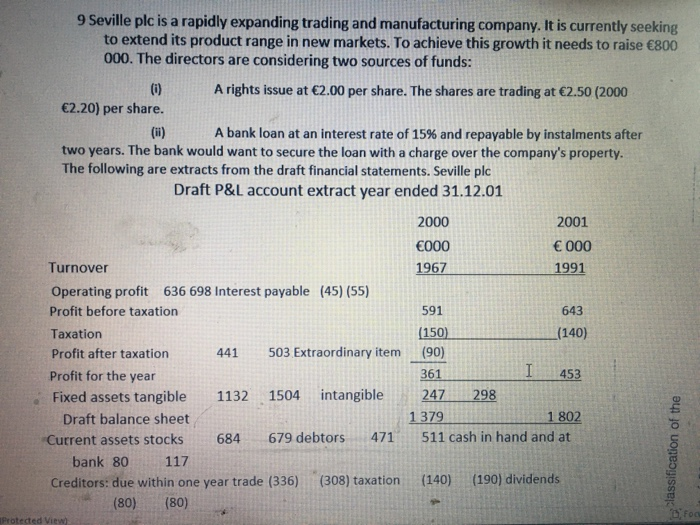

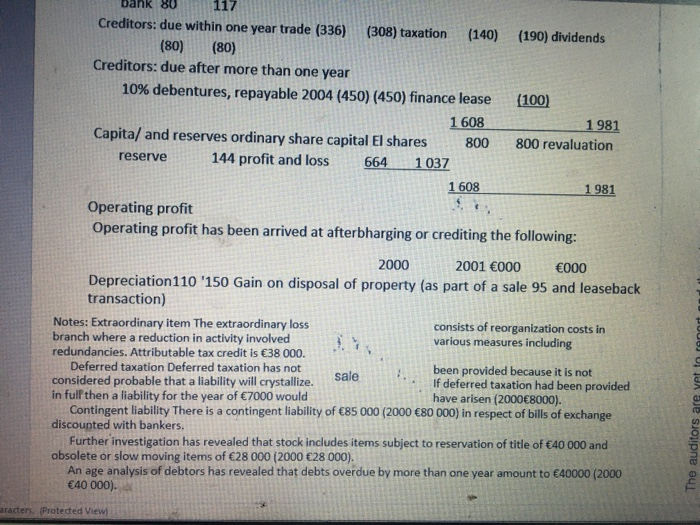

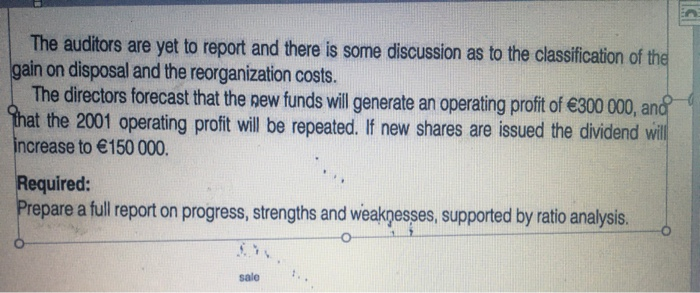

9 Seville plc is a rapidly expanding trading and manufacturing company. It is currently seeking to extend its product range in new markets. To achieve this growth it needs to raise 800 000. The directors are considering two sources of funds: (i) A rights issue at 2.00 per share. The shares are trading at 2.50 (2000 2.20) per share. (ii) A bank loan at an interest rate of 15% and repayable by instalments after two years. The bank would want to secure the loan with a charge over the company's property. The following are extracts from the draft financial statements. Seville plc Draft P&L account extract year ended 31.12.01 2000 000 1967 2001 000 1991 Turnover Operating profit 636 698 Interest payable (45) (55) Profit before taxation Taxation Profit after taxation 441 503 Extraordinary item Profit for the year Fixed assets tangible 1132 1504 intangible Draft balance sheet Current assets stocks 684 679 debtors 471 bank 80 117 Creditors: due within one year trade (336) (308) taxation (80) (80) Protected View 591 643 (150) (140) (90) 361 453 247 298 1 379 1 802 511 cash in hand and at I classification of the (140) (190) dividends Drog ank 80 (190) dividends 117 Creditors: due within one year trade (336) (308) taxation (140) (80) (80) Creditors: due after more than one year 10% debentures, repayable 2004 (450) (450) finance lease 1 608 Capita/ and reserves ordinary share capital El shares 800 reserve 144 profit and loss 664 1037 1 608 (100) 1981 800 revaluation 1981 Operating profit Operating profit has been arrived at afterbharging or crediting the following: 2000 2001 000 000 Depreciation 110 '150 Gain on disposal of property (as part of a sale 95 and leaseback transaction) Notes: Extraordinary item The extraordinary loss consists of reorganization costs in branch where a reduction in activity involved various measures including redundancies. Attributable tax credit is 38 000. Deferred taxation Deferred taxation has not been provided because it is not sale considered probable that a liability will crystallize. If deferred taxation had been provided in full then a liability for the year of 7000 would have arisen (20008000). Contingent liability There is a contingent liability of 85 000 (2000 80 000) in respect of bills of exchange discounted with bankers. Further investigation has revealed that stock includes items subject to reservation of title of 40 000 and obsolete or slow moving items of 28 000 (2000 28 000). An age analysis of debtors has revealed that debts overdue by more than one year amount to 40000 (2000 40 000). The auditors are yet to renart aracters. (Protected View CH The auditors are yet to report and there is some discussion as to the classification of the gain on disposal and the reorganization costs. The directors forecast that the new funds will generate an operating profit of 300 000, and That the 2001 operating profit will be repeated. If new shares are issued the dividend will increase to 150 000. Required: Prepare a full report on progress, strengths and weakesses, supported by ratio analysis. sale 9 Seville plc is a rapidly expanding trading and manufacturing company. It is currently seeking to extend its product range in new markets. To achieve this growth it needs to raise 800 000. The directors are considering two sources of funds: (i) A rights issue at 2.00 per share. The shares are trading at 2.50 (2000 2.20) per share. (ii) A bank loan at an interest rate of 15% and repayable by instalments after two years. The bank would want to secure the loan with a charge over the company's property. The following are extracts from the draft financial statements. Seville plc Draft P&L account extract year ended 31.12.01 2000 000 1967 2001 000 1991 Turnover Operating profit 636 698 Interest payable (45) (55) Profit before taxation Taxation Profit after taxation 441 503 Extraordinary item Profit for the year Fixed assets tangible 1132 1504 intangible Draft balance sheet Current assets stocks 684 679 debtors 471 bank 80 117 Creditors: due within one year trade (336) (308) taxation (80) (80) Protected View 591 643 (150) (140) (90) 361 453 247 298 1 379 1 802 511 cash in hand and at I classification of the (140) (190) dividends Drog ank 80 (190) dividends 117 Creditors: due within one year trade (336) (308) taxation (140) (80) (80) Creditors: due after more than one year 10% debentures, repayable 2004 (450) (450) finance lease 1 608 Capita/ and reserves ordinary share capital El shares 800 reserve 144 profit and loss 664 1037 1 608 (100) 1981 800 revaluation 1981 Operating profit Operating profit has been arrived at afterbharging or crediting the following: 2000 2001 000 000 Depreciation 110 '150 Gain on disposal of property (as part of a sale 95 and leaseback transaction) Notes: Extraordinary item The extraordinary loss consists of reorganization costs in branch where a reduction in activity involved various measures including redundancies. Attributable tax credit is 38 000. Deferred taxation Deferred taxation has not been provided because it is not sale considered probable that a liability will crystallize. If deferred taxation had been provided in full then a liability for the year of 7000 would have arisen (20008000). Contingent liability There is a contingent liability of 85 000 (2000 80 000) in respect of bills of exchange discounted with bankers. Further investigation has revealed that stock includes items subject to reservation of title of 40 000 and obsolete or slow moving items of 28 000 (2000 28 000). An age analysis of debtors has revealed that debts overdue by more than one year amount to 40000 (2000 40 000). The auditors are yet to renart aracters. (Protected View CH The auditors are yet to report and there is some discussion as to the classification of the gain on disposal and the reorganization costs. The directors forecast that the new funds will generate an operating profit of 300 000, and That the 2001 operating profit will be repeated. If new shares are issued the dividend will increase to 150 000. Required: Prepare a full report on progress, strengths and weakesses, supported by ratio analysis. sale 1st,2nd pictures explain the question and 3rd pic required for it

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance And Investments Application To South African Financial Markets

Authors: Mthuli Ncube

1st Edition

3843375984, 9783843375986