Answered step by step

Verified Expert Solution

Question

1 Approved Answer

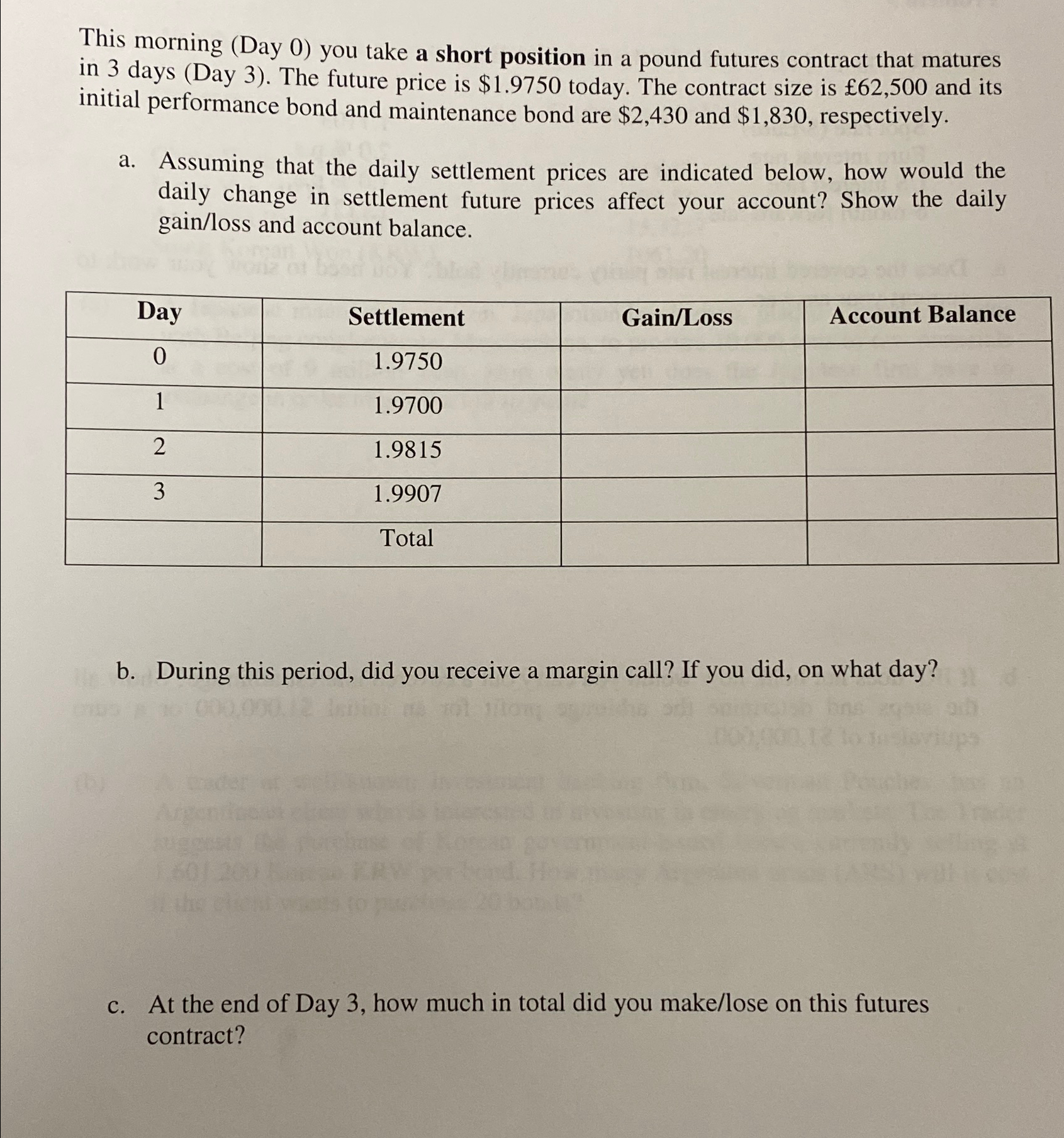

This morning ( Day 0 ) you take a short position in a pound futures contract that matures in 3 days ( Day 3 )

This morning Day you take a short position in a pound futures contract that matures in days Day The future price is $ today. The contract size is and its initial performance bond and maintenance bond are $ and $ respectively.

a Assuming that the daily settlement prices are indicated below, how would the daily change in settlement future prices affect your account? Show the daily gainloss and account balance.

tableDaySettlement,GainLossAccount BalanceTotal,,

b During this period, did you receive a margin call? If you did, on what day?

c At the end of Day how much in total did you makelose on this futures contract?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

The Pillars Of Finance The Misalignment Of Finance Theory And Investment Practice

Authors: G. Fraser-Sampson

2014th Edition

1137264055, 978-1137264053