Answered step by step

Verified Expert Solution

Question

1 Approved Answer

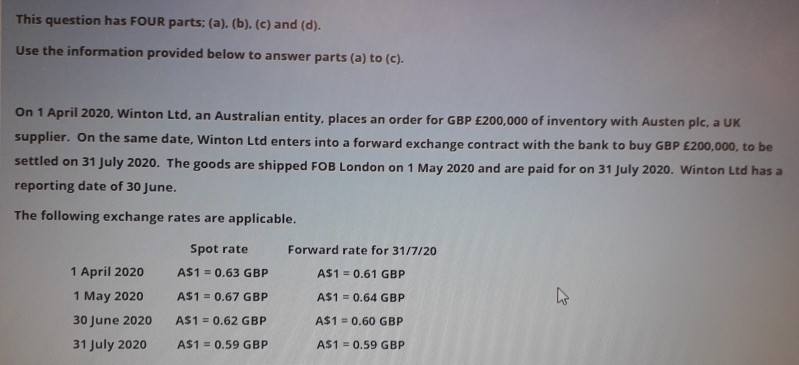

This question has FOUR parts: (a), (b). (c) and (d). Use the information provided below to answer parts (a) to (c). On 1 April 2020,

This question has FOUR parts: (a), (b). (c) and (d). Use the information provided below to answer parts (a) to (c). On 1 April 2020, Winton Ltd, an Australian entity, places an order for GBP 200,000 of inventory with Austen plc, a UK supplier. On the same date, Winton Ltd enters into a forward exchange contract with the bank to buy GBP 200,000, to be settled on 31 July 2020. The goods are shipped FOB London on 1 May 2020 and are paid for on 31 July 2020. Winton Ltd has a reporting date of 30 June. The following exchange rates are applicable. Spot rate Forward rate for 31/7/20 A$1 = 0.63 GBP A$1 = 0.61 GBP A$1 = 0.67 GBP A$1 = 0.64 GBP 1 April 2020 1 May 2020 30 June 2020 31 July 2020 AS1 = 0.62 GBP A$1 = 0.60 GBP A$1 = 0.59 GBP A$1 = 0.59 GBP Question 4(a) (4 marks) Required: Complete the table below showing the movement and the change in value of the hedged item. Question 4(b) (6 marks) Required: Complete the table showing the movement and the change in value of the hedging instrument. Question 4(c) (10 marks) Required: Prepare the journal entries for Winton Led to reflect the above transactions

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Auditing Investments

Authors: Barbara Davison

1st Edition

0894134272, 978-0894134272