Answered step by step

Verified Expert Solution

Question

1 Approved Answer

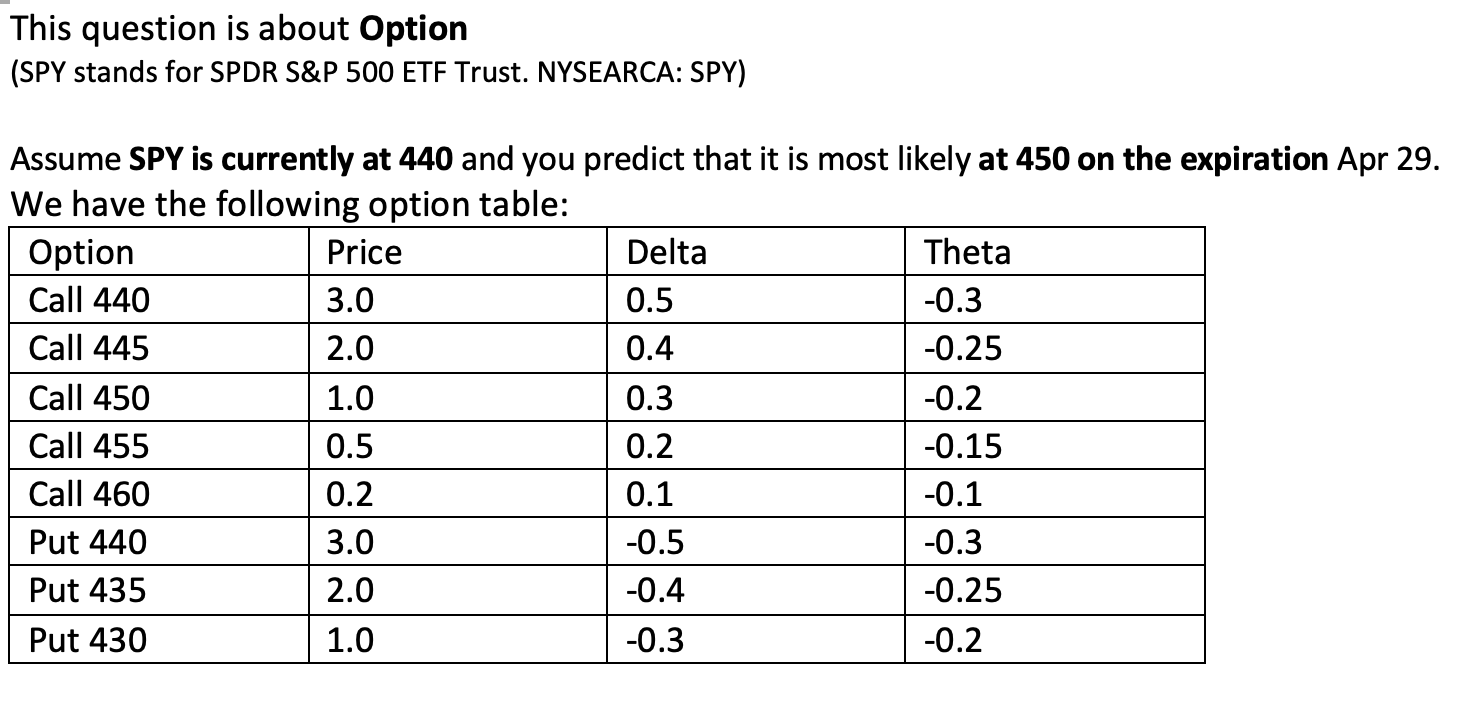

This question is about Option (SPY stands for SPDR S&P 500 ETF Trust. NYSEARCA: SPY) Assume SPY is currently at 440 and you predict that

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Financial Management

Authors: Eugene F Brigham, Phillip R Daves

9th Edition

032431986X, 9780324319866