those answers are right how DID they get them?

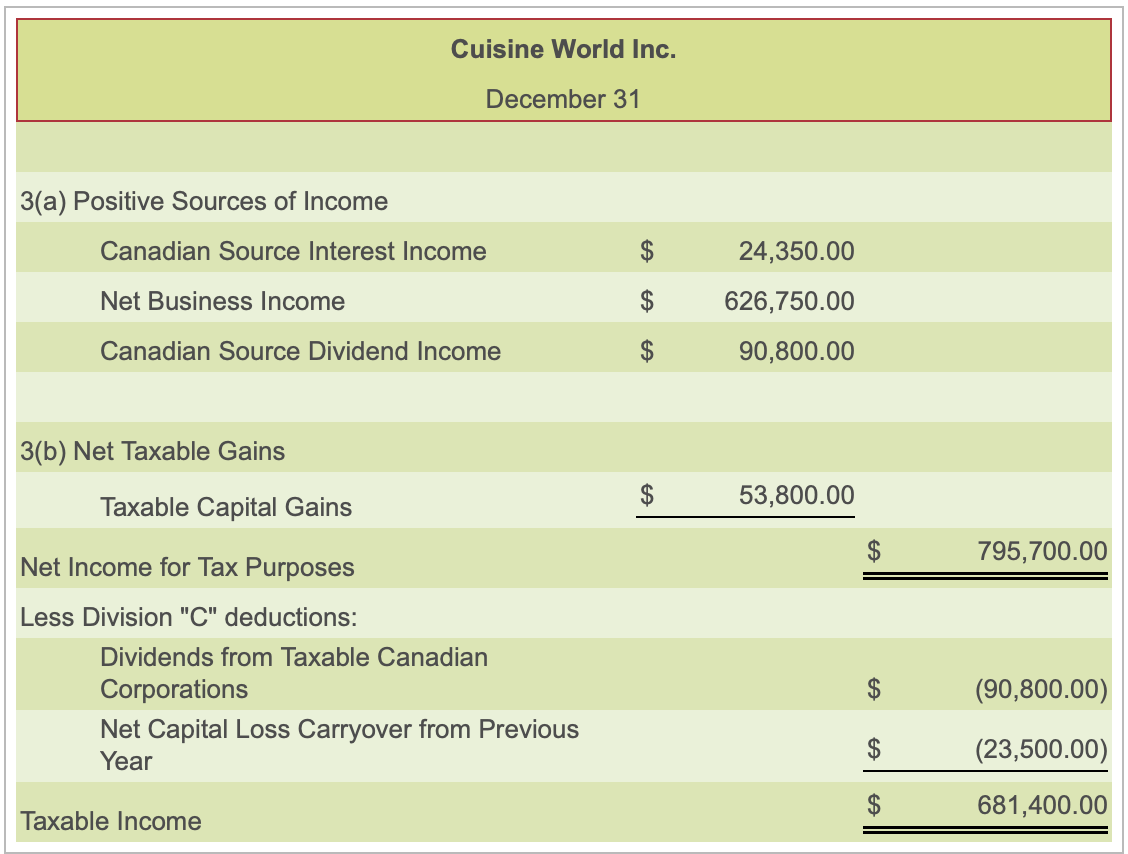

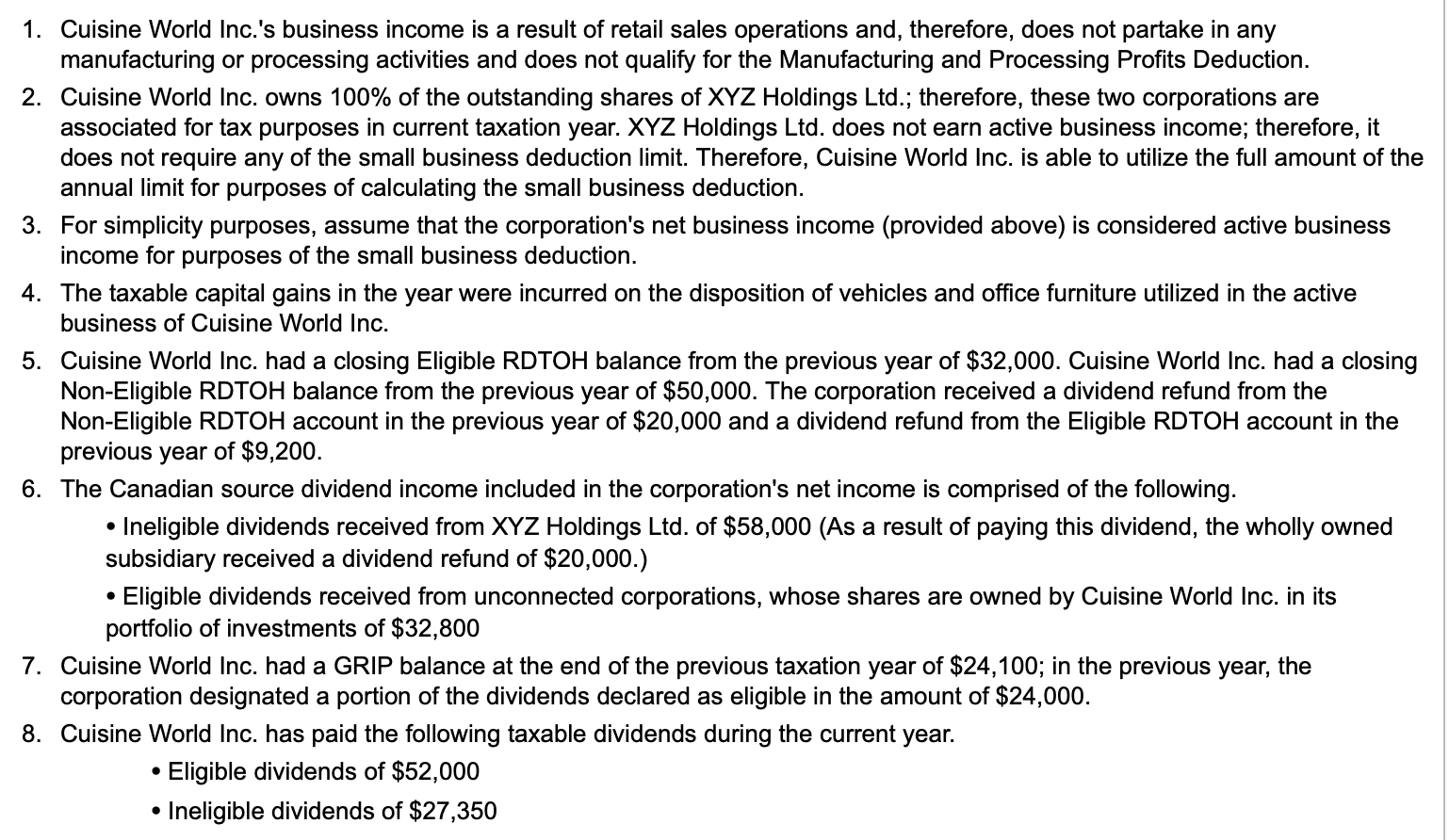

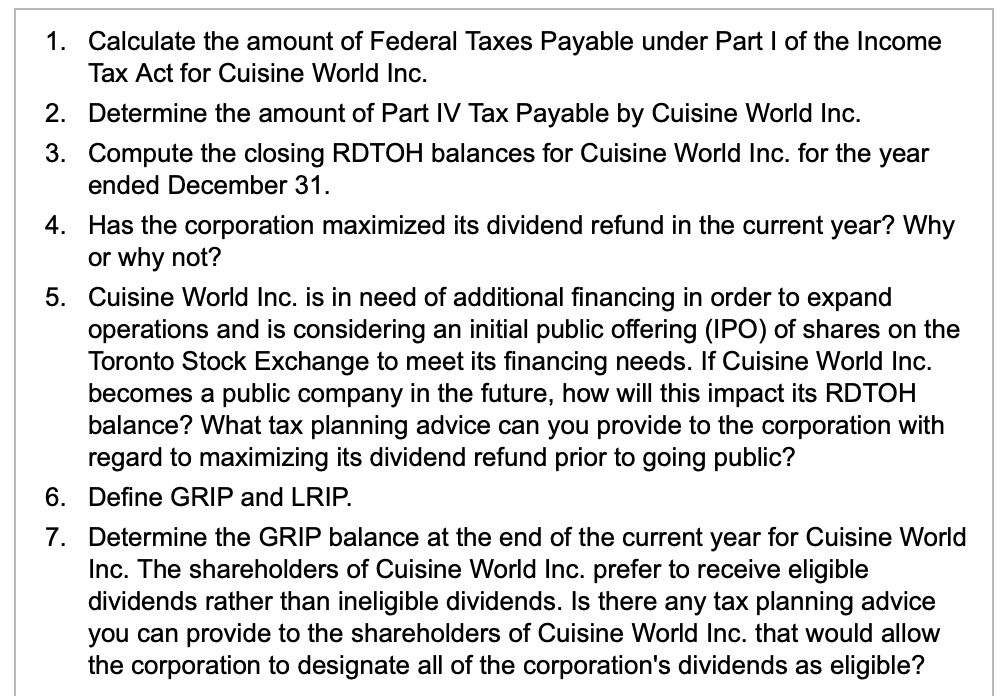

X Question 13.1.7 Question Help Cuisine World Inc. is a Canadian controlled private corporation (CCPC) that operates a retail business selling cooking utensils, knives, and small appliances for both professional chefs and home cooks. Cuisine World Inc. is operated out of Laval, Quebec, and all of the corporation's revenue and expenses are incurred in Quebec. (Click on the icon to view the financial information.) A (Click on the icon to view the additional information.) Required Requirement 1. Calculate the amount of Federal Taxes Payable under Part I of the Income Tax Act for Cuisine World Inc. (Round to the nearest cent.) The amount of Federal Taxes Payable under Part I of the Income Tax Act for Cuisine World Inc. is $ Cuisine World Inc. December 31 3(a) Positive Sources of Income Canadian Source Interest Income $ 24,350.00 Net Business Income $ 626,750.00 Canadian Source Dividend Income $ 90,800.00 3(b) Net Taxable Gains $ Taxable Capital Gains 53,800.00 $ 795,700.00 Net Income for Tax Purposes Less Division "C" deductions: Dividends from Taxable Canadian Corporations Net Capital Loss Carryover from Previous Year $ (90,800.00) $ (23,500.00) $ 681,400.00 Taxable Income 1. Cuisine World Inc.'s business income is a result of retail sales operations and, therefore, does not partake in any manufacturing or processing activities and does not qualify for the Manufacturing and Processing Profits Deduction. 2. Cuisine World Inc. owns 100% of the outstanding shares of XYZ Holdings Ltd.; therefore, these two corporations are associated for tax purposes in current taxation year. XYZ Holdings Ltd. does not earn active business income; therefore, it does not require any of the small business deduction limit. Therefore, Cuisine World Inc. is able to utilize the full amount of the annual limit for purposes of calculating the small business deduction. 3. For simplicity purposes, assume that the corporation's net business income (provided above) is considered active business income for purposes of the small business deduction. 4. The taxable capital gains in the year were incurred on the disposition of vehicles and office furniture utilized in the active business of Cuisine World Inc. 5. Cuisine World Inc. had a closing Eligible RDTOH balance from the previous year of $32,000. Cuisine World Inc. had a closing Non-Eligible RDTOH balance from the previous year of $50,000. The corporation received a dividend refund from the Non-Eligible RDTOH account in the previous year of $20,000 and a dividend refund from the Eligible RDTOH account in the previous year of $9,200. 6. The Canadian source dividend income included in the corporation's net income is comprised of the following. Ineligible dividends received from XYZ Holdings Ltd. of $58,000 (As a result of paying this dividend, the wholly owned subsidiary received a dividend refund of $20,000.) Eligible dividends received from unconnected corporations, whose shares are owned by Cuisine World Inc. in its portfolio of investments of $32,800 7. Cuisine World Inc. had a GRIP balance at the end of the previous taxation year of $24,100; in the previous year, the corporation designated a portion of the dividends declared as eligible in the amount of $24,000. 8. Cuisine World Inc. has paid the following taxable dividends during the current year. Eligible dividends of $52,000 Ineligible dividends of $27,350 1. Calculate the amount of Federal Taxes Payable under Part I of the Income Tax Act for Cuisine World Inc. 2. Determine the amount of Part IV Tax Payable by Cuisine World Inc. 3. Compute the closing RDTOH balances for Cuisine World Inc. for the year ended December 31. 4. Has the corporation maximized its dividend refund in the current year? Why or why not? 5. Cuisine World Inc. is in need of additional financing in order to expand operations and is considering an initial public offering (IPO) of shares on the Toronto Stock Exchange to meet its financing needs. If Cuisine World Inc. becomes a public company in the future, how will this impact its RDTOH balance? What tax planning advice can you provide to the corporation with regard to maximizing its dividend refund prior to going public? 6. Define GRIP and LRIP. 7. Determine the GRIP balance at the end of the current year for Cuisine World Inc. The shareholders of Cuisine World Inc. prefer to receive eligible dividends rather than ineligible dividends. Is there any tax planning advice you can provide to the shareholders of Cuisine World Inc. that would allow the corporation to designate all of the corporation's dividends as eligible? Requirement 1. Calculate the amount of Federal Taxes Payable under Part 1 of the Income Tax Act for Cuisine World Inc. (Round to the nearest cent.) The amount of Federal Taxes Payable under Part of the Income Tax Act for Cuisine World Inc. is $ 87,288.83 Requirement 2. Determine the amount of Part IV Tax Payable by Cuisine World Inc. (Round to the nearest cent.) The amount of Part IV Tax Payable by Cuisine World Inc. is $ 32,573.00 Requirement 3. Compute the closing RDTOH balances for Cuisine World Inc. for the year ended December 31, (Round amounts to the nearest cent.) The closing eligible RDTOH balance for Cuisine World Inc. is $ 35,373.33. The closing non-eligible RDTOH balance for Cuisine World Inc. is $ 66,759.33 Requirement 4. Has the corporation maximized its dividend refund in the current year? Why or why not? The company has not maximized its dividend refund. In order to ensure that the corporation receives the maximum dividend refund, it should declare dividends equal to 2.608 times the closing RDTOH balances. Requirement 5. Cuisine World Inc. is in need of additional financing in order to expand operations and is considering an initial public offering (IPO) of shares on the Toronto Stock Exchange to meet its financing needs. If Cuisine World Inc. becomes a public company in the future, how will this impact its RDTOH balance? What tax planning advice can you provide to the corporation with regard to maximizing its dividend refund prior to going public? If Cuisine World Inc. becomes a public company in the future, how will this impact their RDTOH balance? XA. Cuisine would be able to keep its RDTOH balance as RDTOH and dividend refunds are for private and public corporationis OB. Cuisine would only keep 50% of its RDTOH balance as RDTOH and dividend refunds are reduced when a private corporation becomes public c. Cuisine would lose its RDTOH balance as RDTOH and dividend refunds are only for private corporations. OD. The RDTOH balance for Cuisine is reset to $0 as RDTOH and dividend refunds are not rolled over when a private corporation becomes public. What tax planning advice can you provide to the corporation with regard to maximizing its dividend refund prior to going public? What tax planning advice can you provide to the corporation with regard to maximizing its dividend refund prior to going public? Determine the correct statement pertaining to the tax advice for a CCPC considering going public. Choose the correct answer below. A. Distribute adequate dividends to maximize the dividend refund. B. To maximize the dividend refund, do not distribute any dividends. C. Issue a 2-for-1 share split immediately before going public to maximize the dividend refund. D. Declare dividends before going public, but do not pay them until after going public Requirement 6. Define GRIP and LRIP. Define GRIP In general, this account tracks the portion of a CCPC's income that has been taxed at general or high corporate tax rates. Define LRIP. In general, this account tracks the portion of a non-CCPC's income that has been taxed at low or preferential corporate tax rates. Requirement 7. Determine the GRIP balance at the end of the current year for Cuisine World Inc. The shareholders of Cuisine World Inc. prefer to receive eligible dividends rather than ineligible dividends. Is there any tax planning advice you can provide to the shareholders of Cuisine World Inc. that would allow the corporation to designate all of the corporation's dividends as eligible? (Round to the nearest whole dollar.) The GRIP balance at the end of the current year for Cuisine World Inc. is $149,900. The shareholders of Cuisine World Inc. prefer to receive eligible dividends rather than ineligible dividends. Is there any tax planning advice you can provide to the shareholders of Cuisine World Inc. that would allow the corporation to designate all of the corporation's dividends as eligible? Cuisine World Inc. should file an ITA 89(11) election which will deem the corporation to be a CCPC X Question 13.1.7 Question Help Cuisine World Inc. is a Canadian controlled private corporation (CCPC) that operates a retail business selling cooking utensils, knives, and small appliances for both professional chefs and home cooks. Cuisine World Inc. is operated out of Laval, Quebec, and all of the corporation's revenue and expenses are incurred in Quebec. (Click on the icon to view the financial information.) A (Click on the icon to view the additional information.) Required Requirement 1. Calculate the amount of Federal Taxes Payable under Part I of the Income Tax Act for Cuisine World Inc. (Round to the nearest cent.) The amount of Federal Taxes Payable under Part I of the Income Tax Act for Cuisine World Inc. is $ Cuisine World Inc. December 31 3(a) Positive Sources of Income Canadian Source Interest Income $ 24,350.00 Net Business Income $ 626,750.00 Canadian Source Dividend Income $ 90,800.00 3(b) Net Taxable Gains $ Taxable Capital Gains 53,800.00 $ 795,700.00 Net Income for Tax Purposes Less Division "C" deductions: Dividends from Taxable Canadian Corporations Net Capital Loss Carryover from Previous Year $ (90,800.00) $ (23,500.00) $ 681,400.00 Taxable Income 1. Cuisine World Inc.'s business income is a result of retail sales operations and, therefore, does not partake in any manufacturing or processing activities and does not qualify for the Manufacturing and Processing Profits Deduction. 2. Cuisine World Inc. owns 100% of the outstanding shares of XYZ Holdings Ltd.; therefore, these two corporations are associated for tax purposes in current taxation year. XYZ Holdings Ltd. does not earn active business income; therefore, it does not require any of the small business deduction limit. Therefore, Cuisine World Inc. is able to utilize the full amount of the annual limit for purposes of calculating the small business deduction. 3. For simplicity purposes, assume that the corporation's net business income (provided above) is considered active business income for purposes of the small business deduction. 4. The taxable capital gains in the year were incurred on the disposition of vehicles and office furniture utilized in the active business of Cuisine World Inc. 5. Cuisine World Inc. had a closing Eligible RDTOH balance from the previous year of $32,000. Cuisine World Inc. had a closing Non-Eligible RDTOH balance from the previous year of $50,000. The corporation received a dividend refund from the Non-Eligible RDTOH account in the previous year of $20,000 and a dividend refund from the Eligible RDTOH account in the previous year of $9,200. 6. The Canadian source dividend income included in the corporation's net income is comprised of the following. Ineligible dividends received from XYZ Holdings Ltd. of $58,000 (As a result of paying this dividend, the wholly owned subsidiary received a dividend refund of $20,000.) Eligible dividends received from unconnected corporations, whose shares are owned by Cuisine World Inc. in its portfolio of investments of $32,800 7. Cuisine World Inc. had a GRIP balance at the end of the previous taxation year of $24,100; in the previous year, the corporation designated a portion of the dividends declared as eligible in the amount of $24,000. 8. Cuisine World Inc. has paid the following taxable dividends during the current year. Eligible dividends of $52,000 Ineligible dividends of $27,350 1. Calculate the amount of Federal Taxes Payable under Part I of the Income Tax Act for Cuisine World Inc. 2. Determine the amount of Part IV Tax Payable by Cuisine World Inc. 3. Compute the closing RDTOH balances for Cuisine World Inc. for the year ended December 31. 4. Has the corporation maximized its dividend refund in the current year? Why or why not? 5. Cuisine World Inc. is in need of additional financing in order to expand operations and is considering an initial public offering (IPO) of shares on the Toronto Stock Exchange to meet its financing needs. If Cuisine World Inc. becomes a public company in the future, how will this impact its RDTOH balance? What tax planning advice can you provide to the corporation with regard to maximizing its dividend refund prior to going public? 6. Define GRIP and LRIP. 7. Determine the GRIP balance at the end of the current year for Cuisine World Inc. The shareholders of Cuisine World Inc. prefer to receive eligible dividends rather than ineligible dividends. Is there any tax planning advice you can provide to the shareholders of Cuisine World Inc. that would allow the corporation to designate all of the corporation's dividends as eligible? Requirement 1. Calculate the amount of Federal Taxes Payable under Part 1 of the Income Tax Act for Cuisine World Inc. (Round to the nearest cent.) The amount of Federal Taxes Payable under Part of the Income Tax Act for Cuisine World Inc. is $ 87,288.83 Requirement 2. Determine the amount of Part IV Tax Payable by Cuisine World Inc. (Round to the nearest cent.) The amount of Part IV Tax Payable by Cuisine World Inc. is $ 32,573.00 Requirement 3. Compute the closing RDTOH balances for Cuisine World Inc. for the year ended December 31, (Round amounts to the nearest cent.) The closing eligible RDTOH balance for Cuisine World Inc. is $ 35,373.33. The closing non-eligible RDTOH balance for Cuisine World Inc. is $ 66,759.33 Requirement 4. Has the corporation maximized its dividend refund in the current year? Why or why not? The company has not maximized its dividend refund. In order to ensure that the corporation receives the maximum dividend refund, it should declare dividends equal to 2.608 times the closing RDTOH balances. Requirement 5. Cuisine World Inc. is in need of additional financing in order to expand operations and is considering an initial public offering (IPO) of shares on the Toronto Stock Exchange to meet its financing needs. If Cuisine World Inc. becomes a public company in the future, how will this impact its RDTOH balance? What tax planning advice can you provide to the corporation with regard to maximizing its dividend refund prior to going public? If Cuisine World Inc. becomes a public company in the future, how will this impact their RDTOH balance? XA. Cuisine would be able to keep its RDTOH balance as RDTOH and dividend refunds are for private and public corporationis OB. Cuisine would only keep 50% of its RDTOH balance as RDTOH and dividend refunds are reduced when a private corporation becomes public c. Cuisine would lose its RDTOH balance as RDTOH and dividend refunds are only for private corporations. OD. The RDTOH balance for Cuisine is reset to $0 as RDTOH and dividend refunds are not rolled over when a private corporation becomes public. What tax planning advice can you provide to the corporation with regard to maximizing its dividend refund prior to going public? What tax planning advice can you provide to the corporation with regard to maximizing its dividend refund prior to going public? Determine the correct statement pertaining to the tax advice for a CCPC considering going public. Choose the correct answer below. A. Distribute adequate dividends to maximize the dividend refund. B. To maximize the dividend refund, do not distribute any dividends. C. Issue a 2-for-1 share split immediately before going public to maximize the dividend refund. D. Declare dividends before going public, but do not pay them until after going public Requirement 6. Define GRIP and LRIP. Define GRIP In general, this account tracks the portion of a CCPC's income that has been taxed at general or high corporate tax rates. Define LRIP. In general, this account tracks the portion of a non-CCPC's income that has been taxed at low or preferential corporate tax rates. Requirement 7. Determine the GRIP balance at the end of the current year for Cuisine World Inc. The shareholders of Cuisine World Inc. prefer to receive eligible dividends rather than ineligible dividends. Is there any tax planning advice you can provide to the shareholders of Cuisine World Inc. that would allow the corporation to designate all of the corporation's dividends as eligible? (Round to the nearest whole dollar.) The GRIP balance at the end of the current year for Cuisine World Inc. is $149,900. The shareholders of Cuisine World Inc. prefer to receive eligible dividends rather than ineligible dividends. Is there any tax planning advice you can provide to the shareholders of Cuisine World Inc. that would allow the corporation to designate all of the corporation's dividends as eligible? Cuisine World Inc. should file an ITA 89(11) election which will deem the corporation to be a CCPC