Question

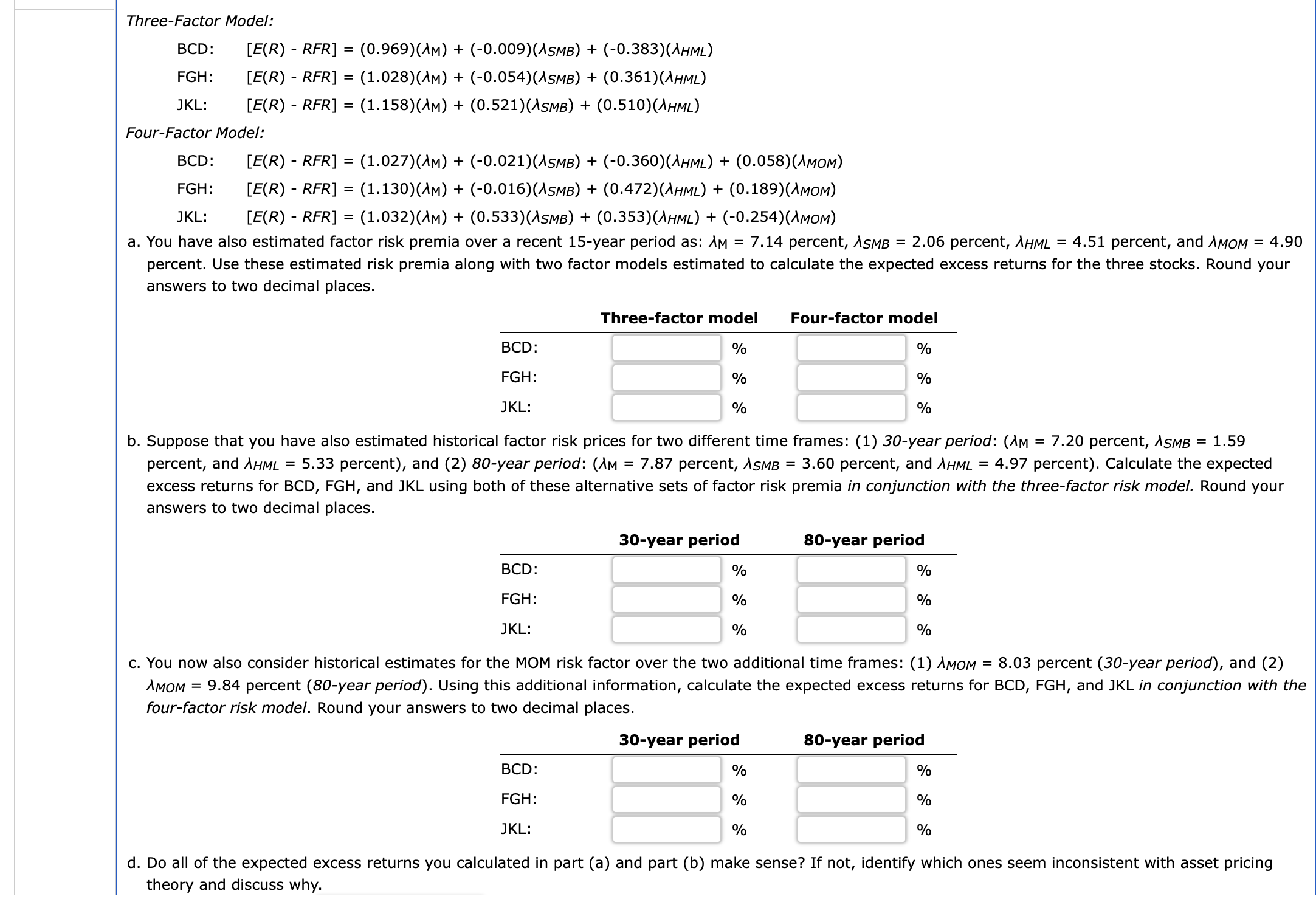

Three-Factor Model: BCD:,[E(R)-RFR]=(0.969)(lambda _(M))+(-0.009)(lambda _(SMB))+(-0.383)(lambda _(HML)) FGH:,[E(R)-RFR]=(1.028)(lambda _(M))+(-0.054)(lambda _(SMB))+(0.361)(lambda _(HML)) JKL:,[E(R)-RFR]=(1.158)(lambda _(M))+(0.521)(lambda _(SMB))+(0.510)(lambda _(HML)) Four-Factor Model: BCD:,[E(R)-RFR]=(1.027)(lambda _(M))+(-0.021)(lambda _(SMB))+(-0.360)(lambda _(HML))+(0.058)(lambda _(MOM)) FGH:,[E(R)-RFR]=(1.130)(lambda _(M))+(-0.016)(lambda _(SMB))+(0.472)(lambda

Three-Factor Model:\

BCD:,[E(R)-RFR]=(0.969)(\\\\lambda _(M))+(-0.009)(\\\\lambda _(SMB))+(-0.383)(\\\\lambda _(HML))\ FGH:,[E(R)-RFR]=(1.028)(\\\\lambda _(M))+(-0.054)(\\\\lambda _(SMB))+(0.361)(\\\\lambda _(HML))\ JKL:,[E(R)-RFR]=(1.158)(\\\\lambda _(M))+(0.521)(\\\\lambda _(SMB))+(0.510)(\\\\lambda _(HML))\ Four-Factor Model:\

BCD:,[E(R)-RFR]=(1.027)(\\\\lambda _(M))+(-0.021)(\\\\lambda _(SMB))+(-0.360)(\\\\lambda _(HML))+(0.058)(\\\\lambda _(MOM))\ FGH:,[E(R)-RFR]=(1.130)(\\\\lambda _(M))+(-0.016)(\\\\lambda _(SMB))+(0.472)(\\\\lambda _(HML))+(0.189)(\\\\lambda _(MOM))\ JKL:,[E(R)-RFR]=(1.032)(\\\\lambda _(M))+(0.533)(\\\\lambda _(SMB))+(0.353)(\\\\lambda _(HML))+(-0.254)(\\\\lambda _(MOM))\ a. You have also estimated factor risk premia over a recent 15-year period as:

\\\\lambda _(M)=7.14percent,

\\\\lambda _(SMB)=2.06percent,

\\\\lambda _(HML)=4.51percent, and

\\\\lambda _(MOM)=4.90\ percent. Use these estimated risk premia along with two factor models estimated to calculate the expected excess returns for the three stocks. Round your\ answers to two decimal places.\ b. Suppose that you have also estimated historical factor risk prices for two different time frames: (1) 30-year period: percent,

\\\\lambda _(SMB )=1.59\ percent, and

\\\\lambda _(HML)=5.33percent

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

M Finance

Authors: Marcia Cornett, Troy Adair, John Nofsinger

3rd Edition

0077861779, 978-0077861773