Answered step by step

Verified Expert Solution

Question

1 Approved Answer

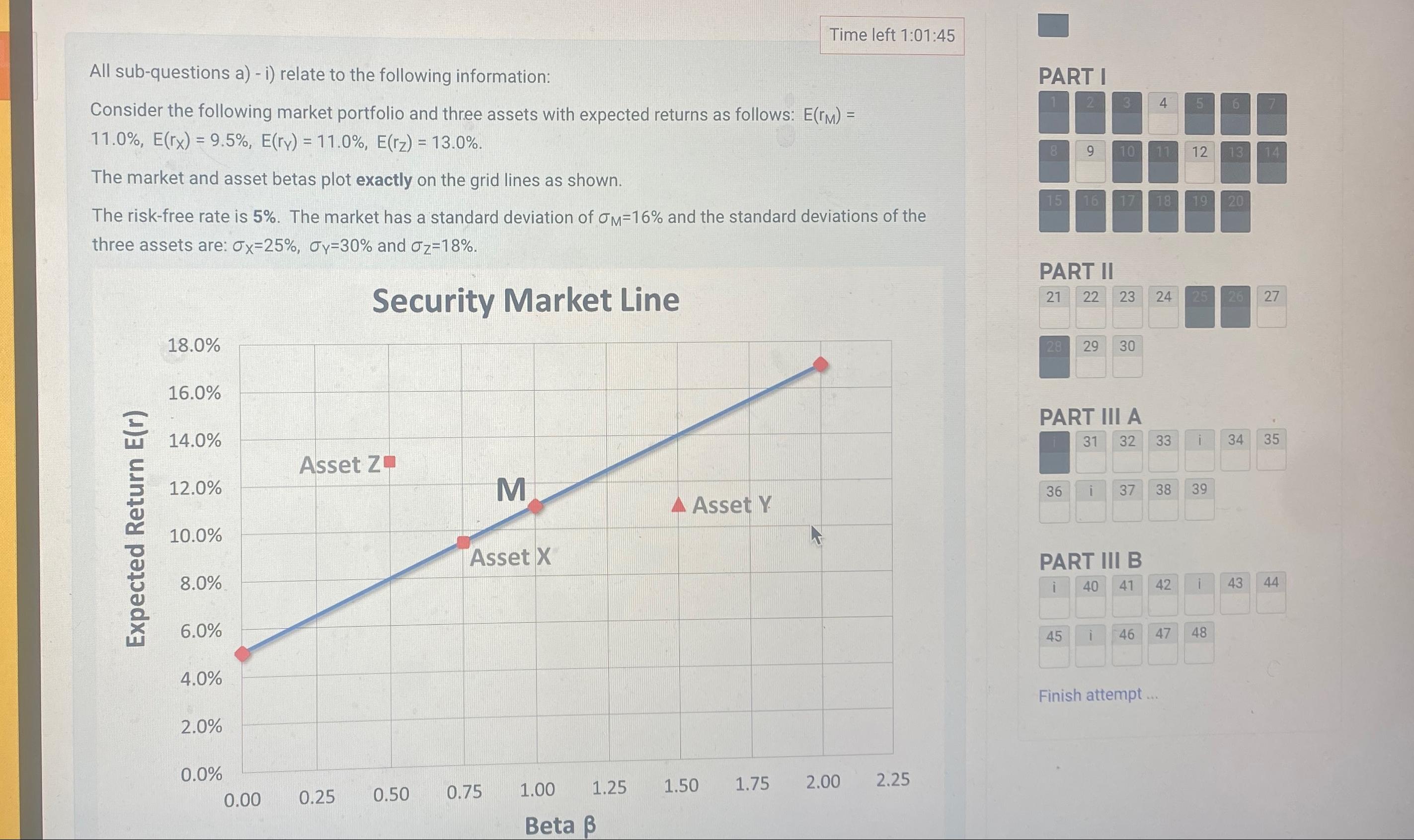

Time left 1 : 0 1 : 4 5 All sub - questions a ) - i ) relate to the following information: Consider the

Time left ::

All subquestions a i relate to the following information:

Consider the following market portfolio and three assets with expected returns as follows:

The market and asset betas plot exactly on the grid lines as shown.

The riskfree rate is The market has a standard deviation of and the standard deviations of the three assets are: and

Security Market Line

PART I

PART II

table

Finish attempt

Question a what are the alphas for asset X Y and Z

Question b what is the name of line, what is its slope state as a decimal what does the slope represent?

C if an equally weighted portfolio were formed from Asset XY and Z what would be the portfolio beta? Answer in decimal places

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Healthcare Finance An Introduction To Accounting And Financial Management

Authors: Louis C. Gapenski

2nd Edition

1567931650, 978-1567931655