Question

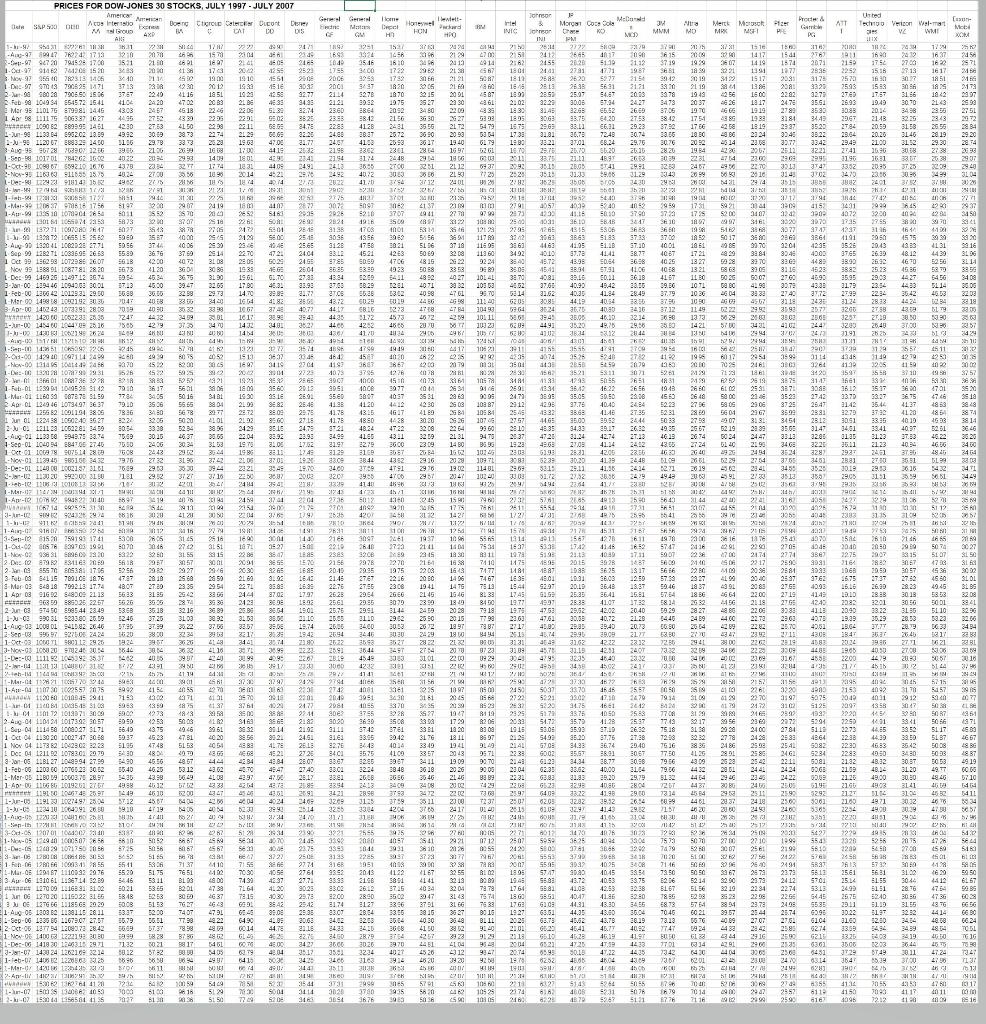

Time series regression. Datasets includes Monthly returns for the Dow-Jones 30 Industrials and the S&P 500 for July 1997-July 2007. a. Calculate the continuous monthly

Time series regression. Datasets includes Monthly returns for the

Dow-Jones 30 Industrials and the S&P 500 for July 1997-July 2007.

a. Calculate the continuous monthly returns for D-J30 and S&P 500. Construct and comment

on the return time series.

b. Using the functions match () and offset (), compare the distributions of returns on the S&P

500 for three periods: the second half of 1999, the second half of 2003, and the second half

of 2006. For the same periods calculate descriptive statistics (mean, standard deviation,

min, max, skewness) and comment on your results.

c. The test of CAPM is based on the time series regressions introduced by Black et al (1972).

Regress the monthly returns of each of the stocks on the S&P 500 using the following

equation:

, = + , + ,

d. Compute the slope, intercept, R 2 , and t-statistics for the slope and intercept. Comment on

the results.

e. Test the validity of CAPM, using the following equation:

= 0 + 1 +

Comment on your result and provide your own thought on the validity of the TEST.

f. CAPM hypothesis holds true when the returns and betas are linearly related with each other,

which means that the slope 2 should be equal to zero. Extend part c by running a test of

non-linearity between the stock returns and their individual betas using the following

equation:

= 0 + 1 + 2 2 +

Comment on your results.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Tor Tor And The Deep Web

Authors: Joshua Welsh

1st Edition

1542745373, 978-1542745376