Answered step by step

Verified Expert Solution

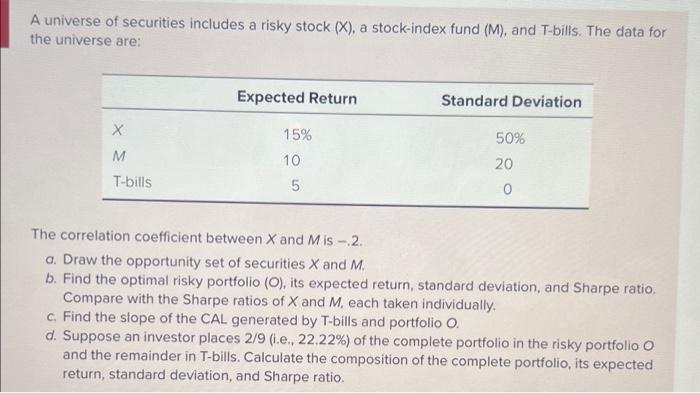

Question

1 Approved Answer

TO 6x depicts the locatie Theatrets code of the dice de the construction of the optimalisya the action of funds between there they com plete

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Fitness Forever 5 Steps To More Money Less Risk And More Peace Of Mind

Authors: Paul Merriman, Richard Buck

1st Edition

0071786988,0071786996