Question

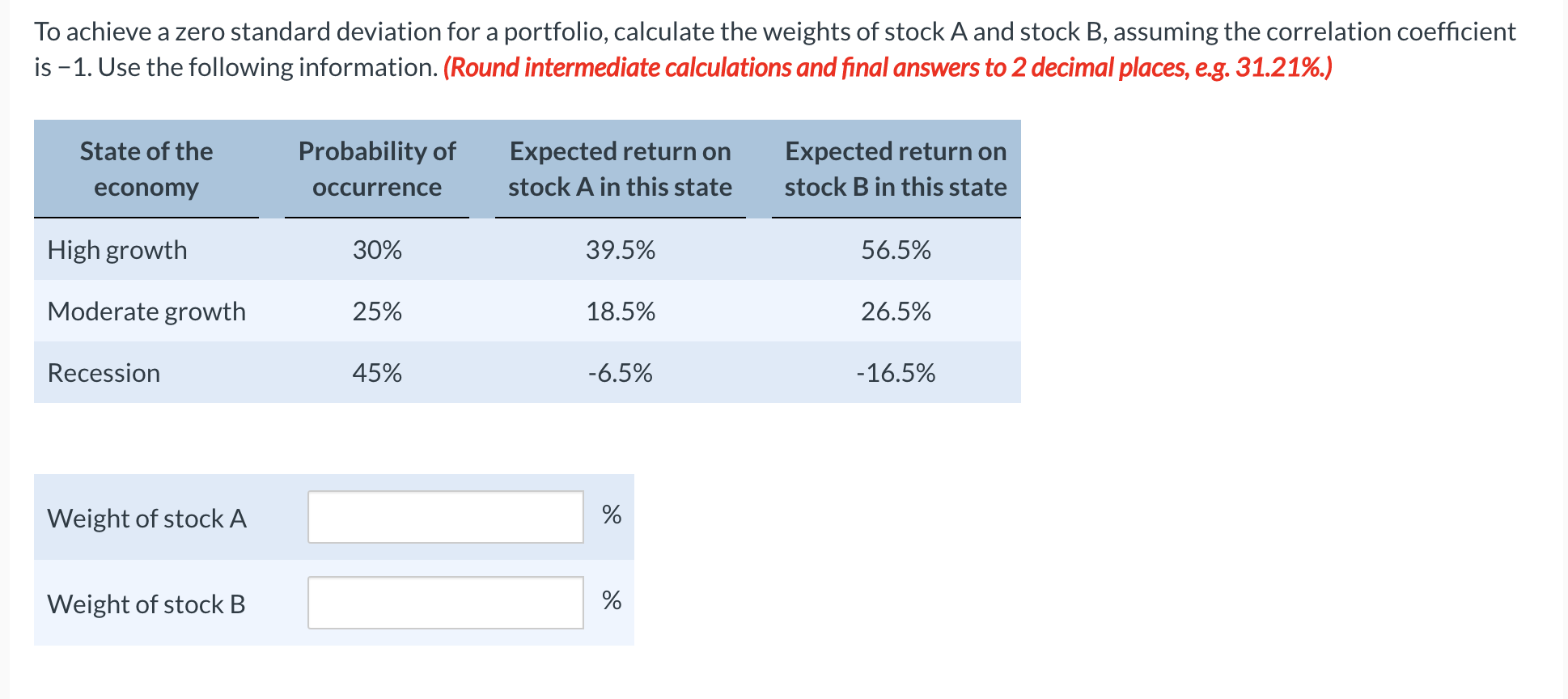

To achieve a zero standard deviation for a portfolio, calculate the weights of stock A and stock B, assuming the correlation coefficient is 1. Use

To achieve a zero standard deviation for a portfolio, calculate the weights of stock A and stock B, assuming the correlation coefficient is 1. Use the following information. (Round intermediate calculations and final answers to 2 decimal places, e.g. 31.21%.)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Personal Finance

Authors: E. Thomas Garman, Raymond E. Forgue, Jonathan Fox

14th Edition

0357901495, 9780357901496