Answered step by step

Verified Expert Solution

Question

1 Approved Answer

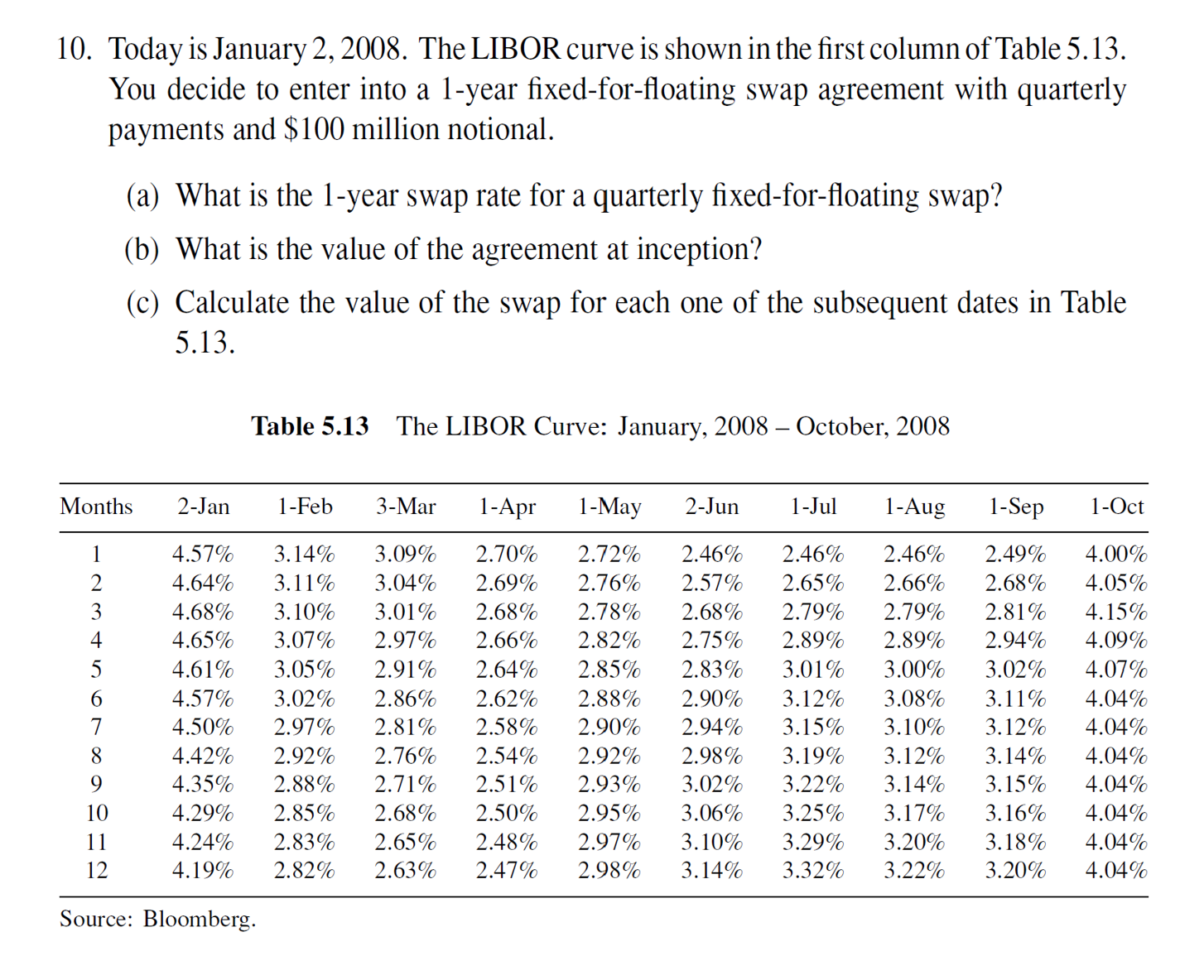

Today is January 2 , 2 0 0 8 . The LIBOR curve is shown in the first column of Table 5 . 1 3

Today is January The LIBOR curve is shown in the first column of Table

You decide to enter into a year fixedforfloating swap agreement with quarterly

payments and $ million notional.

a What is the year swap rate for a quarterly fixedforfloating swap?

b What is the value of the agreement at inception?

c Calculate the value of the swap for each one of the subsequent dates in Table

Table The LIBOR Curve: January, October,

Source: Bloomberg.

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Intermediate Financial Management

Authors: Eugene F. Brigham, Phillip R. Daves

8th Edition

0324258917, 9780324258912