Answered step by step

Verified Expert Solution

Question

1 Approved Answer

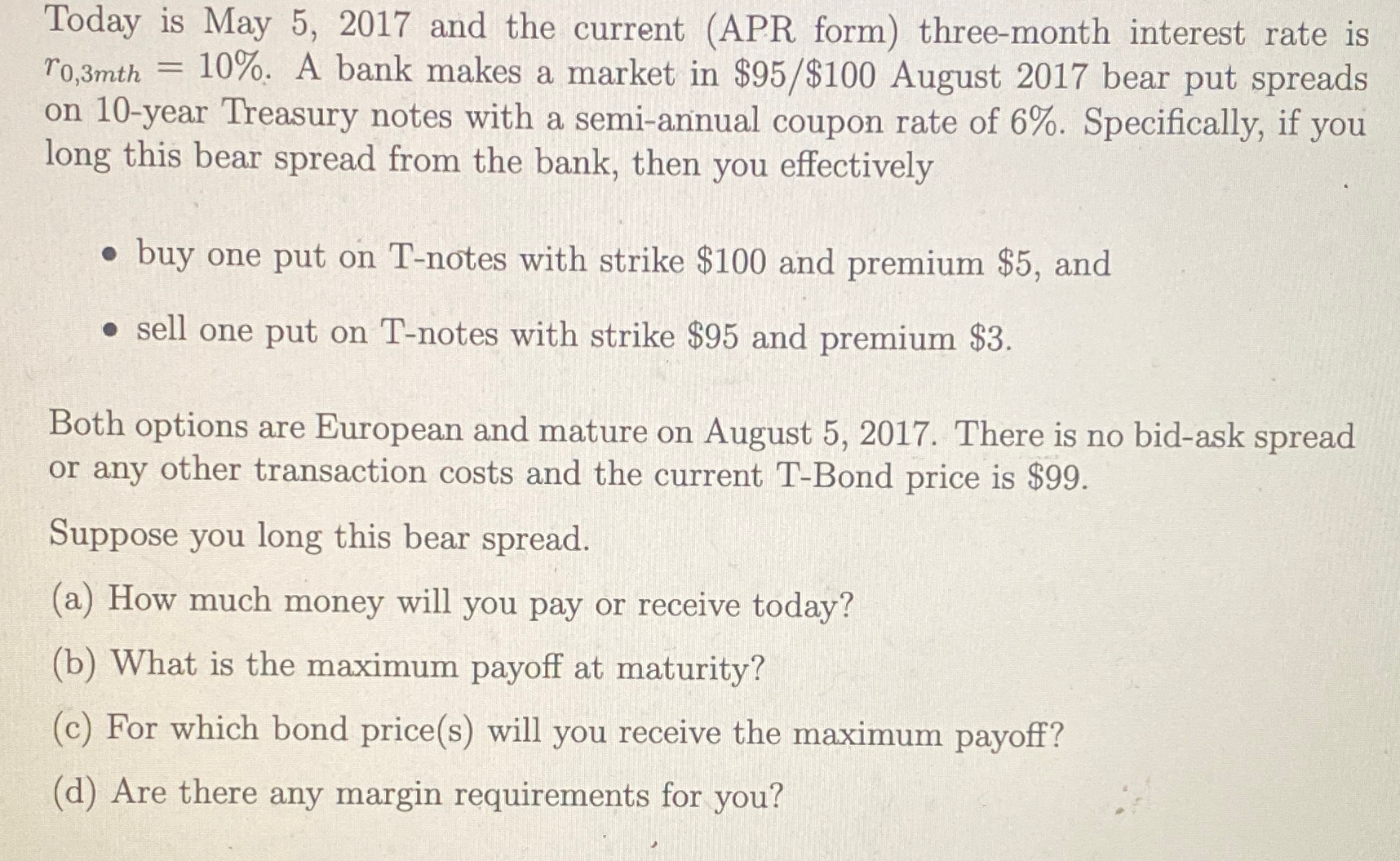

Today is May 5 , 2 0 1 7 and the current ( APR form ) three - month interest rate is r 0 ,

Today is May and the current APR form threemonth interest rate is A bank makes a market in $ August bear put spreads on year Treasury notes with a semiannual coupon rate of Specifically, if you long this bear spread from the bank, then you effectively

buy one put on Tnotes with strike $ and premium $ and

sell one put on Tnotes with strike $ and premium $

Both options are European and mature on August There is no bidask spread or any other transaction costs and the current TBond price is $

Suppose you long this bear spread.

a How much money will you pay or receive today?

b What is the maximum payoff at maturity?

c For which bond prices will you receive the maximum payoff?

d Are there any margin requirements for you?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Finance For Nonfinancial Managers Beginners Handbook For Finance

Authors: Murugesan Ramaswamy

1st Edition

1516973801, 978-1516973804