Question

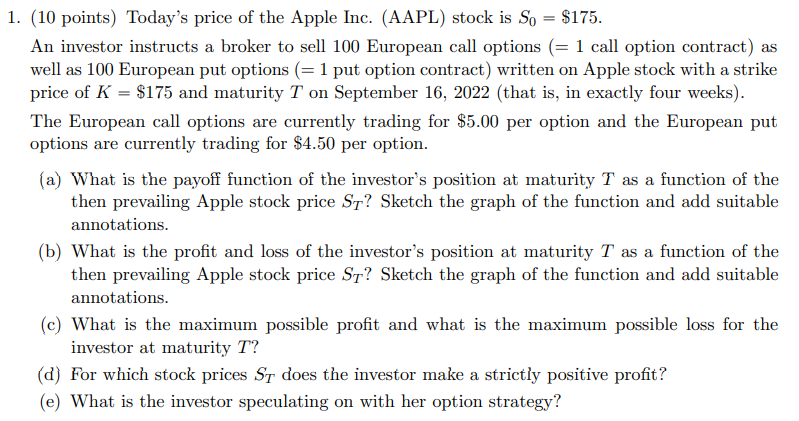

Todays price of the Apple Inc. (AAPL) stock is S0 $175. An investor instructs a broker to sell 100 European call options (= 1 call

Todays price of the Apple Inc. (AAPL) stock is S0 $175. An investor instructs a broker to sell 100 European call options (= 1 call option contract) as well as 100 European put options (= 1 put option contract) written on Apple stock with a strike price of K $175 and maturity T on September 16, 2022 (that is, in exactly four weeks). The European call options are currently trading for $5.00 per option and the European put options are currently trading for $4.50 per option. (a) What is the payoff function of the investors position at maturity T as a function of the then prevailing Apple stock price ST ? Sketch the graph of the function and add suitable annotations. (b) What is the profit and loss of the investors position at maturity T as a function of the then prevailing Apple stock price ST ? Sketch the graph of the function and add suitable annotations. (c) What is the maximum possible profit and what is the maximum possible loss for the investor at maturity T? (d) For which stock prices ST does the investor make a strictly positive profit? (e) What is the investor speculating on with her option strategy?

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Understanding Financial Risk Management

Authors: Angelo Corelli

1st Edition

0415746183, 978-0415746182