Answered step by step

Verified Expert Solution

Question

1 Approved Answer

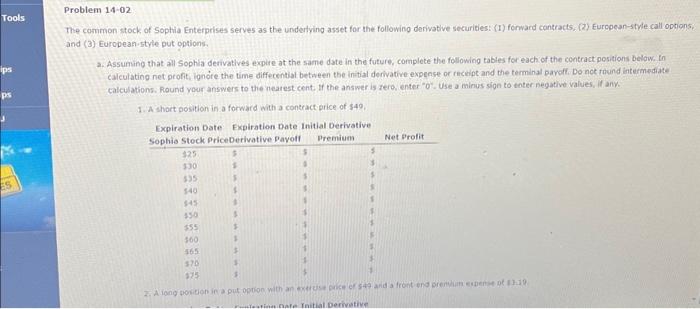

Tools ips ps ES Problem 14-02 The common stock of Sophia Enterprises serves as the underlying asset for the following derivative securities: (1) forward contracts,

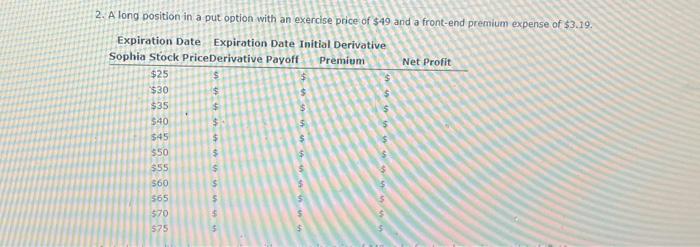

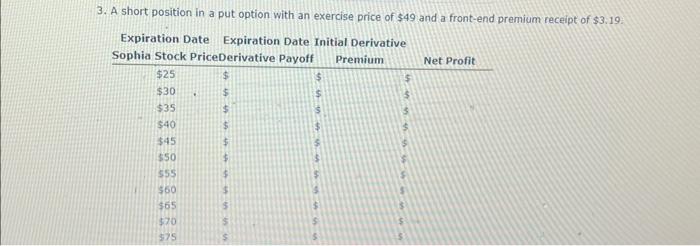

Tools ips ps ES Problem 14-02 The common stock of Sophia Enterprises serves as the underlying asset for the following derivative securities: (1) forward contracts, (2) European-style call options, and (3) European-style put options. a. Assuming that all Sophia derivatives expire at the same date in the future, complete the following tables for each of the contract positions below. In calculating net profit, ignore the time differential between the initial derivative expense or receipt and the terminal payoff. Do not round intermediate calculations. Round your answers to the nearest cent. If the answer is zero, enter "0". Use a minus sign to enter negative values, if any. 1. A short position in a forward with a contract price of $49. Expiration Date Expiration Date Initial Derivative Sophia Stock Price Derivative Payoff $25 $30 $35 $40 $45 $50 $55 $60 $65 $70 $75 2. A long position in a put option with an exercise price of $49 and a front-end premium expense of $3.19. piration Date Initial Derivative $ $ $ $ $ $ $ $ $ $ $ $ $ $ $ Premium $ 69 69 69 69 55 17 5 $ $ Net Profit **

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Planning Demystified A Self Teaching Guide

Authors: Paul Lim

1st Edition

0071476717,0071709711