Answered step by step

Verified Expert Solution

Question

1 Approved Answer

Topic: Portfolio Theory and CAPM (Risk and return) QUESTION 1 The Finance Manager of Mekar Indah Bhd proposes two risky securities and risk-free securities for

Topic: Portfolio Theory and CAPM (Risk and return)

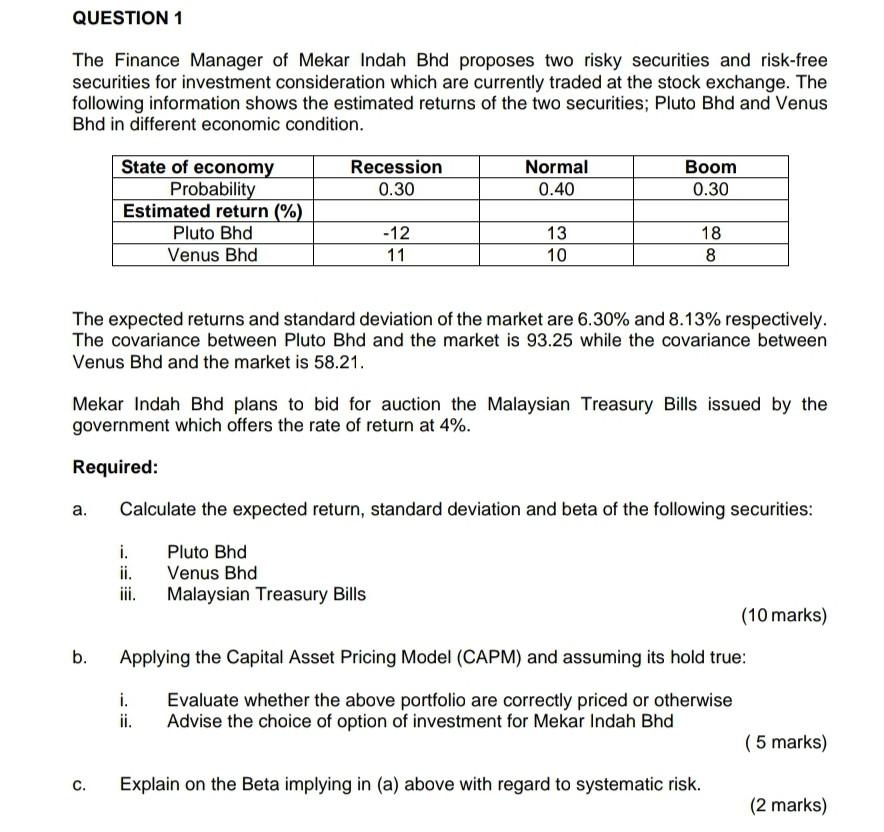

QUESTION 1 The Finance Manager of Mekar Indah Bhd proposes two risky securities and risk-free securities for investment consideration which are currently traded at the stock exchange. The following information shows the estimated returns of the two securities; Pluto Bhd and Venus Bhd in different economic condition. Recession 0.30 Normal 0.40 Boom 0.30 State of economy Probability Estimated return (%) Pluto Bhd Venus Bhd 13 -12 11 10 18 8 The expected returns and standard deviation of the market are 6.30% and 8.13% respectively. The covariance between Pluto Bhd and the market is 93.25 while the covariance between Venus Bhd and the market is 58.21. Mekar Indah Bhd plans to bid for auction the Malaysian Treasury Bills issued by the government which offers the rate of return at 4%. Required: Calculate the expected return, standard deviation and beta of the following securities: a. i. ii. Pluto Bhd Venus Bhd Malaysian Treasury Bills (10 marks) b. Applying the Capital Asset Pricing Model (CAPM) and assuming its hold true: i. ii. Evaluate whether the above portfolio are correctly priced or otherwise Advise the choice of option of investment for Mekar Indah Bhd (5 marks) c. Explain on the Beta implying in (a) above with regard to systematic risk. (2 marks)

Step by Step Solution

There are 3 Steps involved in it

Step: 1

Get Instant Access to Expert-Tailored Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Gender And Finance

Authors: Ylva Baeckström

1st Edition

103205557X, 978-1032055572