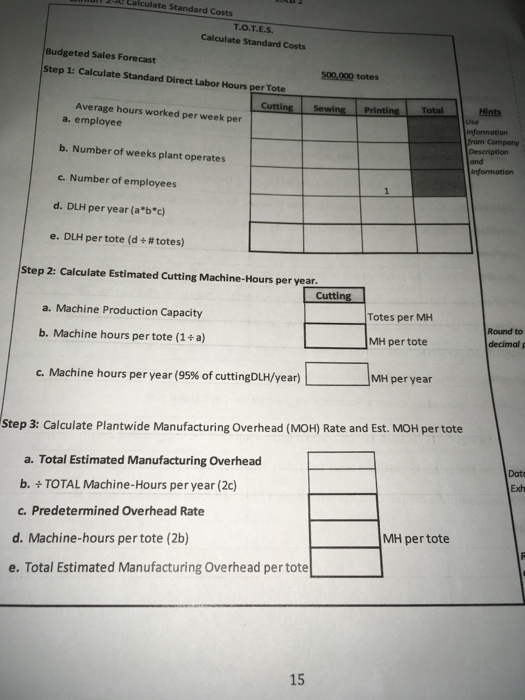

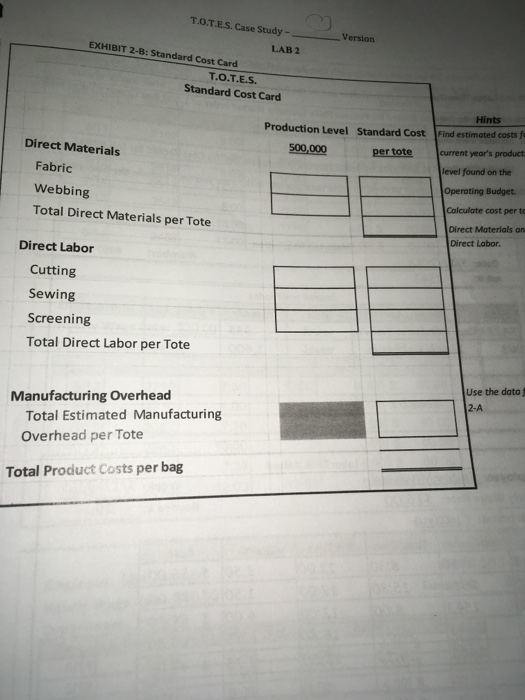

TOTES. CASE STUDY JOB COSTING version Name: LAB 2 their T.o.T.Es, currently uses a job costing system to allocate costs to each job. Although products are very similar, each customer requires a different logo on their custom tote. Furthermore, Tonia and Tara have started experimenting with different sizes and lines of product in order to expand their market. Lab 2 has two parts. Students calculate the standard costs for totes in the first part. In the second part, students allocate actual costs to a specific job. PART 1: Using the data from Lab and the Company Description, students will 1 determine standard costs for direct materials, directlabor and for allocating manufacturing overhead. T.oT.E.s. uses machine hours in the cutting department for allocating manufacturing overhead. Based on historical records, it has been determined that the cutting machines are operating for 95% of the hours worked by cutting department employees. The plant operates 50 weeks per year. The company has two cutting machines. For the current totes each machine can cut fabric for 125 totes each hour. On Exhibit 2-A, calculate e standard number of direct labor (MH) for the cutting machines in Step 2, and calculate the plannwidemandacturinggverhead rate in Step 3. Using this information, create a Standard Cost Card for totes in Exhibit 2-B. PART 2: Costs for each job are tracked using Job Cost Record (Exhibit 2-C). a Copies of the Materials Requisition form and Labor Time Records have been copied so that students can complete the Job Cost Record for Job #2543. All totes shipped on May were 21, 20XX. TOTES. CASE STUDY JOB COSTING version Name: LAB 2 their T.o.T.Es, currently uses a job costing system to allocate costs to each job. Although products are very similar, each customer requires a different logo on their custom tote. Furthermore, Tonia and Tara have started experimenting with different sizes and lines of product in order to expand their market. Lab 2 has two parts. Students calculate the standard costs for totes in the first part. In the second part, students allocate actual costs to a specific job. PART 1: Using the data from Lab and the Company Description, students will 1 determine standard costs for direct materials, directlabor and for allocating manufacturing overhead. T.oT.E.s. uses machine hours in the cutting department for allocating manufacturing overhead. Based on historical records, it has been determined that the cutting machines are operating for 95% of the hours worked by cutting department employees. The plant operates 50 weeks per year. The company has two cutting machines. For the current totes each machine can cut fabric for 125 totes each hour. On Exhibit 2-A, calculate e standard number of direct labor (MH) for the cutting machines in Step 2, and calculate the plannwidemandacturinggverhead rate in Step 3. Using this information, create a Standard Cost Card for totes in Exhibit 2-B. PART 2: Costs for each job are tracked using Job Cost Record (Exhibit 2-C). a Copies of the Materials Requisition form and Labor Time Records have been copied so that students can complete the Job Cost Record for Job #2543. All totes shipped on May were 21, 20XX