Question: (40 points) Recently, stock PLTR has been touted on several newsgroups with comments such as: TUIG: PLTR rocks. Buy before it takes off! Or TTH:

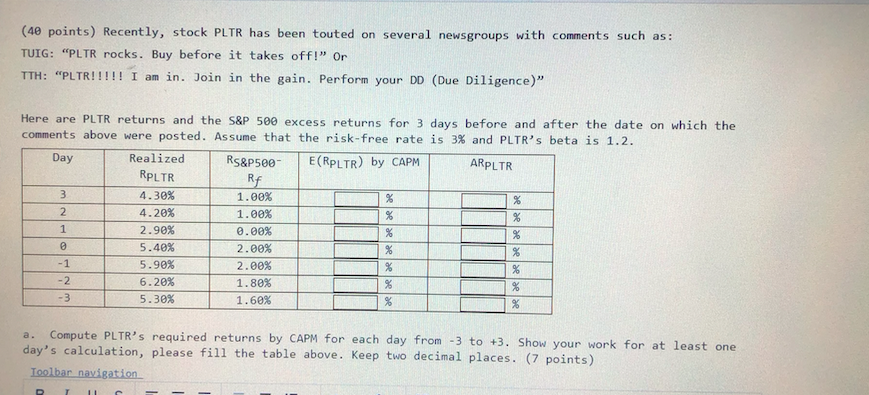

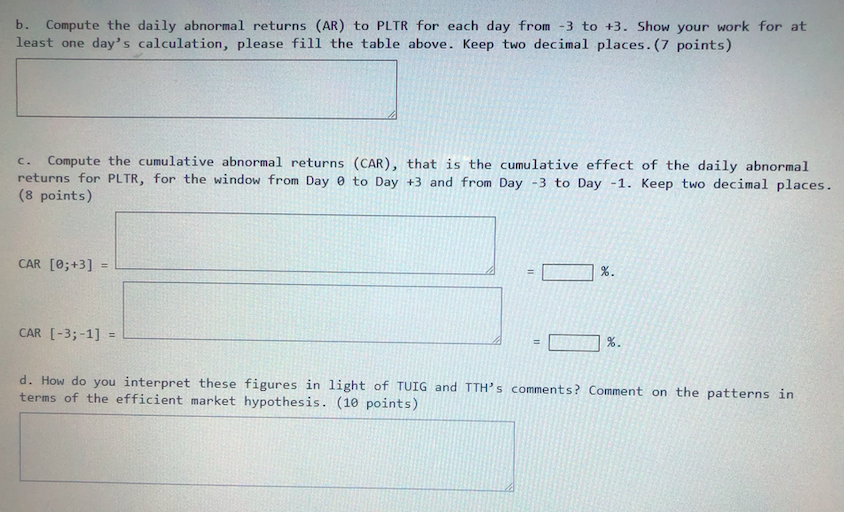

(40 points) Recently, stock PLTR has been touted on several newsgroups with comments such as: TUIG: "PLTR rocks. Buy before it takes off! Or TTH: "PLTR!!!!! I am in. Join in the gain. Perform your DD (Due Diligence)" Here are PLTR returns and the S&P 500 excess returns for 3 days before and after the date on which the comments above were posted. Assume that the risk-free rate is 3% and PLTR's beta is 1.2. Day Realized Rs&P500- E(RPLTR) by CAPM ARPLTR RPLTR Rf 3 4.30% 1.00% % 2 4.20% 1.00% % % 1 2.90% .00% % 5.40% 2.00% % % -1 5.90% 2.00% % % -2 6.20% 1.80% % % -3 5.30% 1.60% % a. Compute PLTR's required returns by CAPM for each day from -3 to +3. Show your work for at least one day's calculation, please fill the table above. Keep two decimal places. (7 points) Toolbar navigation P T b. Compute the daily abnormal returns (AR) to PLTR for each day from 3 to +3. Show your work for at least one day's calculation, please fill the table above. Keep two decimal places.(7 points) C. Compute the cumulative abnormal returns (CAR), that is the cumulative effect of the daily abnormal returns for PLTR, for the window from Day to Day +3 and from Day -3 to Day -1. Keep two decimal places. (8 points) CAR [0;+3] = %. CAR (-3; -1] 11 %. d. How do you interpret these figures in light of TUIG and TTH's comments? Comment on the patterns in terms of the efficient market hypothesis. (10 points) (40 points) Recently, stock PLTR has been touted on several newsgroups with comments such as: TUIG: "PLTR rocks. Buy before it takes off! Or TTH: "PLTR!!!!! I am in. Join in the gain. Perform your DD (Due Diligence)" Here are PLTR returns and the S&P 500 excess returns for 3 days before and after the date on which the comments above were posted. Assume that the risk-free rate is 3% and PLTR's beta is 1.2. Day Realized Rs&P500- E(RPLTR) by CAPM ARPLTR RPLTR Rf 3 4.30% 1.00% % 2 4.20% 1.00% % % 1 2.90% .00% % 5.40% 2.00% % % -1 5.90% 2.00% % % -2 6.20% 1.80% % % -3 5.30% 1.60% % a. Compute PLTR's required returns by CAPM for each day from -3 to +3. Show your work for at least one day's calculation, please fill the table above. Keep two decimal places. (7 points) Toolbar navigation P T b. Compute the daily abnormal returns (AR) to PLTR for each day from 3 to +3. Show your work for at least one day's calculation, please fill the table above. Keep two decimal places.(7 points) C. Compute the cumulative abnormal returns (CAR), that is the cumulative effect of the daily abnormal returns for PLTR, for the window from Day to Day +3 and from Day -3 to Day -1. Keep two decimal places. (8 points) CAR [0;+3] = %. CAR (-3; -1] 11 %. d. How do you interpret these figures in light of TUIG and TTH's comments? Comment on the patterns in terms of the efficient market hypothesis. (10 points)

Step by Step Solution

There are 3 Steps involved in it

Get step-by-step solutions from verified subject matter experts