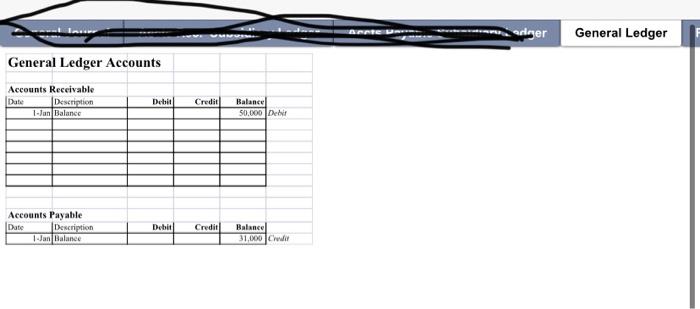

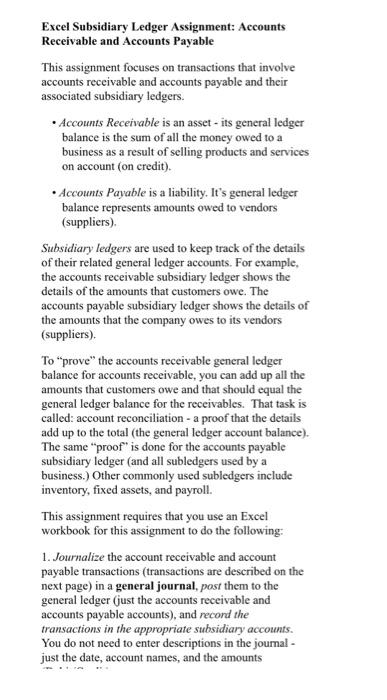

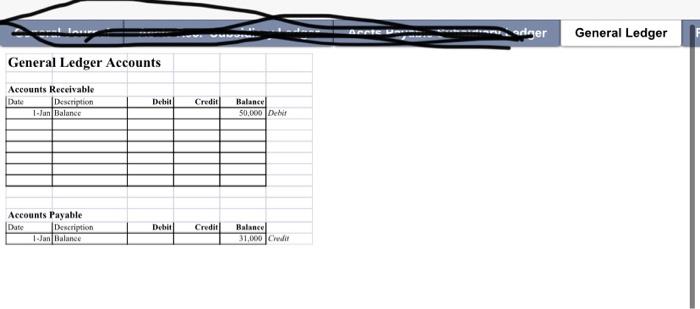

General Ledger Accounts Excel Subsidiary Ledger Assignment: Accounts Receivable and Accounts Payable This assignment focuses on transactions that involve accounts receivable and accounts payable and their associated subsidiary ledgers. - Accounts Receivable is an asset - its general ledger balance is the sum of all the money owed to a business as a result of selling products and services on account (on credit). - Accounts Payable is a liability. It's general ledger balance represents amounts owed to vendors (supplicrs). Subsidiary ledgers are used to keep track of the details of their related general ledger accounts. For example, the accounts receivable subsidiary ledger shows the details of the amounts that customers owe. The accounts payable subsidiary ledger shows the details of the amounts that the company owes to its vendors (suppliers). To "prove" the accounts receivable general ledger balance for accounts receivable, you can add up all the amounts that customers owe and that should equal the general ledger balance for the receivables. That task is called: account reconciliation - a proof that the details add up to the total (the general ledger account balance). The same "proof" is done for the accounts payable subsidiary ledger (and all subledgers used by a business.) Other commonly used subledgers include inventory, fixed assets, and payroll. This assignment requires that you use an Excel workbook for this assignment to do the following: 1. Journalize the account receivable and account payable transactions (transactions are described on the next page) in a general journal, post them to the general ledger (just the accounts receivable and accounts payable accounts), and recond the transactions in the appropriate subsidiary accounts. You do not need to enter descriptions in the journal just the date, account names, and the amounts General Ledger Accounts Excel Subsidiary Ledger Assignment: Accounts Receivable and Accounts Payable This assignment focuses on transactions that involve accounts receivable and accounts payable and their associated subsidiary ledgers. - Accounts Receivable is an asset - its general ledger balance is the sum of all the money owed to a business as a result of selling products and services on account (on credit). - Accounts Payable is a liability. It's general ledger balance represents amounts owed to vendors (supplicrs). Subsidiary ledgers are used to keep track of the details of their related general ledger accounts. For example, the accounts receivable subsidiary ledger shows the details of the amounts that customers owe. The accounts payable subsidiary ledger shows the details of the amounts that the company owes to its vendors (suppliers). To "prove" the accounts receivable general ledger balance for accounts receivable, you can add up all the amounts that customers owe and that should equal the general ledger balance for the receivables. That task is called: account reconciliation - a proof that the details add up to the total (the general ledger account balance). The same "proof" is done for the accounts payable subsidiary ledger (and all subledgers used by a business.) Other commonly used subledgers include inventory, fixed assets, and payroll. This assignment requires that you use an Excel workbook for this assignment to do the following: 1. Journalize the account receivable and account payable transactions (transactions are described on the next page) in a general journal, post them to the general ledger (just the accounts receivable and accounts payable accounts), and recond the transactions in the appropriate subsidiary accounts. You do not need to enter descriptions in the journal just the date, account names, and the amounts