Tree Top Company is a service based company that rents canoes for use on local lakes and rivers. At the beginning of the new

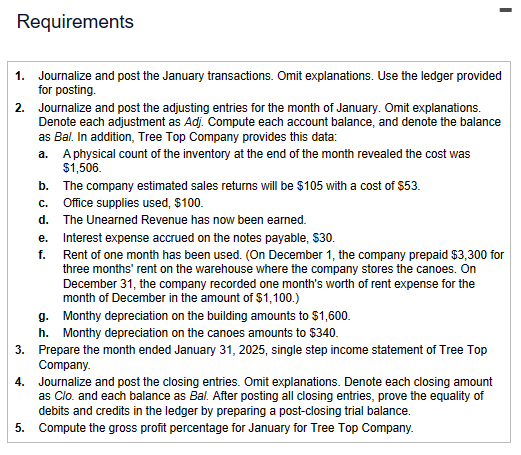

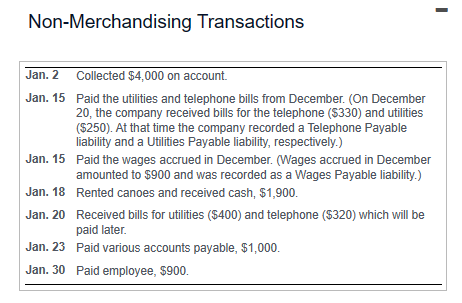

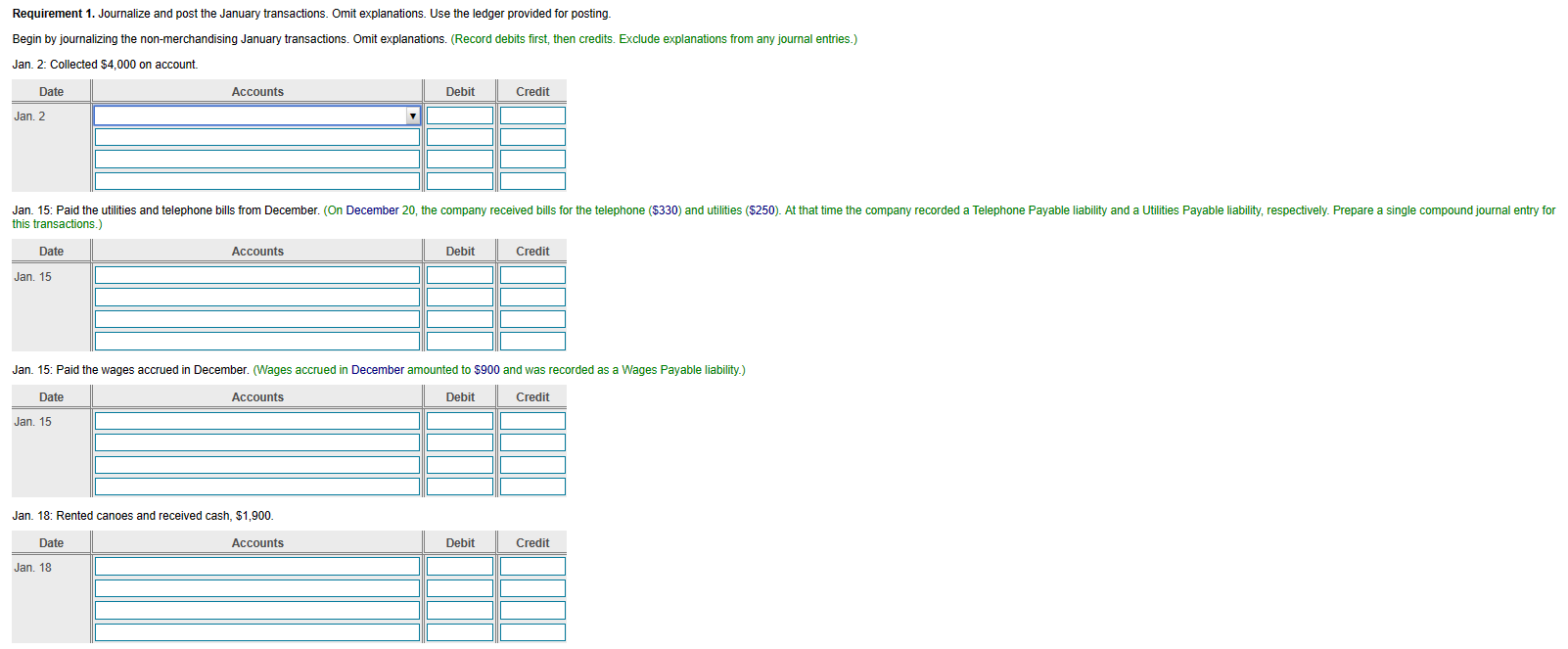

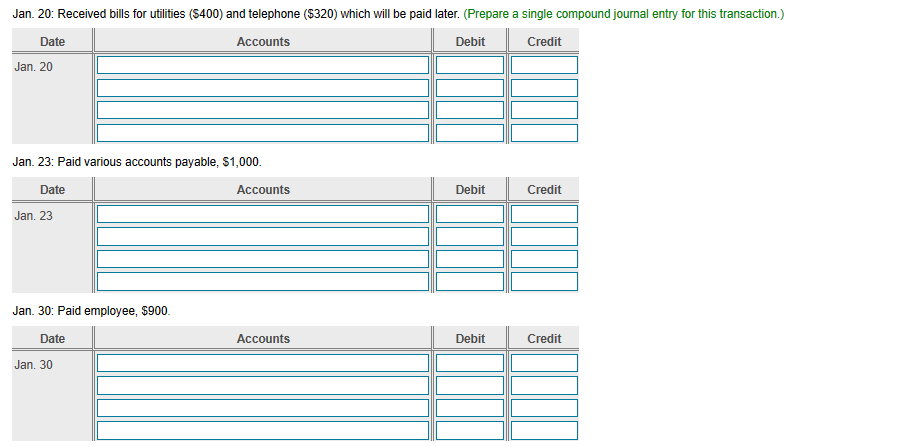

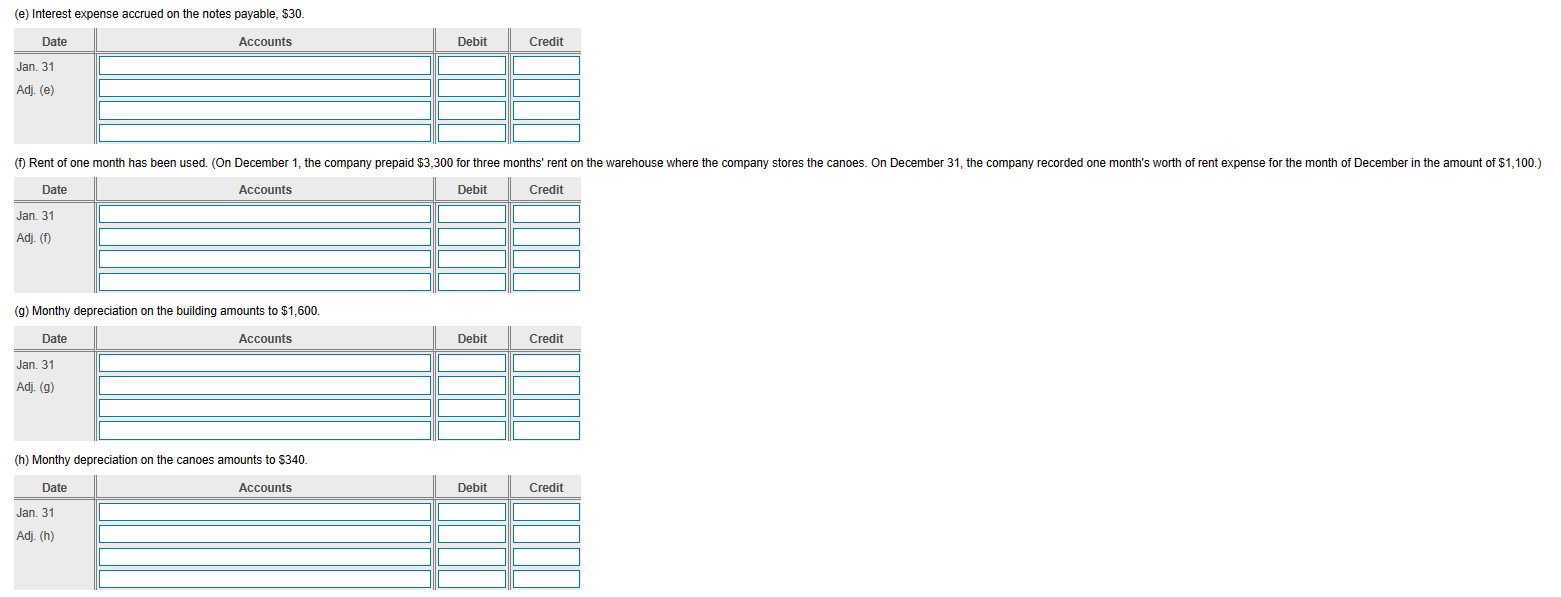

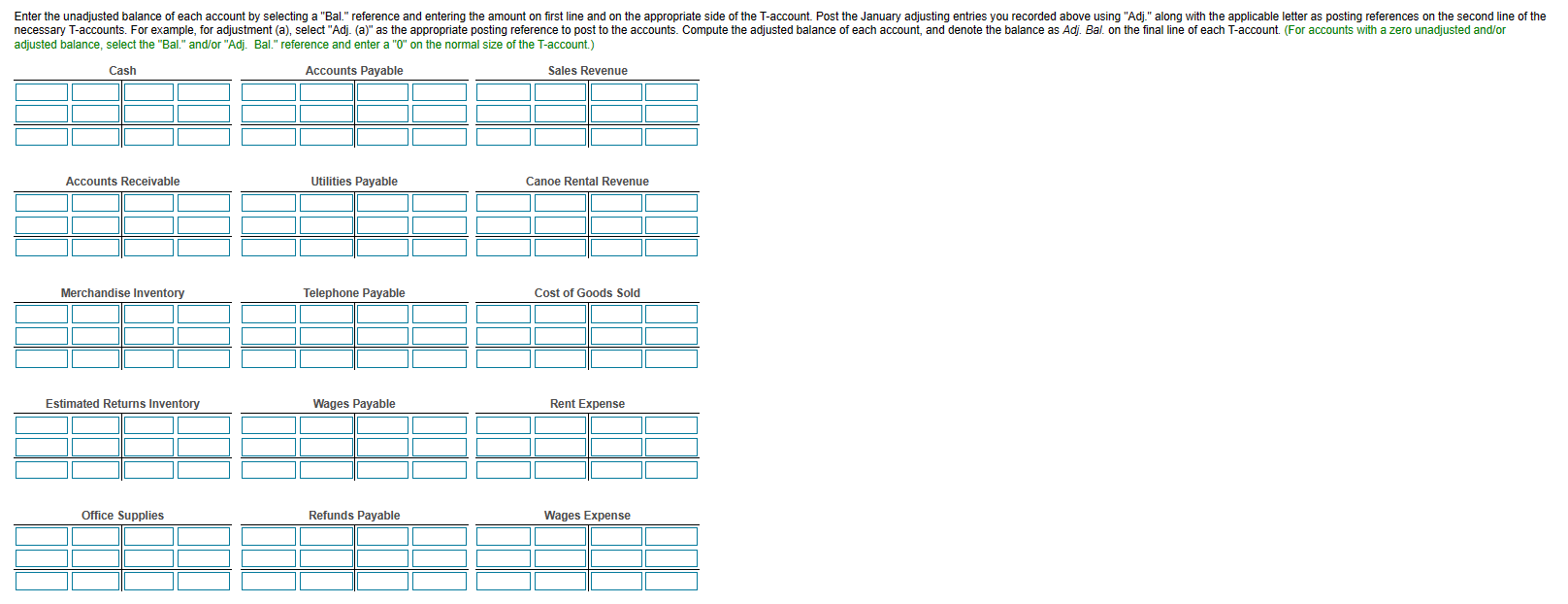

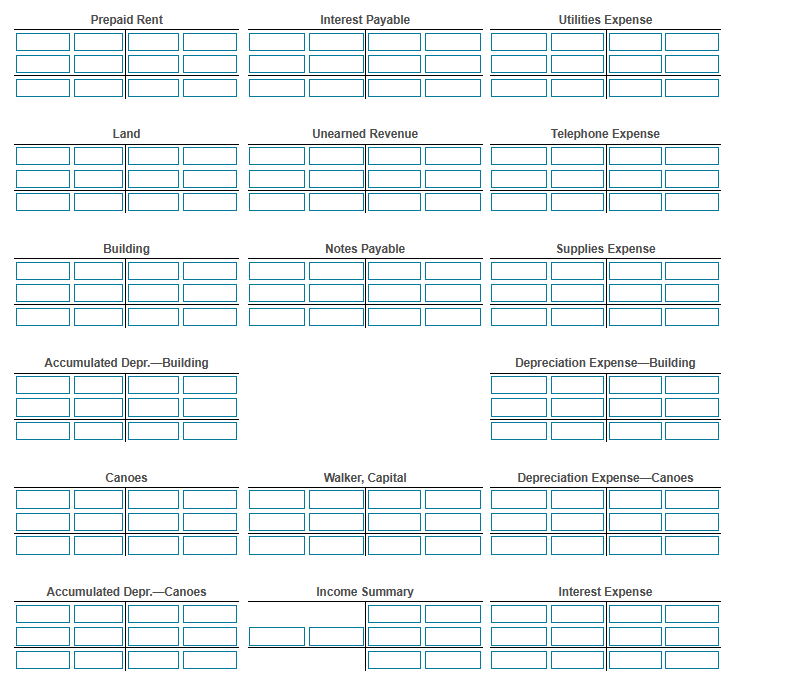

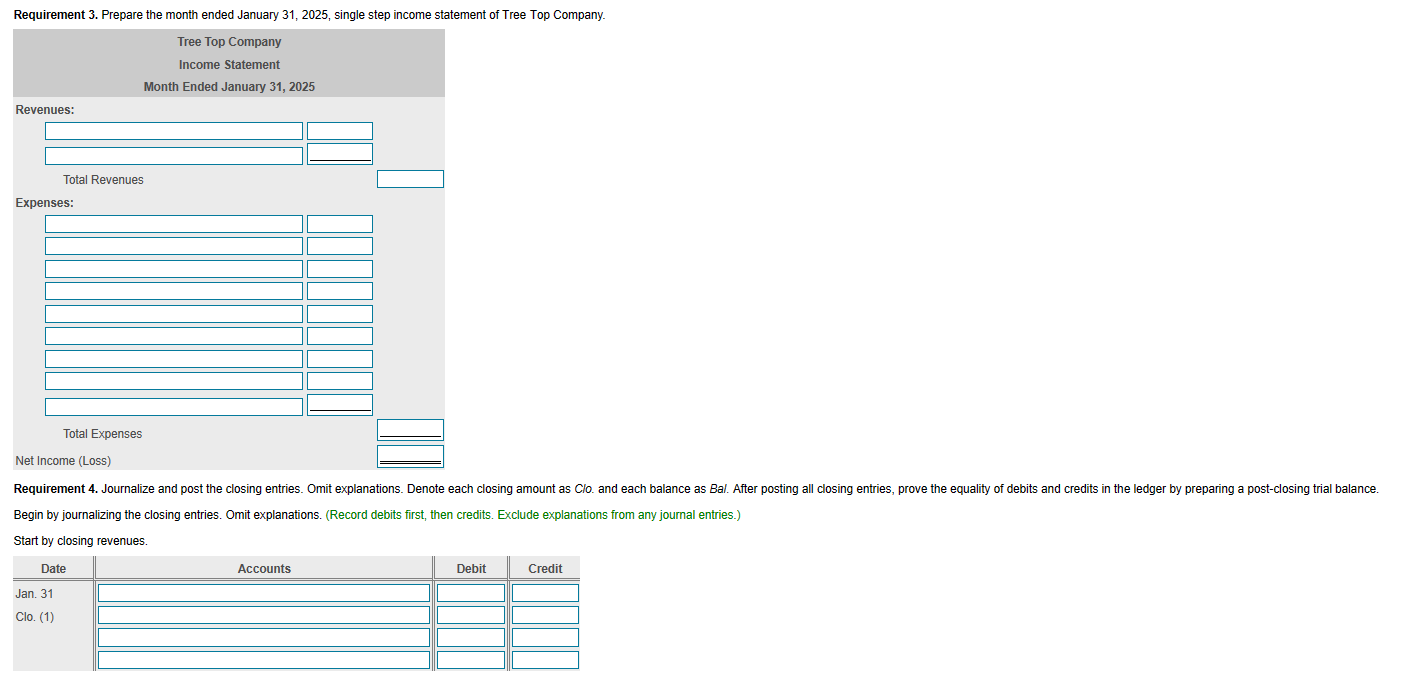

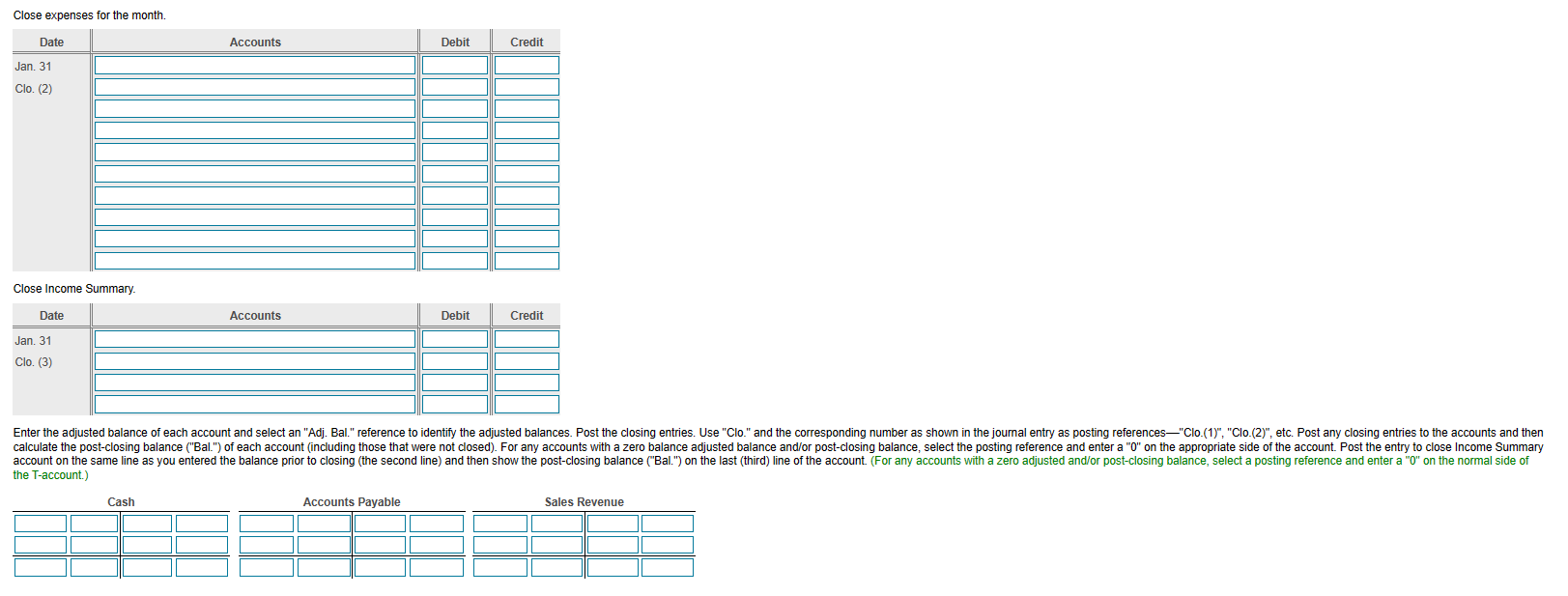

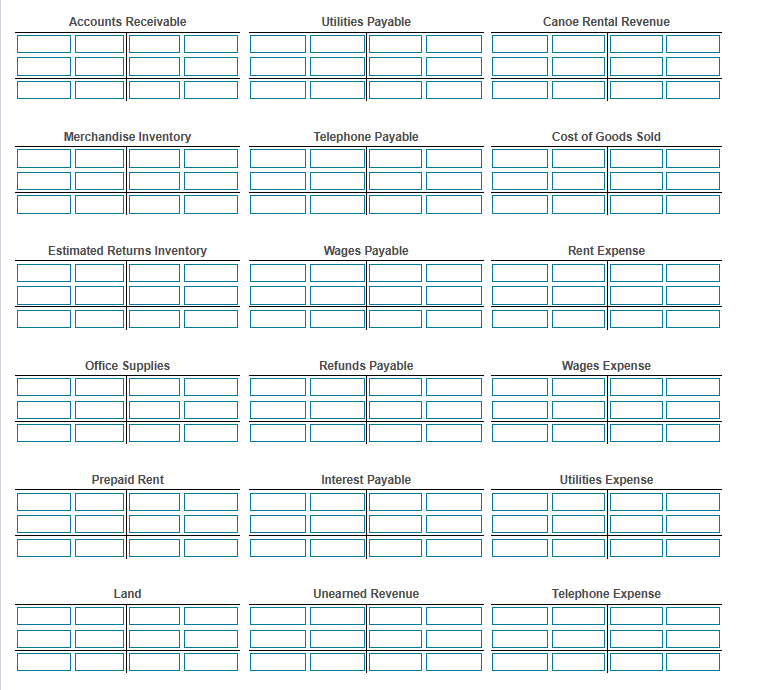

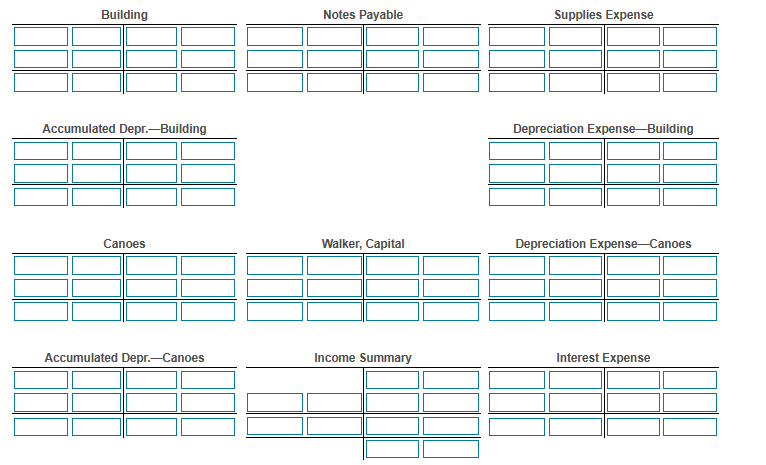

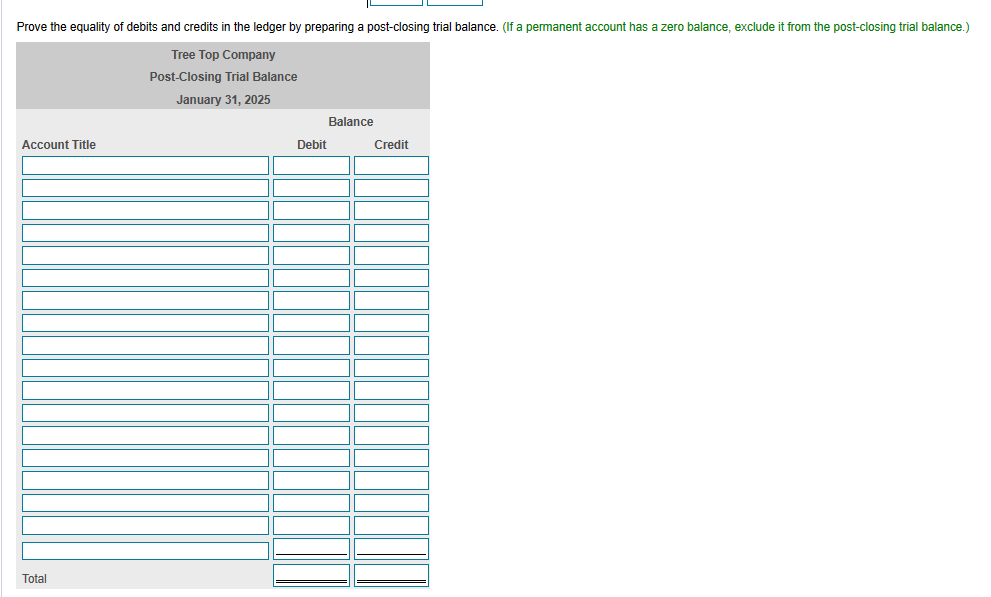

Tree Top Company is a service based company that rents canoes for use on local lakes and rivers. At the beginning of the new year, Tree Top Company decided to carry and sell T-shirts with its logo printed on them. Tree Top Company uses the perpetual inventory system to account for the inventory. During January 2025, Tree Top Company completed these merchandising transactions, and posted the merchandising transactions to the ledger accounts. Tree Top Company does not typically prepare adjusting and closing entries each month, but the company is surprised at how popular the shirts are and wishes to know the net income for January and would also like to understand how to prepare the closing entries for a merchandising company. During January 2025, Tree Top Company completed the following non-merchandising transactions: Requirements 1. Journalize and post the January transactions. Omit explanations. Use the ledger provided for posting. 2. Journalize and post the adjusting entries for the month of January. Omit explanations. Denote each adjustment as Adj. Compute each account balance, and denote the balance as Bal. In addition, Tree Top Company provides this data: a. A physical count of the inventory at the end of the month revealed the cost was $1,506. b. C. d. e. f. The company estimated sales returns will be $105 with a cost of $53. Office supplies used, $100. The Unearned Revenue has now been earned. Interest expense accrued on the notes payable, $30. Rent of one month has been used. (On December 1, the company prepaid $3,300 for three months' rent on the warehouse where the company stores the canoes. On December 31, the company recorded one month's worth of rent expense for the month of December in the amount of $1,100.) g. Monthy depreciation on the building amounts to $1,600. h. Monthy depreciation on the canoes amounts to $340. 3. Prepare the month ended January 31, 2025, single step income statement of Tree Top Company. 4. Journalize and post the closing entries. Omit explanations. Denote each closing amount as Clo. and each balance as Bal. After posting all closing entries, prove the equality of debits and credits in the ledger by preparing a post-closing trial balance. 5. Compute the gross profit percentage for January for Tree Top Company. Non-Merchandising Transactions Jan. 2 Jan. 15 Jan. 15 Jan. 18 Jan. 20 Jan. 23 Jan. 30 Collected $4,000 on account. Paid the utilities and telephone bills from December. (On December 20, the company received bills for the telephone ($330) and utilities ($250). At that time the company recorded a Telephone Payable liability and a Utilities Payable liability, respectively.) Paid the wages accrued in December. (Wages accrued in December amounted to $900 and was recorded as a Wages Payable liability.) Rented canoes and received cash, $1,900. Received bills for utilities ($400) and telephone ($320) which will be paid later. Paid various accounts payable, $1,000. Paid employee, $900. Requirement 1. Journalize and post the January transactions. Omit explanations. Use the ledger provided for posting. Begin by journalizing the non-merchandising January transactions. Omit explanations. (Record debits first, then credits. Exclude explanations from any journal entries.) Jan. 2: Collected $4,000 on account. Date Jan. 2 Date Jan. 15 Jan. 15: Paid the utilities and telephone bills from December. (On December 20, the company received bills for the telephone ($330) and utilities ($250). At that time the company recorded a Telephone Payable liability and a Utilities Payable liability, respectively. Prepare a single compound journal entry for this transactions.) Date Jan. 15 Accounts Date Accounts Jan. 18 Jan. 18: Rented canoes and received cash, $1,900. Jan. 15: Paid the wages accrued in December. (Wages accrued in December amounted to $900 and was recorded as a Wages Payable liability.) Debit Credit Accounts Debit Accounts Debit Credit Debit Credit Credit Jan. 20: Received bills for utilities ($400) and telephone ($320) which will be paid later. (Prepare a single compound journal entry for this transaction.) Date Credit Jan. 20 Jan. 23: Paid various accounts payable, $1,000. Date Jan. 23 Jan. 30: Paid employee, $900. Date Accounts Jan. 30 Accounts Accounts Debit Debit Debit Credit Credit The opening balances of each account (that were determined after recording the January merchandising transactions) have been entered for you. Post the January non-merchandising transactions you recorded above using the dates as posting references. Compute each account balance, and denote the balance as Bal. (For any transactions that occurred on the same date that affect the same account, post to the account in the same order as you prepared the journal entries above. For any accounts with a zero balance after posting the January non-merchandising transactions, select a "Bal." reference and enter a "0" on the normal side of the T-account.) Review the journal entries you prepared above. Cash 10,262 Bal Bal. Bal. Accounts Receivable 7,300 Merchandise Inventory 1,521 Accounts Payable 5,680 Bal. Utilities Payable 250 Bal. Telephone Payable 330 Bal. Bal. Sales Revenue 8,396 Bal. Canoe Rental Revenue 0 Cost of Goods Sold 5,183 Bal. Bal. Bal. Bal. Bal. Bal. Estimated Returns Inventory Office Supplies 800 Prepaid Rent 2,200 Land 110,000 Building 207,000 Wages Payable 900 Bal. Refunds Payable Interest Payable 0 Bal. 30 Bal. Unearned Revenue Notes Payable 300 Bal. 8,640 Bal. Bal. Bal Bal. Bal. Bal. Rent Expense 0 Wages Expense Utilities Expense Telephone Expense 0 Supplies Expense 0 Bal. Accumulated Depr.-Building 1,600 Bal. Canoes 16,320 Accumulated Depr.-Canoes 500 Bal. Jan. 31 Adj. (a) Walker, Capital 333,960 Bal. Income Summary 0 Bal. Bal. Bal. Bal. Depreciation Expense-Building Depreciation Expense-Canoes 0 Interest Expense 0 Requirement 2. Journalize and post the adjusting entries for the month of January. Omit explanations. Denote each adjustment as Adj. Compute each account balance, and denote the balance as Bal. Begin by journalizing the adjusting entries for the month of January. Omit explanations. (Record debits first, then credits. Exclude explanations from any journal entries.) (a) A physical count of the inventory at the end of the month revealed the cost was $1,506. Date Accounts Debit Credit (b) The company estimated sales returns will be $105 with a cost of $53. Begin by preparing the entry to journalize the sales portion of the adjustment. Do not record the expense adjustment related to the information. We will do that in the following step. Date Accounts Debit Credit Jan. 31 Adj. (b) Now journalize the expense adjustment related to the estimated sales returns. Date Accounts Jan. 31 Adj. (b) (c) Office supplies used, $100. Date Jan. 31 Adj. (c) Date Accounts Jan. 31 Adj. (d) Debit Debit Credit (d) The Unearned Revenue has now been earned. (The Unearned Revenue balance was initially recorded in December as part of fees paid by customers for the future rental of canoes.) Accounts Credit Debit Credit (e) Interest expense accrued on the notes payable, $30. Date Accounts Jan. 31 Adj. (e) (g) Monthy depreciation on the building amounts to $1,600. Date Accounts (1) Rent of one month has been used. (On December 1, the company prepaid $3,300 for three months' rent on the warehouse where the company stores the canoes. On December 31, the company recorded one month's worth of rent expense for the month of December in the amount of $1,100.) Date Accounts Credit Debit Jan. 31 Adj. (f) Jan. 31 Adj. (g) (h) Monthy depreciation on the canoes amounts to $340. Date Accounts Debit Jan. 31 Adj. (h) Debit Credit Debit Credit Credit Enter the unadjusted balance of each account by selecting a "Bal." reference and entering the amount on first line and on the appropriate side of the T-account. Post the January adjusting entries you recorded above using "Adj." along with the applicable letter as posting references on the second line of the necessary T-accounts. For example, for adjustment (a), select "Adj. (a)" as the appropriate posting reference to post to the accounts. Compute the adjusted balance of each account, and denote the balance as Adj. Bal. on the final line of each T-account. (For accounts with a zero unadjusted and/or adjusted balance, select the "Bal." and/or "Adj. Bal." reference and enter a "0" on the normal size of the T-account.) Cash Accounts Payable Sales Revenue Accounts Receivable Merchandise Inventory Estimated Returns Inventory Office Supplies Utilities Payable Telephone Payable Wages Payable Refunds Payable Canoe Rental Revenue Cost of Goods Sold Rent Expense Wages Expense Prepaid Rent Land Building Accumulated Depr.-Building Canoes Accumulated Depr.-Canoes Interest Payable Unearned Revenue Notes Payable Walker, Capital Income Summary Utilities Expense Telephone Expense Supplies Expense Depreciation Expense-Building Depreciation Expense-Canoes Interest Expense Requirement 3. Prepare the month ended January 31, 2025, single step income statement of Tree Top Company. Tree Top Company Income Statement Month Ended January 31, 2025 Revenues: Total Revenues Expenses: Total Expenses Net Income (Loss) Requirement 4. Journalize and post the closing entries. Omit explanations. Denote each closing amount as Clo. and each balance as Bal. After posting all closing entries, prove the equality of debits and credits in the ledger by preparing Begin by journalizing the closing entries. Omit explanations. (Record debits first, then credits. Exclude explanations from any journal entries.) Start by closing revenues. Jan. 31 Clo. (1) Date Accounts Debit Credit post-closing trial balance. Close expenses for the month. Date Jan. 31 Clo. (2) Close Income Summary. Date Jan. 31 Clo. (3) Accounts Cash Accounts Debit Accounts Payable Debit Credit Enter the adjusted balance f each account and select an "Adj. Bal." reference to identify the adjusted balances. Post the closing entries. Use "Clo." and the corresponding number as shown in the journal entry as posting references-"Clo.(1)", "Clo.(2)", etc. Post any closing entries to the accounts and then calculate the post-closing balance ("Bal.") of each account (including those that were not closed). For any accounts with a zero balance adjusted balance and/or post-closing balance, select the posting reference and enter a "0" on the appropriate side of the account. Post the entry to close Income Summary account on the same line as you entered the balance prior to closing (the second line) and then show the post-closing balance ("Bal.") on the last (third) line of the account. (For any accounts with a zero adjusted and/or post-closing balance, select a posting reference and enter a "0" on the normal side of the T-account.) Credit Sales Revenue Accounts Receivable Merchandise Inventory Estimated Returns Inventory Office Supplies Prepaid Rent Land Utilities Payable Telephone Payable Wages Payable Refunds Payable Interest Payable Unearned Revenue Canoe Rental Revenue Cost of Goods Sold Rent Expense Wages Expense Utilities Expense Telephone Expense Building Accumulated Depr.-Building Canoes Accumulated Depr.-Canoes Notes Payable Walker, Capital Income Summary Supplies Expense Depreciation Expense-Building Depreciation Expense-Canoes Interest Expense Prove the equality of debits and credits in the ledger by preparing a post-closing trial balance. (If a permanent account has a zero balance, exclude it from the post-closing trial balance.) Tree Top Company Post-Closing Trial Balance January 31, 2025 Account Title Total Debit Balance Credit Requirement 5. Compute the gross profit percentage for January for Tree Top Company. (Round the gross profit percentage to the nearest tenth of a percent, X.X%.) Gross profit % % = =

Step by Step Solution

There are 3 Steps involved in it

Step: 1

1 Journalize and post the January transactions Prepare journal entries for all January transactions and post them to the respective ledger accounts 2 Journalize and post the adjusting entries for Janu...

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Authors: Tracie L. Miller Nobles, Brenda L. Mattison, Ella Mae Matsumura

6th Edition

978-0134486840, 134486838, 134486854, 134486846, 9780134486833, 978-0134486857